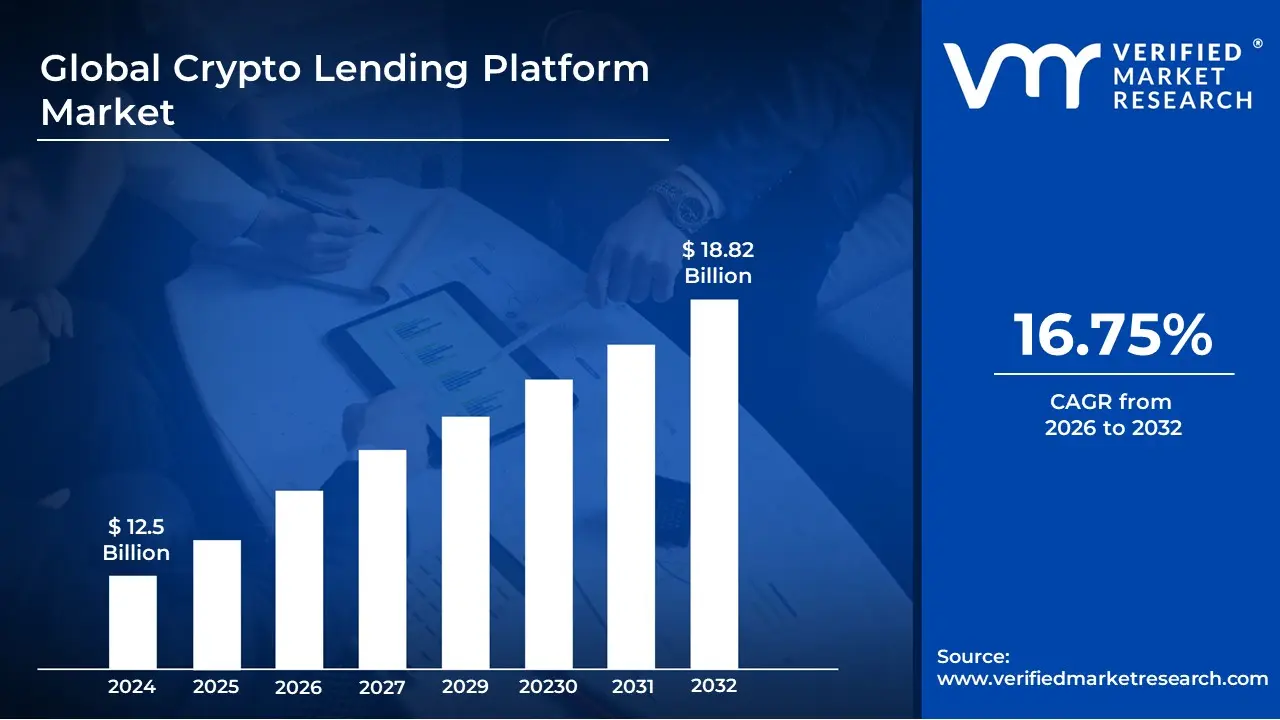

Market size and growth trajectory

The crypto lending market is recovering from the liquidity crunch of 2022, but the scale of current activity suggests a fundamentally different ecosystem than the one that existed a few years ago. At the end of Q3 2025, crypto-collateralized lending reached an all-time high of $73.59 billion, according to Galaxy Research. This peak was driven largely by decentralized finance (DeFi) protocols, which captured approximately two-thirds of the total volume.

While that record high has since corrected, the long-term trajectory remains upward. The global crypto lending platform market is projected to reach $25.06 billion by 2030, growing at a compound annual rate of 18.5%. This growth is not just a return to previous levels but an expansion into new institutional and retail segments that were previously excluded due to regulatory uncertainty.

The shift from opaque, centralized lenders to transparent, on-chain protocols has changed how capital flows. Lenders now retain ownership of their assets while earning returns, with smart contracts enforcing collateralization ratios in real time. This structural change has reduced counterparty risk—the primary cause of failures like Celsius and Voyager—but has introduced new complexities around oracle reliability and liquidation mechanics.

DeFi dominance over centralized venues

Use this section to make the Crypto Lending Market Research decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Real world assets driving new liquidity

Real world assets (RWA) are shifting crypto lending from a speculative game to a utility-driven market. By tokenizing tangible assets like treasury bills and real estate, platforms are introducing a stable class of collateral that does not swing with Bitcoin's daily volatility. This shift allows lenders to earn yields backed by cash flows rather than pure market sentiment.

The integration of RWA acts as a shock absorber for lending protocols. When crypto markets crash, borrowers can still service loans using yields generated from traditional assets. This decoupling reduces the risk of liquidation cascades that plagued the industry in previous cycles. It also opens the door for institutional capital that requires regulatory clarity and predictable returns.

The IMF has noted the growing macroeconomic importance of these instruments, highlighting the need for clear recording standards as crypto lending merges with traditional finance. As regulatory frameworks solidify, RWA-backed lending is poised to become a primary source of on-chain liquidity, offering a bridge between decentralized finance and the global bond market.

Risk management and collateral dynamics

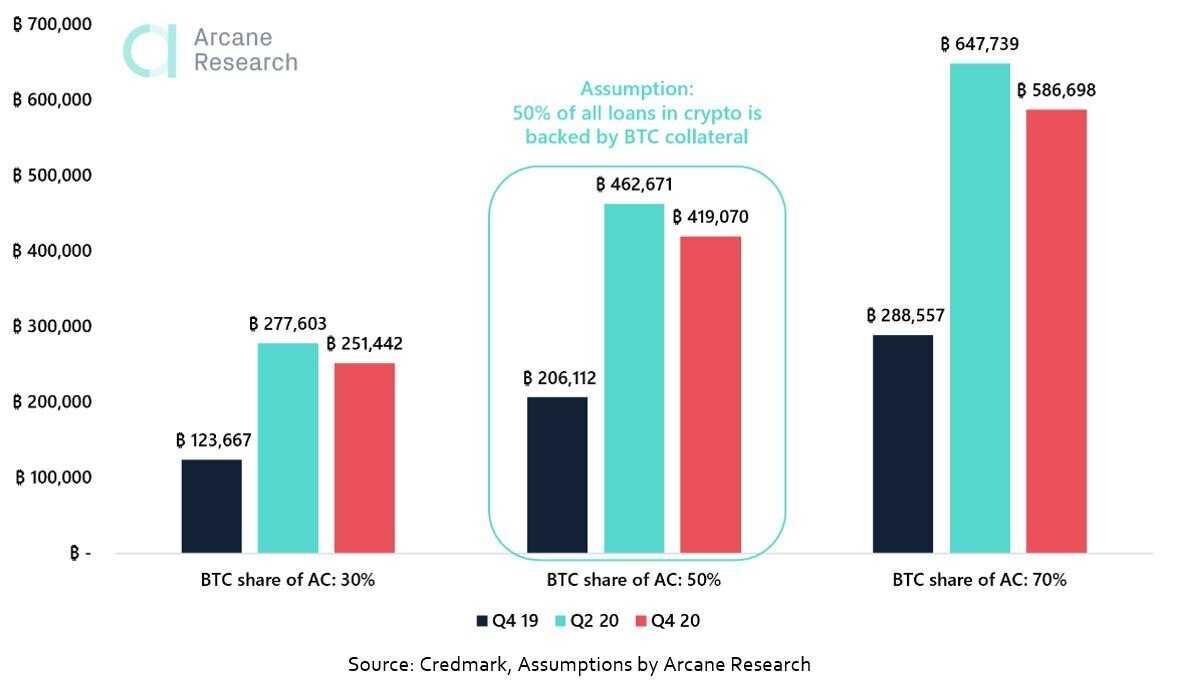

The mechanics of crypto lending rely on a simple but unforgiving equation: over-collateralization. Unlike traditional finance, where credit scores and cash flow determine borrowing power, decentralized lending platforms require borrowers to lock up digital assets worth more than the loan they receive. This buffer protects lenders against the extreme volatility inherent in the crypto market. If the value of the collateral drops too quickly, the system triggers a liquidation to recover the debt.

Liquidation thresholds are the heartbeat of this risk management model. Most platforms set a Loan-to-Value (LTV) ratio, typically between 70% and 80%. If the collateral value falls below this line, an automated process sells the assets to repay the loan. During periods of high volatility, these liquidations can cascade, creating a feedback loop where forced selling drives prices down further, triggering more liquidations. This dynamic was a primary driver of the 2022 market crash, where leveraged positions unwound simultaneously across multiple protocols.

Oracle failures represent another critical failure point. Lending platforms depend on decentralized oracles to fetch real-time asset prices. If an oracle is delayed, manipulated, or fails, the platform may not detect a collateral shortfall in time. While most major protocols have diversified oracle feeds to mitigate this risk, the reliance on external data sources remains a structural vulnerability. Understanding these mechanics is essential for anyone navigating the crypto lending market, as the stability of the entire ecosystem depends on the integrity of these automated safeguards.

Build a resilient crypto lending strategy

Constructing a resilient lending strategy requires balancing yield generation with strict risk mitigation. In a market where platform solvency and asset volatility can shift rapidly, diversification acts as the primary defense against single-point failures. Instead of concentrating capital in high-yield, unsecured loans, a robust approach spreads exposure across multiple protocols, asset classes, and custodial structures.

Step 1: Diversify across lending platforms and protocols

Relying on a single platform creates concentrated counterparty risk. Allocate capital across established centralized exchanges and decentralized finance (DeFi) protocols to mitigate the impact of any one entity’s failure. Coinbase Institutional notes that borrowing and lending markets operate across both decentralized and traditional financing rails, offering distinct risk profiles for each [The Lending Landscape - Coinbase Institutional Market Intelligence]. By splitting exposure, you ensure that a protocol-specific bug or regulatory action does not freeze your entire portfolio.

Spread capital between centralized lending desks and decentralized money markets. This structural separation protects against protocol-specific smart contract vulnerabilities or centralized insolvency events.

Step 2: Balance stablecoin and volatile asset exposure

Yield sources vary significantly by asset type. Stablecoins typically offer lower, more predictable returns (often 3%–10% annually) compared to volatile tokens, which carry higher yield potential but also higher liquidation risk [Is crypto lending profitable?]. A balanced portfolio might allocate 60-70% to stablecoin pools for baseline income, while reserving the remainder for volatile asset lending to capture beta-like yield during bull markets. This mix smooths out return volatility over time.

Mix stablecoin pools for steady, lower-risk yield with volatile asset lending for higher potential returns. This balance mitigates the impact of sudden market downturns on your overall income stream.

Step 3: Monitor collateralization ratios and liquidation thresholds

Security in lending is defined by collateralization. If the value of your crypto falls below a certain threshold, lenders may require you to add more collateral or repay part of the loan [How safe is crypto lending?]. For lenders, this means understanding the health of the underlying borrower pool. Prioritize platforms with over-collateralized positions and real-time liquidation mechanisms to ensure your principal is protected by sufficient asset backing.

Track the health factors of lending pools. Avoid pools with low collateralization ratios, as they are more susceptible to cascading liquidations during market volatility, which can erode your principal.

Step 4: Use live market data to adjust allocation

Static strategies fail in dynamic markets. Regularly review market conditions using live data to adjust your lending allocations. If interest rates on stablecoins drop significantly, consider rotating capital into other yield-generating opportunities or increasing your volatile asset exposure if market conditions permit. Use technical charts to identify broader market trends that may impact borrower demand and liquidity depth.

Use live market data to rebalance your portfolio. Rotate capital between stablecoin and volatile lending pools based on current interest rate spreads and broader market trends to maximize risk-adjusted returns.

Step 5: Verify platform security and regulatory compliance

Finally, prioritize platforms with transparent security audits and clear regulatory compliance. DeFi lending relies on smart contracts, which are immutable once deployed. Check for recent audit reports from reputable firms and assess the platform’s track record during previous market stress events. Regulatory clarity in your jurisdiction also reduces the risk of sudden platform shutdowns or asset freezes.

Audit platform security before depositing funds. Choose protocols with recent, reputable smart contract audits and transparent governance models to minimize the risk of technical failures or regulatory interventions.

Common questions about crypto lending

Crypto lending platforms operate by matching lenders with borrowers, creating a market where capital meets liquidity. Understanding the mechanics behind these transactions helps investors assess whether this asset class fits their risk profile.

No comments yet. Be the first to share your thoughts!