How crypto lending works

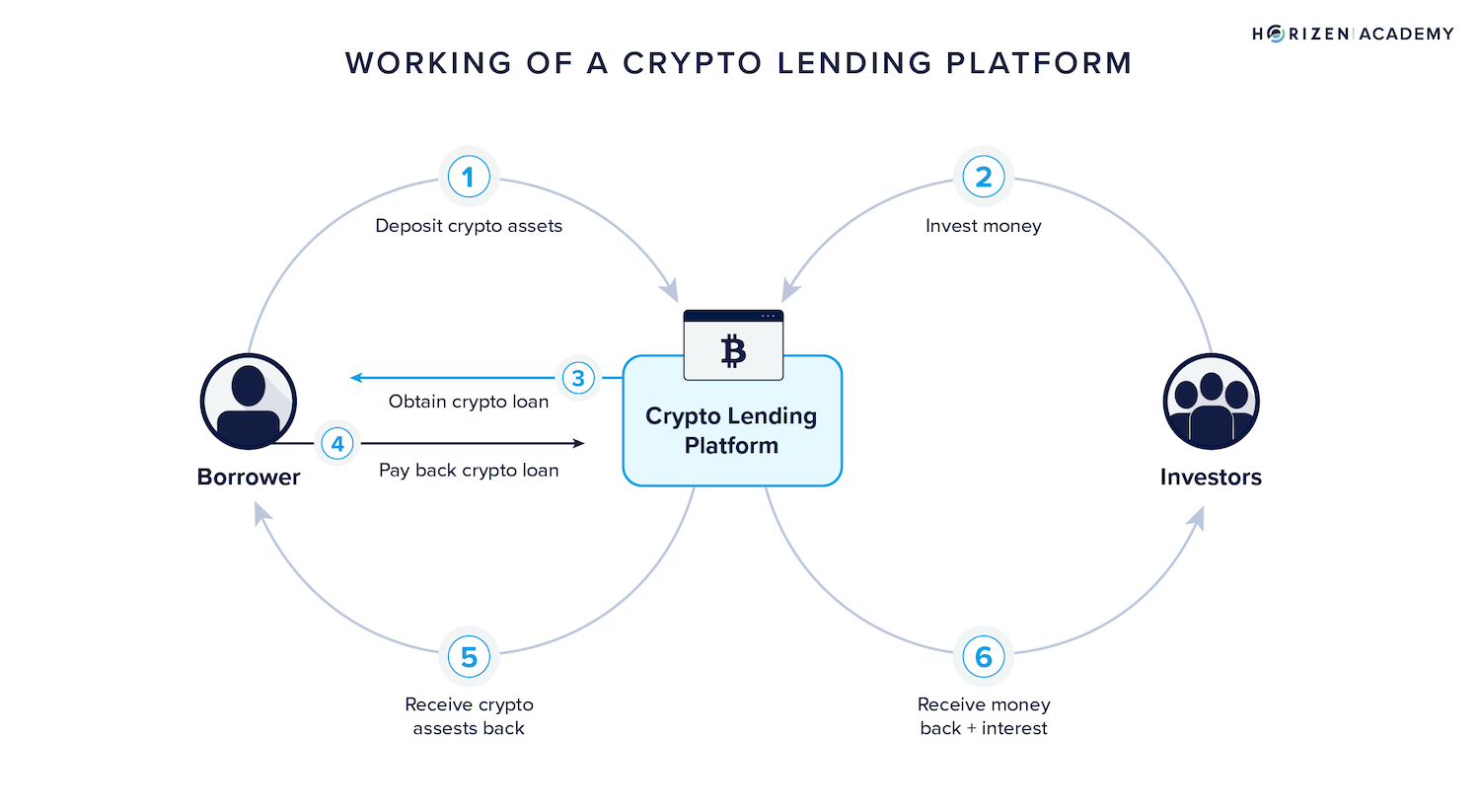

Crypto lending is a financial transaction where one party lends cryptocurrency to another party in exchange for compensation. At its core, it mirrors traditional banking: you deposit assets, and a borrower uses them, paying interest on top. However, the infrastructure behind these transactions splits into two distinct camps. Understanding the difference between centralized exchanges and decentralized protocols is essential for managing risk and yield in 2026.

Centralized Lending Platforms

Centralized platforms, such as Coinbase or Binance, act as the middleman. You deposit your crypto into the exchange’s wallet, and they lend it out to institutional borrowers, margin traders, or other users. The platform sets the interest rates and manages the risk. This model offers convenience and customer support, but it introduces counterparty risk. If the exchange fails or faces regulatory action, your funds may be frozen or lost. You are trusting a single company with custody of your assets, similar to keeping money in a bank account.

Decentralized Lending Protocols

Decentralized finance (DeFi) protocols remove the middleman. Instead of a company, smart contracts on a blockchain automate the lending process. You deposit assets into a liquidity pool, and borrowers borrow directly from that pool by providing collateral. Interest rates are determined algorithmically by supply and demand within the protocol. This model offers transparency and control, as you can often withdraw your funds instantly. However, it requires a deeper understanding of blockchain mechanics and exposes you to smart contract risk—bugs in the code could lead to exploits.

The Role of Volatility

Crypto lending is heavily influenced by the underlying asset’s price movements. Lenders must account for volatility, which can erode real returns or trigger liquidations for borrowers. For context, consider the price action of Bitcoin, the most commonly lent asset.

Choosing Your Path

Your choice between centralized and decentralized lending depends on your risk tolerance and technical comfort. Centralized platforms are better for beginners who prioritize ease of use and fiat on-ramps. Decentralized protocols suit experienced users seeking higher yields and custody control. Regardless of the path, always verify the platform’s security history and insurance coverage before depositing significant capital.

Yield sources and risk tiers

Crypto Lending works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

CeFi vs. DeFi: Custody and Counterparty Risk

Choosing a crypto lending platform requires understanding who actually holds your assets. The structural divide between centralized exchanges (CeFi) and decentralized protocols (DeFi) dictates your exposure to counterparty risk and custody failure. This choice determines whether you rely on a company’s solvency or the mathematical certainty of a smart contract.

Centralized Finance (CeFi)

CeFi platforms operate like traditional banks. You deposit your cryptocurrency into a wallet controlled by the platform, and they lend it out to institutional borrowers or use it for proprietary trading. In this model, you are an unsecured creditor. If the platform mismanages funds or faces a liquidity crisis, your assets are at risk. The 2022 collapse of Celsius Network and the bankruptcy of FTX demonstrated the severe consequences of commingled funds and opaque risk management.

The primary advantage of CeFi is ease of use. These platforms often offer higher yields than DeFi because they can lend to sophisticated borrowers who cannot interact with on-chain protocols. However, this convenience comes with significant counterparty risk. You must trust the platform’s internal controls, regulatory compliance, and capital reserves. "Not your keys, not your coins" is not just a slogan here; it is a warning. When you lend on CeFi, you surrender custody, and the platform becomes the sole point of failure.

Decentralized Finance (DeFi)

DeFi lending protocols operate through smart contracts on public blockchains. You interact directly with the code, depositing assets into a liquidity pool or a collateralized debt position (CDP). You retain custody of your private keys until the moment of transaction, and the protocol executes loans without a central intermediary. This eliminates counterparty risk in the traditional sense, as there is no company that can go bankrupt or freeze your assets arbitrarily.

The trade-off is complexity and smart contract risk. While you avoid institutional failure, you are exposed to code vulnerabilities. A bug in the protocol could lead to a hack or exploit. Additionally, DeFi yields are often lower for stablecoins due to the transparent nature of the markets, though volatile tokens can offer higher returns. The lack of a central entity also means there is no customer support to recover lost funds or resolve disputes. Your security depends entirely on your ability to manage keys and verify contract audits.

Key Differences at a Glance

| Feature | CeFi Lending | DeFi Lending |

|---|---|---|

| Custody | Platform holds keys | User holds keys; protocol holds assets |

| Counterparty Risk | High (Company solvency) | Low (Code reliability) |

| Regulation | Regulated entities | Unregulated / Code is law |

| Yield Potential | Often higher (Opaque lending) | Market-driven (Transparent) |

| Recovery | Possible (Bankruptcy claims) | None (Irreversible transactions) |

Choosing the Right Model

Your choice should align with your risk tolerance and technical comfort. If you prioritize simplicity and are willing to accept counterparty risk for potentially higher yields, CeFi may suit you. However, if you value sovereignty and want to eliminate the risk of a centralized platform failing, DeFi is the safer structural choice, provided you understand the smart contract risks. For most investors, a diversified approach—using CeFi for convenience and DeFi for core holdings—can balance accessibility with security.

Key risks in the current market

Crypto lending offers yield, but the infrastructure remains fragile. The 2026 market environment demands a clear-eyed view of three specific threats: liquidation cascades, smart contract flaws, and shifting regulatory rules. Ignoring these risks can turn passive income into total capital loss.

Liquidation cascades

Lending protocols rely on over-collateralization to manage risk. When asset prices drop rapidly, borrowers face margin calls. If they cannot add collateral, their positions are liquidated. This forced selling drives prices down further, triggering more liquidations in a feedback loop known as a cascade.

This mechanism worked against the market in 2022, wiping out billions in value. While protocols have improved liquidation engines since then, sudden volatility can still overwhelm safeguards. Lenders must understand that their capital is exposed to the health of the entire borrowing ecosystem, not just the value of their specific deposit.

Smart contract vulnerabilities

Most crypto lending happens through code. Smart contracts are immutable once deployed, meaning bugs cannot be patched without a governance vote or hard fork. A single vulnerability can lead to a "rug pull" or total drain of the protocol's liquidity.

Even audited contracts carry risk. Audits are snapshots in time; they do not guarantee future safety. Developers must constantly monitor for new exploit vectors, and lenders should prefer protocols with proven track records and transparent security practices over those offering unusually high yields.

Regulatory shifts

The legal landscape for crypto lending is evolving. Regulators in the US, EU, and Asia are increasingly scrutinizing lending platforms, particularly regarding consumer protection and systemic risk. New rules could restrict yield-bearing products, limit stablecoin lending, or force platforms to hold higher capital reserves.

Compliance costs may reduce the yields available to lenders. In extreme cases, regulatory action could freeze assets or shut down platforms entirely. Lenders should diversify across jurisdictions and avoid concentrating capital in platforms that operate in legal gray areas.

Steps to start lending safely

Before deploying capital, you must treat crypto lending like any other financial instrument: verify the counterparty and secure the access. This workflow prioritizes security due diligence and platform selection to protect your yield strategies for 2026.

Start by auditing the platform’s security posture. Look for third-party security audits, proof of reserves, and insurance coverage for smart contract vulnerabilities. Avoid platforms that cannot provide transparent, recent audit reports from reputable firms. Check if they offer multi-signature wallets or cold storage solutions for user funds.

Choose a lending platform that aligns with your risk tolerance. Established exchanges like Coinbase often provide a baseline of regulatory compliance and customer support, which can be crucial for beginners. Ensure the platform supports the specific assets you intend to lend and clearly discloses the terms, including lock-up periods and early withdrawal penalties.

Enable two-factor authentication (2FA) using an authenticator app, not SMS. Set up withdrawal whitelists to prevent unauthorized transfers. Use a unique, strong password stored in a password manager. Regularly review account activity logs for any suspicious logins or transactions.

Before committing significant capital, deposit a small amount to test the lending process. Verify that the interest accrues correctly and that you can withdraw your principal and earnings without unexpected delays or hidden fees. This step confirms the platform’s operational reliability.

| Feature | Centralized | Decentralized |

|---|---|---|

| Custody | Platform holds keys | User holds keys |

| Regulation | Often regulated | Generally unregulated |

| Insurance | Sometimes available | Rarely available |

Key Takeaways

- Prioritize platforms with transparent audits and clear terms.

- Secure your account with 2FA and withdrawal whitelists.

- Test the system with a small deposit before scaling up.

Frequently asked: what to check next

Is crypto lending profitable?

Profitability depends on the asset and platform. Lending stablecoins typically yields 3% to 10% annually, while volatile tokens offer higher returns with greater risk.

How do I start crypto lending?

Choose a reputable lending platform, deposit your cryptocurrency, and set your lending terms, including interest rates and duration.

What are the risks of crypto lending?

Risks include platform insolvency, smart contract failures, and collateral liquidation during market downturns. Always research the platform’s security history.

No comments yet. Be the first to share your thoughts!