The crypto lending strategy limits to account for

The core tension in crypto lending today is that higher yields usually demand higher infrastructure risk. This constraint forces a choice between the safety of established centralized platforms and the transparency of decentralized protocols. Understanding this tradeoff is the foundation of any 2026 lending strategy.

Centralized Lending Platforms

Centralized exchanges (CEXs) offer the simplest entry point. You deposit assets and earn interest while the platform handles custody and matching. The downside is counterparty risk: if the platform fails, your assets may be frozen or lost. This model relies on traditional financial safeguards, which often lag behind crypto innovation.

Decentralized Finance (DeFi) Protocols

DeFi lending uses smart contracts to match lenders and borrowers without an intermediary. You retain custody of your assets until they are locked in the protocol. While this reduces counterparty risk, it introduces smart contract risk. A bug in the code can lead to total loss, making due diligence on the protocol’s audit history essential.

Crypto-Backed Loans

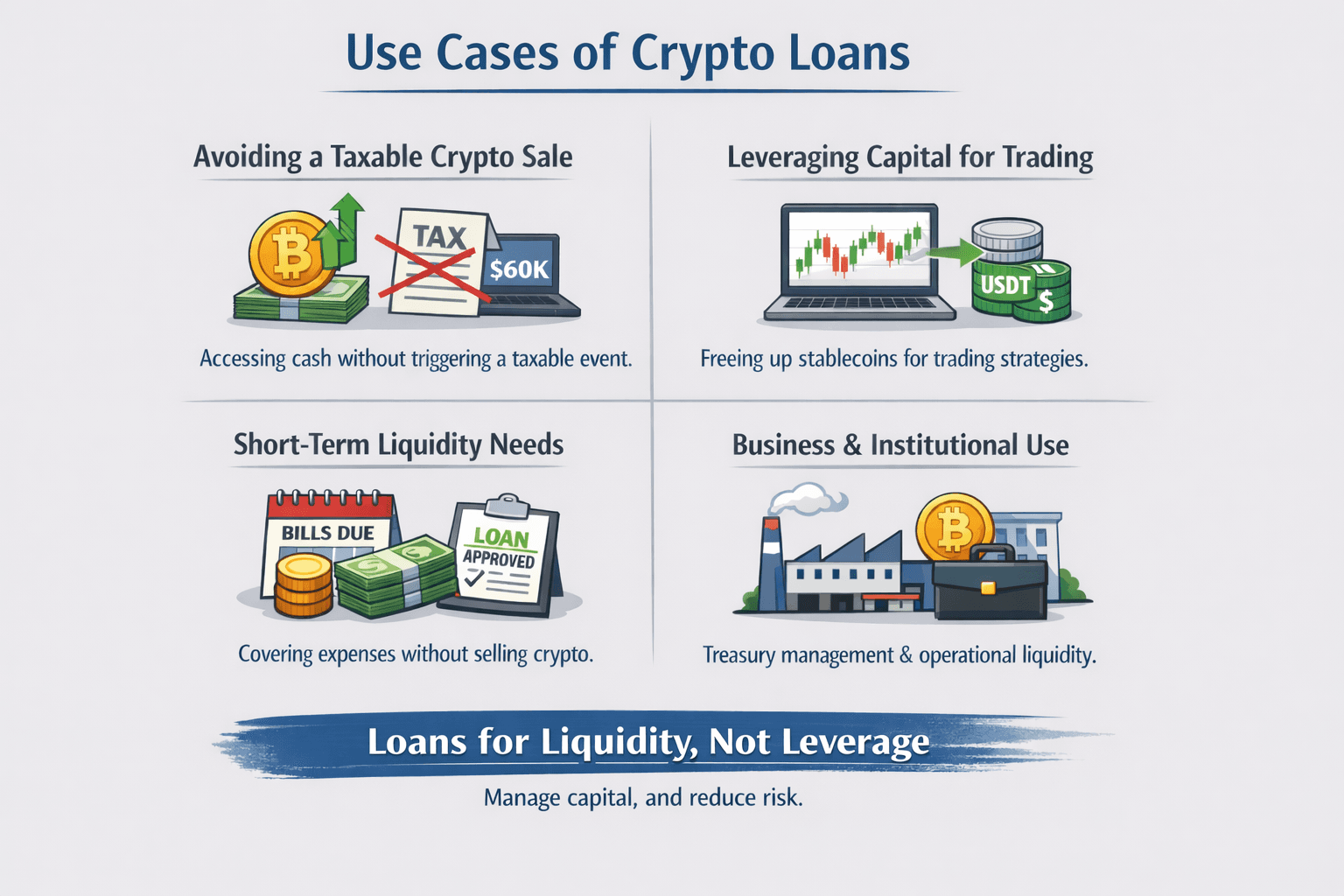

Instead of lending out your assets, you can borrow against them. This strategy allows you to access liquidity without selling your crypto holdings, avoiding immediate tax events. However, you must maintain a sufficient collateral ratio. If the value of your collateral drops, you risk a liquidation, where the protocol sells your assets to cover the loan.

Real-World Asset (RWA) Yields

The emerging trend involves tokenizing real-world assets like treasury bills or real estate. These assets often provide stable, lower-yield returns compared to volatile crypto lending. They offer a hedge against crypto market swings but come with their own regulatory and liquidity constraints. This segment is growing but remains less liquid than pure crypto lending.

The Safety and Profitability Question

Is crypto lending profitable? Yes, but returns vary widely based on risk tolerance. How safe is it? Safety depends entirely on the counterparty—whether it’s a company or a codebase. To make money, you must balance yield with the likelihood of principal loss. The most robust strategies often diversify across these different lending modes.

Crypto lending strategy choices that change the plan

Use this section to make the Crypto Lending Strategy decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Build a Crypto Lending Strategy

To manage the risks of real-world asset yields and infrastructure fragility, you need a concrete framework. Crypto lending offers liquidity without selling assets, but it exposes you to platform security gaps and volatile collateral values. This section outlines the five essential checks to build a resilient lending position.

DeFi and centralized platforms require overcollateralization. You must borrow less than the value of the crypto you pledge. A typical ratio is 150%, meaning you borrow $100 against $150 in assets. This buffer prevents immediate liquidation if the asset price drops. Always check the platform’s specific liquidation threshold before depositing.

Security is the primary risk. Look for platforms with published, recent audits from reputable firms like CertiK or OpenZeppelin. For centralized lenders, check if they publish proof of reserves. Avoid platforms with opaque balance sheets or those offering yields that seem detached from market interest rates, as these often signal unsustainable lending models.

Do not concentrate your entire portfolio in one protocol or chain. Smart contract bugs or network congestion can freeze assets. Spread your lending capital across at least three different protocols and, if possible, multiple blockchains. This reduces the impact of a single point of failure on your overall strategy.

Lending rates fluctuate based on supply and demand. High yields often attract more borrowers, driving rates up, but they can also signal higher risk. Set alerts for rate changes. If you are borrowing, lock in fixed rates if available to protect against sudden spikes. If you are lending, be prepared for APYs to drop as the market saturates.

Ensure you can withdraw your assets or repay loans quickly. Check withdrawal limits and processing times. In a market crash, platforms may impose withdrawal delays to prevent bank-run scenarios. Having a clear exit plan ensures you can reduce exposure before liquidity dries up or collateral values plummet.

The Weak Options to Avoid

Not every lending product delivers on its promises. Some strategies look safe on the surface but carry hidden risks that can erase yields or lock up capital. Below are three common weak options that deserve a closer look before you commit funds.

Overcollateralized Loans with Volatile Assets

Crypto-backed loans require you to pledge digital assets as collateral. While this secures the loan, it introduces liquidation risk if the asset price drops sharply. If you borrow against a volatile token like Ethereum or Solana, a 20% market dip can trigger an automatic sale of your collateral. This isn't a bug; it's the mechanism that keeps the lender solvent. However, for the borrower, it means losing an asset you might have wanted to hold long-term. Always check the loan-to-value (LTV) ratio and the liquidation threshold. A high LTV leaves little room for error.

Yield Farming on Unaudited Protocols

High yields often signal high risk. Some platforms advertise double-digit returns by lending out assets to unknown borrowers or through complex, unaudited smart contracts. These protocols may lack basic security checks, making them vulnerable to hacks or exploits. Even if a protocol seems popular, a lack of third-party audits is a red flag. One security flaw can drain the entire pool. Stick to protocols with a proven track record and transparent audit reports. Never chase yield without understanding the underlying risk.

Platform-Specific Risk Without Diversification

Lending all your assets on a single platform concentrates your risk. If that platform faces insolvency, regulatory action, or a technical failure, you could lose everything. Diversifying across multiple reputable platforms reduces this exposure. Look for platforms with strong capitalization, clear regulatory compliance, and insurance funds. While this might lower your average yield slightly, it protects your principal. The goal is sustainable income, not a gamble on a single counterparty's stability.

Crypto lending strategy: what to check next

Before committing capital to real-world asset yields or infrastructure plays, it helps to address the practical objections that define the risk-reward profile of this sector. The answers below clarify how the mechanics work, where the profit comes from, and what safety measures actually matter in 2026.

These questions highlight the core trade-off: higher yields come with higher counterparty and technical risks. Always verify platform audits and reserve proofs before lending.

No comments yet. Be the first to share your thoughts!