Crypto lending limits to account for

Crypto Lending Analysis works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Crypto lending choices that change the plan

Crypto lending offers a way to earn yield or access liquidity without selling your assets, but it introduces specific operational and market risks that differ from traditional banking. Understanding these tradeoffs helps you decide whether the potential return justifies the exposure to platform solvency and smart contract vulnerabilities.

Platform counterparty risk

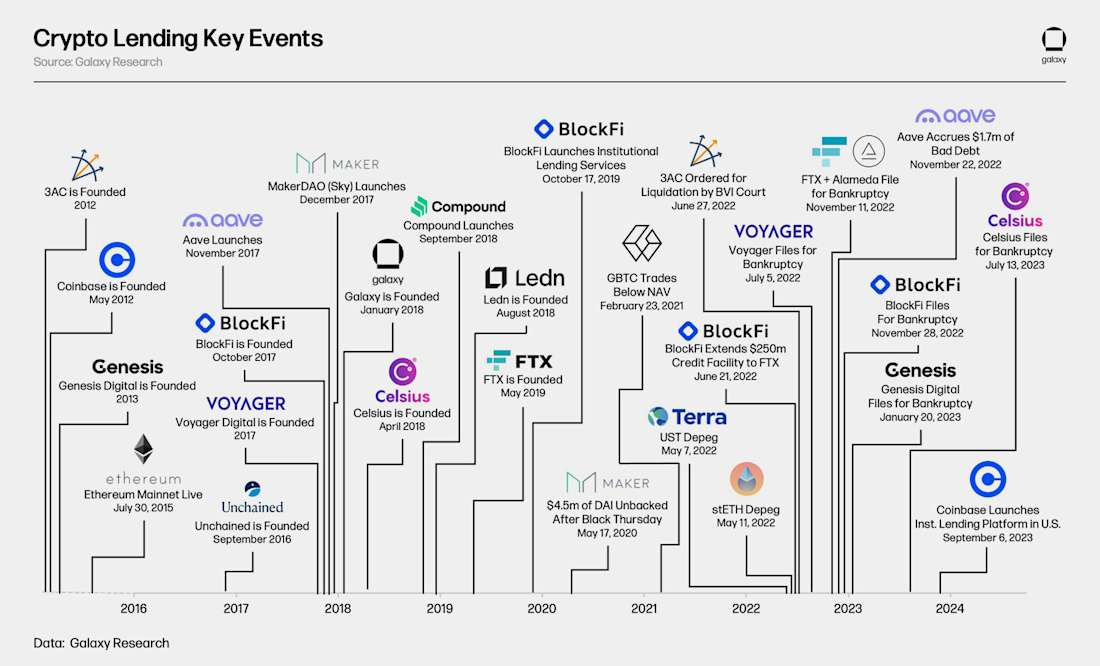

When you lend through a centralized platform, you are taking on credit risk. If the lender defaults or faces insolvency, your assets may be frozen or lost. This was evident in the collapse of several major lending protocols in 2022. Unlike insured bank deposits, crypto lending lacks federal protection, making platform selection critical. You should evaluate the platform's reserve audits, insurance funds, and historical compliance record before depositing assets.

Liquidation mechanics and volatility

For crypto-backed loans, the loan-to-value (LTV) ratio determines your safety margin. If the collateral price drops rapidly, the platform may liquidate your assets to cover the loan. This can happen even if you intend to repay the loan later. High volatility in assets like Bitcoin or Ethereum can trigger liquidations during brief market dips. Setting conservative LTVs and monitoring positions closely is essential to avoid unwanted asset sales.

Yield sustainability and RWA exposure

Yields in decentralized finance (DeFi) often come from real-world asset (RWA) backends or liquidity provision fees. These yields can be high but are not guaranteed. They depend on the continued demand for borrowing and the performance of underlying assets. In contrast, stablecoin yields may be lower but are often more predictable. Assess whether the yield is driven by genuine economic activity or unsustainable token emissions that could collapse if market conditions shift.

Smart contract and technical risk

DeFi lending relies on smart contracts that execute transactions automatically. While transparent, these contracts can contain bugs or vulnerabilities that exploiters can target. Audits reduce but do not eliminate this risk. A single flaw can lead to significant losses. Additionally, you face technical risks such as private key loss or wallet compromise. Using hardware wallets and multi-signature setups can mitigate some of these risks, but they add complexity to the lending process.

| Feature | Centralized (CeFi) | Decentralized (DeFi) | RWA-Backed |

|---|---|---|---|

| Counterparty Risk | High (platform default) | Low (smart contract only) | Medium (originator default) |

| Yield Source | Platform spread | Liquidity fees | Real asset cash flow |

| Regulatory Oversight | Moderate (varies by jurisdiction) | Minimal | Growing (compliant issuers) |

| Asset Custody | Platform holds keys | User holds keys | Third-party custodian |

| Liquidation Speed | Manual or semi-automated | Instant (on-chain) | Negotiated or automated |

How to vet crypto lending platforms

Crypto lending offers yield, but the infrastructure carries distinct risks. Before allocating capital, use this framework to evaluate platforms on security, transparency, and counterparty quality.

Require real-time or frequent proof of reserves (PoR) for deposited assets. Independent audits from reputable firms should confirm that user funds are not commingled with operational capital. Platforms lacking transparent, verifiable solvency reports present unacceptable risk.

Examine the assets accepted as collateral. High loan-to-value (LTV) ratios on volatile assets increase liquidation risk. Platforms should maintain conservative LTVs and have clear, automated liquidation protocols to protect lenders during market downturns.

Prefer platforms operating in regulated jurisdictions or those that have obtained specific licenses (e.g., BitLicense, MSB). Regulatory compliance often signals stricter internal controls and consumer protection measures, reducing the risk of sudden shutdowns or asset freezes.

If the platform uses decentralized protocols, review their smart contract audit history. Look for multiple audits from top-tier firms and active bug bounty programs. Unaudited or poorly maintained contracts are a primary vector for total loss of funds.

Watch for weak options and misleading claims

Crypto lending promises passive income, but the 2026 landscape hides risks that simple yield numbers don't show. Borrowers and lenders alike face infrastructure gaps, regulatory shifts, and hidden fees that can erode returns faster than market volatility. Before committing capital, you need to spot the weak links in the chain.

Misleading APY claims

Platforms often advertise annual percentage yields (APY) that assume 100% collateralization and no liquidation events. These numbers ignore the cost of borrowing against your own assets. If you borrow stablecoins against Bitcoin to earn yield elsewhere, you are paying spread. The net return is rarely as high as the headline APY suggests. Check if the yield is net of borrowing costs or gross. Gross figures are marketing tools, not profit metrics.

Overcollateralization traps

Most crypto loans require overcollateralization, meaning you must lock up more value than you borrow. If the collateral asset drops 10-20%, you face liquidation. Some platforms allow partial liquidation, which sells off your best assets first. This is a slow bleed that destroys long-term position value. Look for platforms that offer flexible collateral ratios or allow you to set your own liquidation thresholds. If the platform forces a binary liquidation, you are taking on unnecessary risk.

Smart contract and infrastructure risks

DeFi lending protocols rely on code. Bugs in smart contracts can lead to total loss of funds. Even reputable platforms have been exploited. Check if the protocol has been audited by multiple firms and if the audit reports are public. Look for bug bounty programs. If a platform lacks transparency around its code or has a history of unpatched vulnerabilities, walk away. The yield is not worth the risk of a total wipeout.

Regulatory and custody uncertainty

Regulatory scrutiny is increasing. Platforms may freeze withdrawals or change terms to comply with new laws. Understand who holds your private keys. Non-custodial platforms give you control but require technical expertise. Custodial platforms hold your keys, meaning you trust the company. If the company collapses, you lose your assets. Choose based on your risk tolerance and technical ability. Do not assume regulatory protection exists for crypto assets.

Crypto lending: what to check next

Crypto lending sits at the intersection of high yield and protocol risk. Before committing capital to RWA yields or DeFi infrastructure, it helps to understand the mechanics and the tradeoffs involved.

No comments yet. Be the first to share your thoughts!