How crypto lending works in 2026

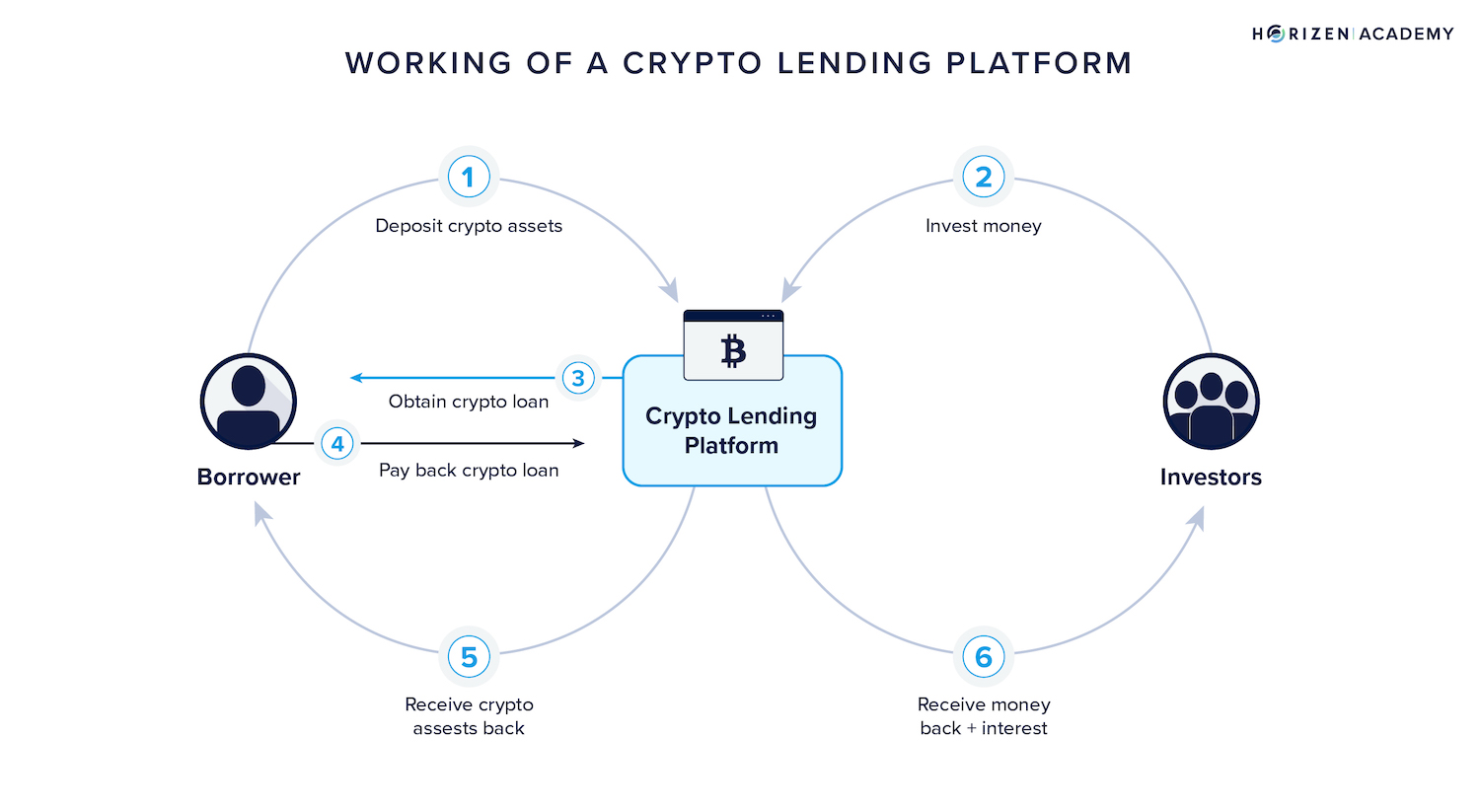

At its core, crypto lending is a financial transaction where one party lends cryptocurrency to another in exchange for compensation Coinbase. This mechanism mirrors traditional banking but operates through two distinct frameworks: centralized finance (CeFi) and decentralized finance (DeFi). Understanding the difference is essential before placing capital at risk.

In CeFi models, you lend assets to a centralized platform, which then acts as the intermediary. The platform pools your funds and lends them to institutional borrowers, such as hedge funds or market makers. In return, you receive interest payments, often higher than traditional savings accounts. However, this convenience comes with counterparty risk—you are trusting a single company to manage your assets securely and transparently. Accounting standards, as noted by PwC, treat these transactions as lending activities where the reporting entity expects a fee in return PwC.

DeFi models operate without a central intermediary. Instead, smart contracts on blockchains like Ethereum or Solana automatically match lenders with borrowers. You deposit assets into a liquidity pool, and borrowers borrow against them, with the protocol handling interest distribution. While this removes counterparty risk associated with a single company, it introduces technical risks, such as smart contract vulnerabilities or oracle failures. The yield in DeFi is often driven by supply and demand dynamics within the protocol rather than institutional borrowing fees.

The underlying asset you lend also dictates the risk profile. Lending stablecoins typically yields 3% to 10% annually, offering more stability but lower returns. Lending volatile tokens like Bitcoin or Ethereum can offer higher yields, but the value of your principal can fluctuate significantly. To understand the volatility of the primary collateral assets, consider the current market behavior of Bitcoin.

Before evaluating specific platforms or yields, it is critical to recognize that both models carry unique risks. CeFi risks center on solvency and regulatory compliance, while DeFi risks focus on code integrity and liquidity. The next sections will break down these risks and how to assess platform safety.

Comparing lending platforms and yields

Choosing a venue for your crypto assets comes down to a single trade-off: yield versus counterparty risk. Higher returns usually signal that you are taking on more risk, whether through exposure to volatile tokens or reliance on unregulated intermediaries. To make an informed decision, you need to look past the headline APY and understand the underlying mechanics of each platform type.

| Platform Type | Typical APY Range | Primary Risk Factor | Custody Model |

|---|---|---|---|

| Centralized Exchanges (CEX) | 1% - 5% | Platform insolvency, regulatory action | Custodial (Platform holds keys) |

| DeFi Protocols (Lending Pools) | 3% - 15%+ | Smart contract bugs, impermanent loss | Non-custodial (User holds keys) |

| Institutional Lenders | 2% - 6% | Credit default, collateral liquidation | Qualified custodians |

| Stablecoin Vaults | 5% - 10% | De-pegging, underlying asset quality | Mixed (Smart contract or custodial) |

The table above illustrates the spectrum of options available today. Centralized exchanges offer ease of use and familiar interfaces, but they require you to trust the platform with your private keys. If the exchange fails, as we have seen in the past, recovery is rarely guaranteed. In contrast, decentralized finance (DeFi) protocols allow you to retain custody of your assets through smart contracts. While this reduces counterparty risk, it introduces technical risk; a bug in the code can lead to total loss of funds.

Yields are also heavily influenced by the asset you are lending. Stablecoin lending typically offers lower, more predictable returns compared to volatile assets like Bitcoin or Ethereum. This is because stablecoins are often lent out for short-term liquidity needs, whereas volatile tokens are lent for longer durations to capture higher interest rates. Always check the current market conditions, as yields can fluctuate daily based on supply and demand.

When evaluating platforms, prioritize those with transparent audits and a clear track record. For regulated entities, look for compliance with local financial authorities. For DeFi protocols, review third-party security audits and the total value locked (TVL) as indicators of community trust. Never lend more than you can afford to lose, and remember that higher yields are not free—they are compensation for risk.

Real World Assets and Infrastructure Risks

When crypto lending platforms advertise high yields, they are often borrowing against Real World Assets (RWA) like private credit, real estate, or corporate bonds. While this bridges traditional finance with blockchain, it introduces a distinct layer of risk that pure crypto-native lending avoids. The core issue is the disconnect between the digital token and the physical asset it represents.

The Legal Enforceability Gap

The most significant hurdle in RWA lending is legal enforceability. If a borrower defaults on a private credit loan, the smart contract cannot automatically seize the underlying real estate or corporate assets. You are relying on off-chain legal structures to enforce on-chain debt. If the legal wrapper is flawed or if the jurisdiction does not recognize the tokenized claim, the collateral may be worthless in a bankruptcy proceeding. This creates a scenario where you hold a digital token but have no legal recourse to the value it claims to represent.

Smart Contract and Infrastructure Vulnerabilities

Even if the legal structure is sound, the infrastructure connecting the off-chain asset to the on-chain world is fragile. RWA lending requires oracle feeds to verify asset values and smart contracts to manage collateralization ratios. Any vulnerability in these contracts can lead to total loss of funds. Additionally, the custodians holding the actual legal title to the RWA are a single point of failure. If the custodian is hacked, goes insolvent, or acts maliciously, the on-chain representation becomes a hollow shell.

Liquidity Traps in Tokenized Debt

Unlike Bitcoin or Ethereum, which can be sold instantly on any exchange, RWA tokens often face severe liquidity traps. The secondary market for tokenized private credit is thin and fragmented. If you need to exit a position during a market downturn, you may find no buyers, or you may have to sell at a steep discount. This illiquidity risk is often hidden in the high yield promises. You are effectively locking your capital into an asset that cannot be easily converted back to cash when you need it most.

Note: Unlike on-chain collateral (like ETH) which can be liquidated automatically by code, RWA collateral requires off-chain legal enforcement, which is slower, costlier, and less certain.

Regulatory Uncertainty

Regulators are still figuring out how to classify and oversee tokenized real-world assets. The legal status of a tokenized bond or loan is not yet settled in many jurisdictions. New regulations could restrict who can hold these assets, how they can be traded, or even declare certain tokenization structures illegal. This regulatory shadow adds a layer of political risk that pure crypto assets do not face to the same degree.

Infrastructure Dependency

RWA lending platforms are heavily dependent on traditional financial infrastructure. They rely on banks for fiat on-ramps, legal firms for structuring, and auditors for verification. If any of these traditional partners fail or withdraw support, the entire lending operation can collapse. This interdependence means that RWA lending is not truly decentralized; it is a hybrid model that inherits the weaknesses of both the crypto and traditional finance worlds.

Practical Implications for Lenders

For lenders, this means that high yields from RWA-backed loans are not just compensation for time value, but also for legal, liquidity, and regulatory risk. You are essentially acting as a bank, taking on the credit risk of the underlying borrower and the operational risk of the platform. Due diligence must extend beyond the smart contract to include the legal opinions, custodial arrangements, and regulatory compliance of the platform.

Conclusion

RWA lending offers a compelling narrative of bridging TradFi and DeFi, but the risks are substantial and often opaque. The gap between digital representation and physical reality is where value is lost. Lenders must understand that they are not just betting on crypto prices, but on the legal and operational integrity of a complex hybrid system.

How to start crypto lending safely

Starting crypto lending doesn’t require a degree in finance, but it does demand a disciplined approach to security. The process is straightforward: choose a platform, verify your identity, and deposit assets. However, skipping due diligence is the fastest way to lose capital. Treat your first steps like setting up a secure vault rather than opening a savings account.

Before depositing a single dollar, check if the platform is registered or regulated in your jurisdiction. Look for transparent ownership, physical addresses, and clear terms of service. If a platform promises yields that seem too good to be true—like 20% APY on stablecoins without a clear risk explanation—walk away. Stick to established players with a track record of solvency.

Most reputable lending platforms require Know Your Customer (KYC) verification. This involves submitting government-issued ID and sometimes proof of address. While this reduces privacy, it is a critical safety feature. Regulated platforms use KYC to prevent money laundering and protect users from fraud. Avoid platforms that allow anonymous, high-value lending without any identity checks.

Never rely on passwords alone. Enable 2FA using an authenticator app like Google Authenticator or Authy. Avoid SMS-based 2FA if possible, as it is vulnerable to SIM-swapping attacks. This step adds a layer of security that prevents unauthorized access even if your password is compromised.

Do not deposit your entire portfolio at once. Start with a small amount to test the withdrawal process. Ensure you can deposit, earn interest, and withdraw funds smoothly. This "test drive" reveals any hidden fees, processing delays, or platform quirks before you commit significant capital.

Never put all your assets on one platform. Spread your lending capital across two or three reputable platforms to mitigate counterparty risk. Additionally, diversify the assets you lend. Stablecoins offer lower risk and steady yields, while volatile assets like Bitcoin or Ethereum offer higher potential returns but come with market risk. A balanced approach protects you from both platform failure and market crashes.

By following these steps, you build a foundation for safe crypto lending. Remember, the goal is sustainable growth, not gambling. Always prioritize the safety of your principal over the allure of high yields.

Frequently asked questions about crypto lending

How do I start crypto lending?

Begin by selecting a reputable lending platform that aligns with your risk tolerance and asset holdings. Once registered, deposit your cryptocurrency into the platform’s designated wallet. From there, you can configure your lending terms, specifying the interest rate and loan duration to match your financial goals.

Is crypto lending profitable?

Profitability varies based on the platform, asset type, and current market demand. Lending stablecoins generally yields between 3% and 10% annually, offering relative stability. In contrast, lending volatile tokens often provides higher yields but comes with significantly increased risk due to price fluctuations.

What happens if a borrower defaults?

Most platforms use overcollateralization, meaning borrowers must deposit more value than they borrow. If a borrower defaults or the collateral value drops below a set threshold, the platform automatically liquidates the collateral to recover the lent funds. This mechanism protects lenders from total loss, though market volatility can still impact returns.

No comments yet. Be the first to share your thoughts!