Crypto lending market research budget

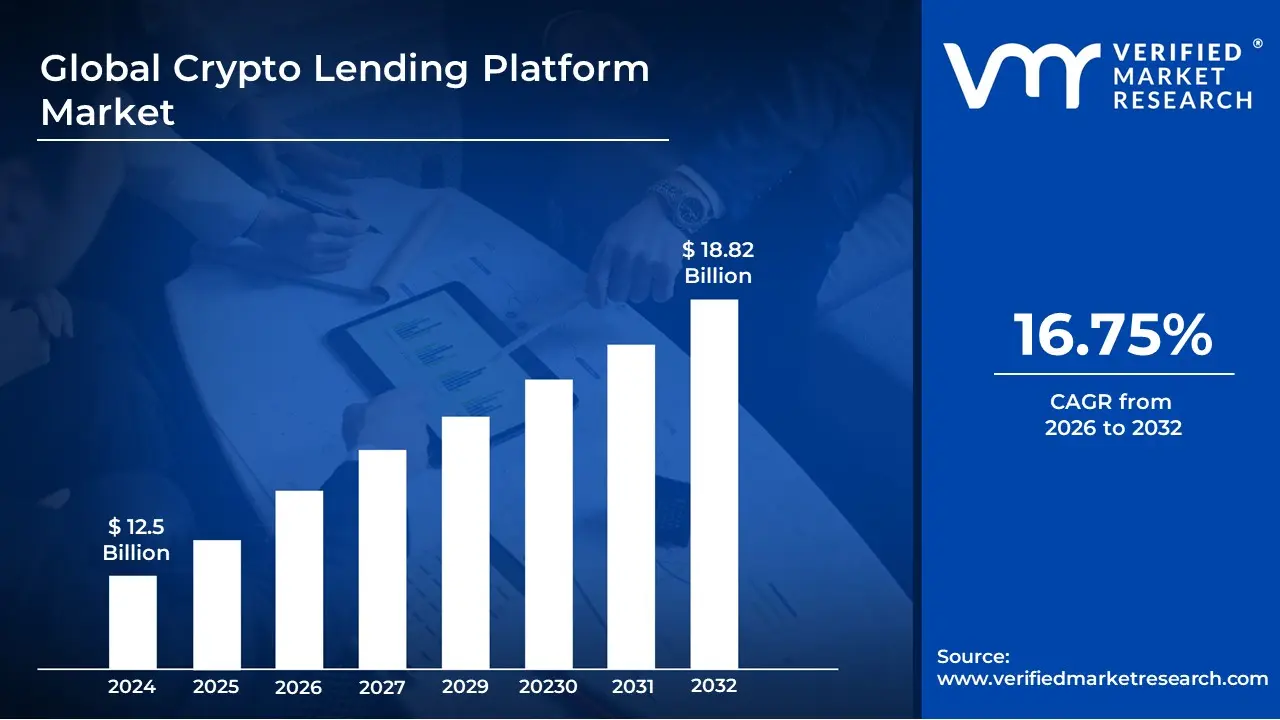

The crypto lending market hit an all-time high of $73.6 billion in Q3 2025, driven by a shift from speculative collateralized debt positions toward pure lending applications [src-serp-2]. This growth isn't just about volume; it's about infrastructure. Lending now accounts for over 80% of the onchain market, leaving traditional crypto-backed loans behind [src-serp-1]. For investors, this means the "budget" for lending is no longer a binary choice between centralized exchanges and decentralized protocols, but a spectrum of yield-generating tools.

When building a lending portfolio, you must account for the tradeoffs between yield, risk, and liquidity. Centralized platforms often offer higher, fixed rates but introduce counterparty risk, while DeFi protocols offer transparency and non-custodial control but fluctuate with market volatility. The best approach is a diversified budget that allocates capital across both environments, balancing the convenience of centralized lending with the composability of decentralized finance.

Below are three essential hardware tools for securing your crypto assets. While these aren't lending protocols themselves, they are the foundational infrastructure for anyone managing significant crypto holdings in a lending environment. Losing your private keys means losing access to your lending yields, making hardware security a non-negotiable part of your lending budget.

As an Amazon Associate, we may earn from qualifying purchases.

As you evaluate lending strategies, remember that the market is evolving rapidly. What was true in Q4 2021 is largely obsolete today. Focus on protocols with audited smart contracts, transparent reserve proofs, and sustainable yield models rather than chasing unsustainable APYs. The goal is consistent, risk-adjusted returns, not speculative gambling.

Compare the strongest crypto lending market research options

Choosing the right data source depends on whether you need real-time on-chain metrics or broader market context. Galaxy Research provides the macro view, tracking total outstanding debt and collateral types across the ecosystem. TheBlock offers granular protocol-level data, essential for monitoring specific platform health.

For traders, live price action matters. Use the widget below to track Bitcoin, the primary collateral asset for most lending positions. The table below compares the primary research tools. Galaxy excels at historical trends and institutional leverage, while TheBlock focuses on current TVL and liquidation risks.

| Source | Primary Focus | Data Depth | Best For |

|---|---|---|---|

| Galaxy Research | Macro leverage trends | High-level market metrics | Understanding sector-wide debt cycles |

| TheBlock | Protocol TVL & debt | Real-time on-chain metrics | Monitoring specific platform health |

| Hedera Learning | DeFi mechanics | Educational overview | Beginners learning lending basics |

Galaxy’s Q3 2025 report highlights that lending applications now dominate on-chain markets, accounting for over 80% of activity. This shift away from collateralized debt positions (CDPs) signals a maturing infrastructure. TheBlock’s data complements this by showing how Aave and MakerDAO handle these volumes daily.

Inspect the expensive parts

The crypto lending market hit a record $73.6 billion in Q3 2025, but that volume masks significant infrastructure risks. When capital is this deep in the system, a single smart contract vulnerability or oracle failure can erase value faster than market volatility. You need a practical inspection checklist to identify where the expensive failure points lie before committing funds.

Start with the code. Lending applications now account for over 80% of the onchain lending market, far outpacing other derivatives. Check if the protocol has undergone independent audits from reputable firms. Look for active bug bounty programs and time since the last security review. Unaudited code is a guaranteed failure point.

Your collateral value depends entirely on price feeds. If an oracle is manipulated, you could be liquidated instantly or the protocol could become insolvent. Check which oracle network the protocol uses. Prefer decentralized oracle networks like Chainlink over single-source feeds. Verify the latency and update frequency of the price data.

Liquidations are the safety valve of lending protocols. If they fail during a crash, the entire system can collapse. Examine the liquidation threshold and bonus structure. A low bonus might discourage liquidators, leaving bad debt. Check historical liquidation data to see if the protocol handles flash crashes gracefully or if it stalls.

As an Amazon Associate, we may earn from qualifying purchases.

The infrastructure holding your capital must be robust. By systematically checking these three areas—code, oracles, and liquidations—you can avoid the most common and expensive pitfalls in the current lending landscape.

Ownership costs and hidden maintenance expenses

A low loan-to-value (LTV) ratio or a competitive interest rate looks attractive on paper, but the actual cost of holding crypto debt often hides in maintenance fees, liquidation buffers, and gas overhead. When borrowing against volatile assets, the price of capital is only half the equation. The other half is the operational friction that erodes your margin over time.

The cost of volatility buffers

Most lending protocols require you to post collateral well above the minimum threshold to avoid immediate liquidation. This "over-collateralization" is a safety feature for lenders, but an opportunity cost for borrowers. If you lock $10,000 in ETH to borrow $5,000 in USDC, that remaining $5,000 in ETH is idle. It earns nothing while you pay interest on the borrowed stablecoin. In a bull market, this is the most significant hidden cost: the foregone appreciation of your locked assets.

Liquidation penalties and gas wars

When the market turns, the cost of exiting a position spikes. If your collateral value drops below the protocol’s health factor, liquidators step in. These agents are incentivized by a liquidation bonus (typically 5-10% of the collateral value), which is taken directly from your position. Additionally, during high-volatility events, network congestion drives up transaction fees. Trying to repay a loan or add collateral during a crash can cost significantly more in gas than in normal conditions, eating further into your capital.

Maintenance and monitoring overhead

DeFi lending is not "set and forget." It requires active monitoring of interest rate models, which can shift from fixed to variable based on utilization rates. If a protocol’s utilization hits 80%, borrowing costs can jump overnight. Without automated alerts or manual oversight, you may find yourself paying premium rates for weeks before adjusting your strategy. This time cost is real, especially for smaller positions where the effort to manage outweighs the potential yield.

When a cheap buy stops being cheap

The cheapest upfront loan is often the most expensive in the long run if it lacks flexibility. Fixed-rate loans protect against rising rates but may come with higher initial premiums. Variable rates start lower but can spiral during high demand. Always calculate the total cost of ownership (TCO) by adding the interest rate, liquidation buffer opportunity cost, and estimated gas fees. If the spread between your borrowing cost and your asset’s yield doesn’t comfortably cover these variables, the loan may not be worth the risk.

As an Amazon Associate, we may earn from qualifying purchases.

Crypto lending market research: what to check next

Before committing capital to crypto lending, it helps to separate the hype from the actual mechanics of yield and risk. The landscape has shifted significantly in 2025, moving away from opaque centralized platforms toward on-chain transparency, but the core trade-offs remain. Below are the most common practical questions readers ask when evaluating this sector.

No comments yet. Be the first to share your thoughts!