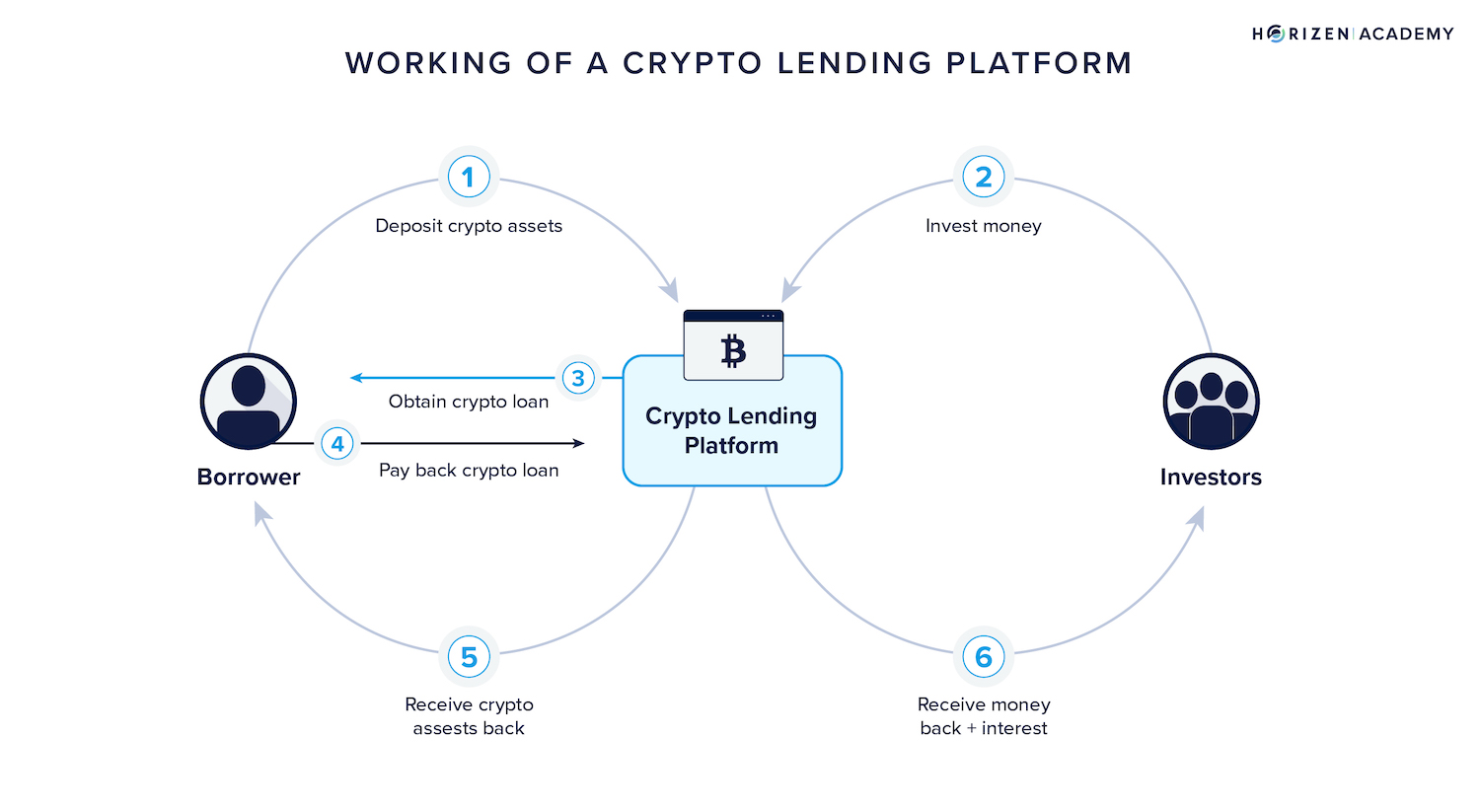

The two engines of crypto lending

Crypto lending has evolved from a niche DeFi experiment into a structured market with distinct yield sources. At its core, the practice is simple: one party lends cryptocurrency to another in exchange for compensation, a definition outlined by major exchanges like Coinbase. However, the mechanisms generating those returns have split into two primary categories: traditional crypto-backed loans and the emerging Real-World Asset (RWA) lending sector.

Traditional crypto-backed loans

In the traditional model, borrowers lock up volatile digital assets as collateral to secure loans. This structure creates a self-contained loop where the yield comes primarily from the interest paid by borrowers who need liquidity without selling their holdings. For lenders, this offers potentially high returns, but it carries significant exposure to the underlying asset's volatility. If the collateral value drops, liquidation events can trigger rapid market movements, making these yields sensitive to broader crypto market sentiment.

Real-World Asset (RWA) lending

RWA lending represents a bridge between decentralized finance and traditional finance. Instead of lending against crypto collateral, this model involves lending against tokenized real-world assets like treasury bills, private credit, or real estate. According to accounting frameworks like PwC’s Viewpoint, these transactions function similarly to traditional lending but operate on blockchain infrastructure. The yields here are generally derived from the cash flows of the underlying real-world asset, offering a different risk profile that is often less correlated with crypto price swings.

Understanding this distinction is critical for anyone evaluating a crypto lending guide. The "yield" you see is not a single metric; it is a reflection of the underlying risk and the source of the cash flow. Whether you are attracted to the high-octane returns of crypto-backed loans or the stability of RWA protocols, recognizing where the money comes from is the first step in managing risk.

How real-world assets fuel crypto lending yields

Real-world asset (RWA) lending represents a structural shift in how yield is generated within the crypto lending ecosystem. Instead of relying solely on speculative trading or volatile interest rate markets, platforms are tokenizing traditional financial instruments. This process bridges the gap between decentralized finance (DeFi) and institutional-grade assets, creating a more stable yield source for participants in the crypto lending landscape.

The most prominent example is tokenized treasury bills. By on-chain tokenizing short-term US government debt, platforms can offer yields that closely track risk-free rates, minus the operational friction of traditional banking. This appeals to institutions seeking predictable returns without leaving the blockchain. Similarly, private credit involves tokenizing loans to real-world businesses. These loans often carry higher interest rates than treasuries, providing a premium yield layer that distinguishes them from generic DeFi lending pools.

Institutions are increasingly shifting capital into these RWA lending mechanisms for two primary reasons: stability and regulatory clarity. Traditional finance firms are looking for ways to deploy capital on-chain without exposing themselves to the extreme volatility of unbacked crypto assets. RWA lending offers a middle ground, combining the transparency of blockchain with the tangible collateral of real-world debt. This trend is accelerating as major financial players recognize the efficiency of tokenized assets in reducing settlement times and counterparty risk.

To understand the broader market context influencing these yields, it is useful to look at the underlying asset performance. The correlation between crypto market cycles and traditional lending rates highlights the beta exposure of these strategies.

Infrastructure and counterparty risks

Crypto Lending works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Due diligence checklist for lenders

Before parking assets on a platform, you need a framework that separates marketing hype from actual solvency. A high-yield rate is rarely free; it’s a risk premium. Your job is to ensure the platform isn’t simply hiding insolvency behind that yield. When evaluating a crypto lending guide or a specific provider, focus on three non-negotiable pillars: audit history, reserve transparency, and legal jurisdiction.

Do not accept internal attestations as proof of solvency. Look for recent, full-scope audits from reputable firms like PwC, KPMG, or Deloitte. These firms provide rigorous assurance on the platform’s financial statements and internal controls. A simple "attestation" report is often limited to specific controls and may not cover the full reserve. If the audit is older than 12 months or from an unknown boutique firm, treat the platform as high-risk. PwC’s research on crypto assets highlights the importance of accurate accounting for these transactions, making their audit standards a reliable benchmark for safety.

Static PDF reports are outdated the moment they are published. The safest platforms use real-time proof-of-reserves (PoR) dashboards that allow you to verify your specific deposit against the total pool. This dashboard should show on-chain balances of the platform’s hot and cold wallets compared to user liabilities. If the platform only offers monthly or quarterly snapshots, you are flying blind. Real-time data allows you to see if the platform is engaging in risky lending practices that exceed its liquid assets.

Where is the entity legally registered, and does it hold a license? Platforms operating in regulated jurisdictions like New York (BitLicense), Switzerland, or the EU (MiCA) are subject to capital reserve requirements and consumer protection laws. An entity registered in an offshore haven with no clear regulatory oversight offers little recourse if things go wrong. Check if the platform is a registered Money Services Business (MSB) with FinCEN in the US or equivalent bodies elsewhere. This legal layer is your only safety net in a bankruptcy scenario.

The chart above shows Coinbase’s stock performance, a publicly traded crypto giant. While not a direct competitor to all lending platforms, its public reporting requirements and market scrutiny serve as a proxy for the level of transparency you should demand from any custodian. If a private lending platform cannot match the transparency of a public company like Coinbase, the risk of hidden leverage is significantly higher.

When assessing risk, always keep the underlying asset price in mind. Volatility can trigger liquidations even on well-audited platforms. Use live price data to understand the current market pressure on collateralized loans.

Frequently asked questions about crypto lending

Crypto lending offers a way to generate yield on idle assets, but it requires understanding both the mechanics and the risks involved. Below are answers to the most common questions regarding profitability and entry methods.

No comments yet. Be the first to share your thoughts!