How to research the crypto lending market

Analyzing the crypto lending market requires looking past headline yields to understand the underlying infrastructure shifts. The sector is no longer just about simple interest-bearing accounts; it is a complex ecosystem of decentralized finance protocols, centralized exchanges, and on-chain lending markets. In Q3 2025, lending applications accounted for more than 80% of the onchain market, while collateralized debt positions (CDPs) held just 16%, a sharp contrast to the 53% CDP dominance seen in late 2021 Galaxy Research. This structural change means your research must focus on where liquidity is actually flowing.

Start by tracking total value locked (TVL) across major lending protocols. This metric reveals which platforms are gaining trust and liquidity. Look for platforms that maintain high utilization rates without triggering excessive liquidation risks. A healthy lending market balances borrower demand with lender supply. If utilization is too low, yields will be unattractive. If it is too high, the risk of protocol insolvency rises.

Next, evaluate the collateral assets being used. The crypto-backed lending market reached a new all-time high of $73.6 billion in Q3 2025 LoanPro. Much of this growth was driven by Bitcoin and Ethereum collateral. Research the specific risk parameters of each asset. Some protocols accept volatile altcoins, while others stick to blue-chip assets. Understanding these differences helps you assess the stability of the lending environment.

Finally, consider the regulatory landscape. The IMF has issued guidance on recording crypto lending in macroeconomic statistics, highlighting the growing integration of these assets into traditional finance IMF. Regulatory clarity can impact platform accessibility and yield sustainability. Keep an eye on jurisdictional changes that might affect liquidity providers and borrowers alike.

Crypto lending market research choices that change the plan

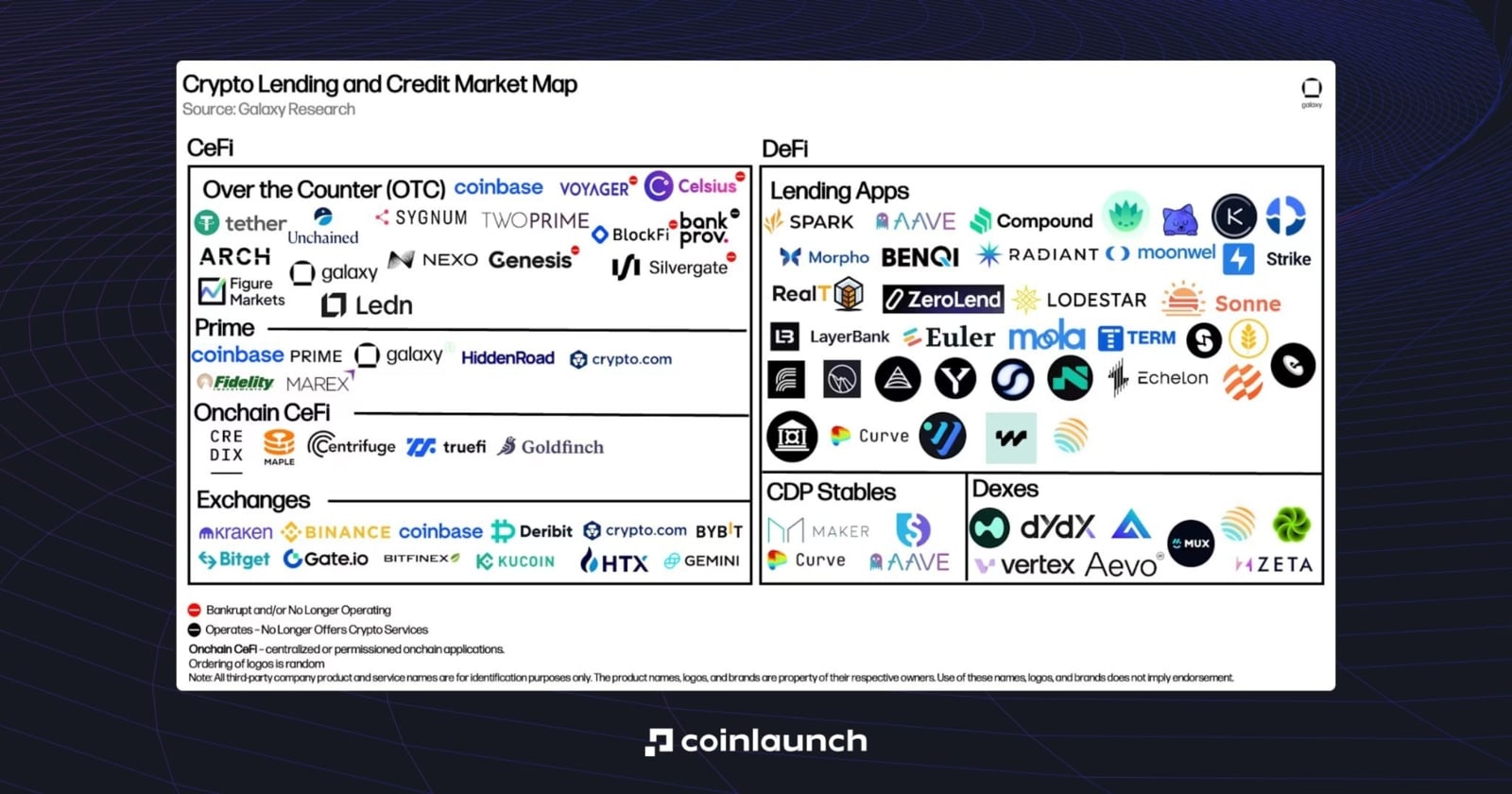

Evaluating the crypto lending market requires looking past headline yields to the structural risks embedded in the platform’s architecture. The sector has shifted significantly from the opaque, centralized models of the past toward on-chain protocols with transparent collateralization, yet the tradeoffs between yield, safety, and liquidity remain complex. Recent data from Galaxy Research highlights that lending applications now account for more than 80% of the on-chain market, a sharp rise from just 53% in late 2021, indicating a maturation in how digital assets are utilized for leverage and yield generation [[src-serp-1]].

When comparing platforms, the primary decision involves balancing the risk of smart contract failure against the convenience of centralized custody. Decentralized Finance (DeFi) protocols offer transparency and non-custodial control but expose users to code vulnerabilities and impermanent loss in liquidity pools. In contrast, Centralized Finance (CeFi) entities provide familiar user interfaces and customer support but reintroduce counterparty risk, as seen in historical platform collapses. Investors must assess whether the extra yield from a DeFi pool justifies the technical complexity and audit risk compared to the regulatory safeguards of a regulated CeFi lender.

To visualize these tradeoffs, compare the key operational differences between major lending structures:

| Feature | DeFi Protocol | CeFi Platform | Hybrid Model |

|---|---|---|---|

| Custody | Non-custodial (user holds keys) | Custodial (platform holds keys) | Mixed (stablecoins custodial, crypto non-custodial) |

| Transparency | On-chain, real-time | Audited reports, delayed | Partial on-chain visibility |

| Yield Source | Protocol fees + incentives | Interest from institutional borrowers | Combination of both |

| Regulatory Risk | Low (code is law) | High (license dependency) | Moderate (jurisdiction dependent) |

Beyond the platform type, the specific asset class and collateral type drive the risk profile. Bitcoin-backed loans have seen a surge, with the broader crypto lending market hitting a record $73.6 billion in Q3 2025 [[src-serp-4]]. However, this growth has exposed a "collateral gap" where the quality of underlying assets varies wildly. Lenders must scrutinize whether the platform accepts volatile altcoins as collateral, which increases liquidation risk during market downturns, or sticks to blue-chip assets like Bitcoin and Ethereum. The choice of collateral directly impacts the loan-to-value (LTV) ratio and the likelihood of forced liquidations.

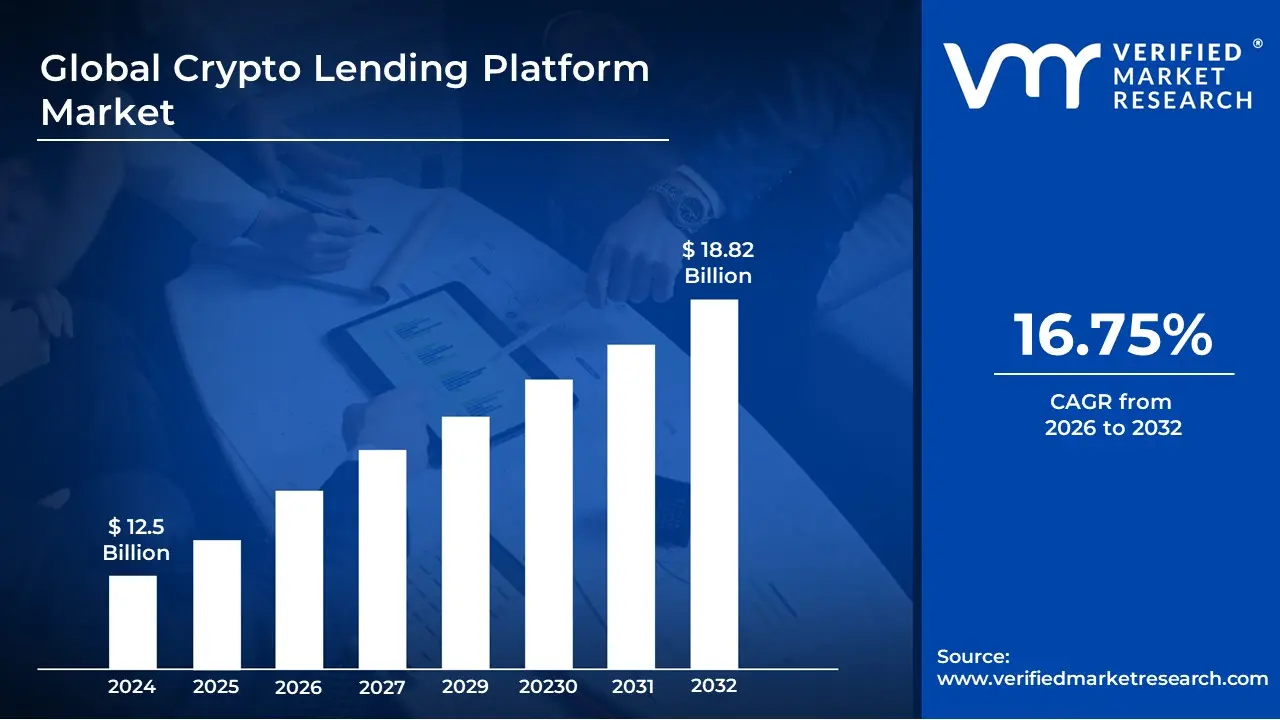

Market expansion is undeniable, with the crypto lending platform market valued at $12.69 billion in 2026 and projected to reach $25.06 billion by 2030 [[src-serp-3]]. This growth is fueled by institutions seeking yield on idle crypto assets without selling their positions. However, this influx of capital has also attracted sophisticated borrowers who may engage in complex leverage strategies, potentially destabilizing the lending pool during high-volatility events. Understanding these dynamics is essential for anyone looking to participate in this high-stakes market.

Choose the next step

Crypto Lending Market Research works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Spotting Weak Options in Crypto Lending

The crypto lending market hit $73.6 billion in Q3 2025, but the surge in volume masks several structural traps for retail lenders and borrowers alike. Many platforms market high yields while hiding the risk concentration in their balance sheets. Identifying these weak options requires looking past the headline APY to the underlying collateral mechanics and platform transparency.

Misleading "Guaranteed" Yields

Many platforms advertise fixed, high-interest returns that appear risk-free but are actually subsidized by volatile trading revenue or unsustainable liquidity pools. These yields often collapse when market volatility spikes or when the platform’s proprietary trading desk faces losses. Always check if the yield is backed by real borrower interest or internal subsidies. If a platform cannot clearly explain the source of its interest payments, treat the rate as speculative rather than income.

Collateral Liquidation Traps

Borrowers often underestimate how quickly their positions can be liquidated during market dips. Some platforms use aggressive liquidation thresholds that trigger sales before the collateral value actually drops below the loan value, especially during flash crashes. This creates a negative feedback loop where forced selling drives prices down further. Look for platforms with dynamic liquidation buffers and transparent oracle data feeds to avoid sudden, unexpected losses.

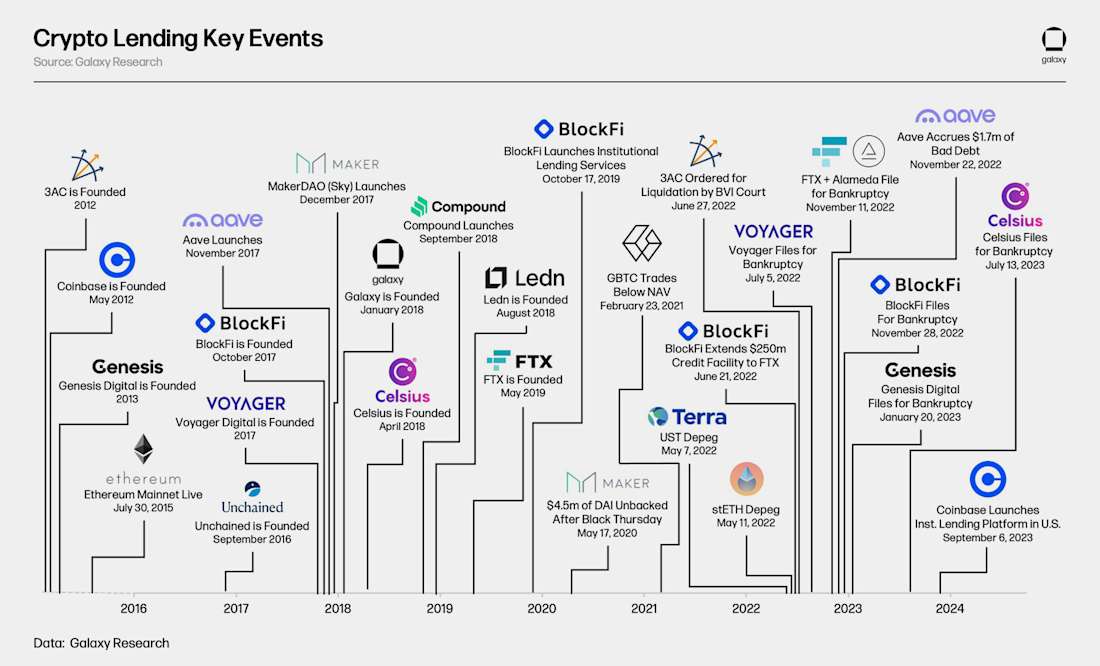

Counterparty Risk in CeFi Models

Centralized crypto lending (CeFi) platforms hold your assets in custodial wallets, meaning you rely entirely on the platform’s security and solvency. Unlike decentralized finance (DeFi), where smart contracts enforce rules, CeFi risks include insider theft, regulatory seizure, or bankruptcy. The 2022 collapses of major CeFi lenders demonstrated that even "audited" platforms can fail. Prioritize platforms with regular, third-party proof-of-reserves audits and segregated customer funds.

Regulatory and Compliance Gaps

Many lending platforms operate in regulatory gray areas, exposing users to sudden service shutdowns or frozen assets. Without clear compliance frameworks, platforms may freeze withdrawals during regulatory investigations, leaving lenders unable to access their principal. Check if the platform is registered with relevant financial authorities and adheres to anti-money laundering (AML) standards. Regulatory clarity is not just a legal formality; it is a critical indicator of platform stability and long-term viability.

Crypto lending market research: what to check next

Before committing capital to crypto lending, it helps to understand the mechanics, scale, and risks involved in the current market. The following answers address the most common questions from investors and borrowers.

Understanding these fundamentals provides a clearer picture of where crypto lending fits into a broader investment strategy.

No comments yet. Be the first to share your thoughts!