How crypto lending works

Crypto lending is a financial transaction where one party lends cryptocurrency to another party in exchange for compensation. Unlike traditional banking, this process bridges two distinct models: centralized finance (CeFi) and decentralized finance (DeFi). Understanding the difference is the first step in navigating this high-stakes market.

In the CeFi model, you lend your assets to a centralized platform, much like depositing money in a bank. The platform acts as the intermediary, managing the loans, setting interest rates, and handling the risk. While this offers a simpler user experience, it introduces counterparty risk. You are trusting a single entity with your keys and your funds. If the platform fails or is hacked, recovering your assets can be difficult or impossible.

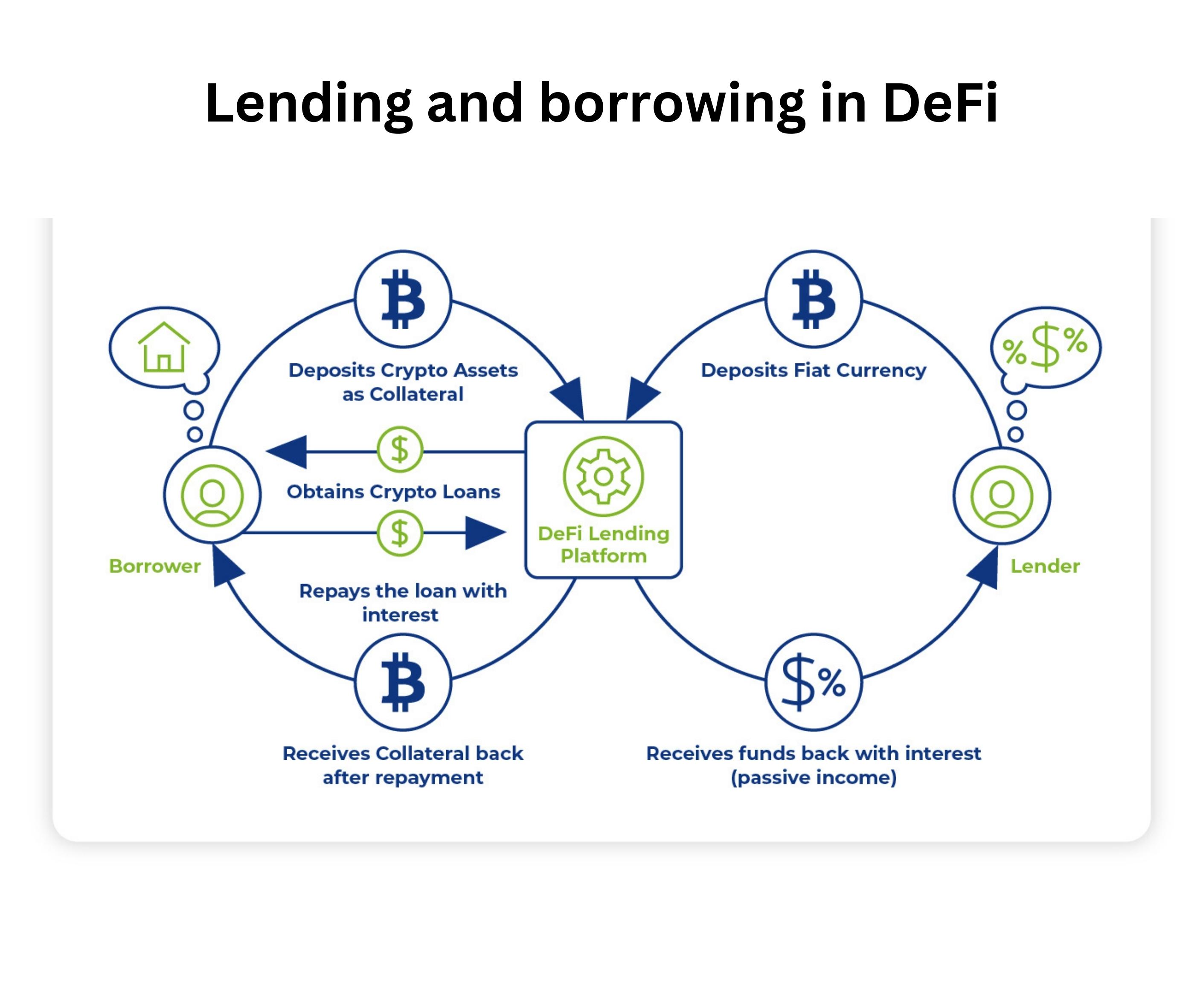

DeFi operates differently. Here, smart contracts on the blockchain automate the lending process without a middleman. Borrowers must typically overcollateralize their loans, locking up more value than they borrow to ensure the lender is protected. This transparency reduces the risk of platform insolvency but requires a deeper understanding of blockchain mechanics and gas fees.

The choice between these models often comes down to control versus convenience. CeFi offers ease of use, while DeFi offers transparency and self-custody. As you explore crypto lending guides, keep in mind that the yield you earn is directly tied to the risk you assume.

CeFi vs. DeFi lending platforms

Choosing between centralized and decentralized infrastructure defines your risk profile in crypto lending. The decision isn't just about yield; it's about who holds the keys and how transparency is managed. Centralized finance (CeFi) offers the familiar interface of traditional banking, while decentralized finance (DeFi) relies on code and self-custody.

Centralized finance (CeFi)

CeFi platforms act as intermediaries, holding your assets in custodial wallets. This model prioritizes user experience and customer support. You interact with a company that manages security, compliance, and liquidity. If you forget your password, they can help you recover your account. However, this convenience comes with counterparty risk. As noted by PwC, lending transactions often involve lending crypto assets to a counterparty, meaning you are trusting the platform's solvency [PwC]. If the platform fails, your funds may be at risk, as seen in past industry collapses. Coinbase describes this as a financial transaction where one party lends to another through a managed service [Coinbase].

Decentralized finance (DeFi)

DeFi platforms operate via smart contracts on public blockchains. There is no central company to call. You connect a self-custody wallet, and the code automatically matches lenders and borrowers. This offers full transparency and control. You retain custody of your assets until the moment of transaction. However, the user experience is steeper. You must manage gas fees, understand smart contract risks, and ensure you don't lose your private keys. Embroker notes that this form of DeFi allows investors to lend directly in exchange for interest, bypassing traditional banks [Embroker].

Side-by-side comparison

The table below highlights the core trade-offs between these two infrastructure types for your crypto lending guide.

| Feature | CeFi | DeFi |

|---|---|---|

| Custody | Platform holds keys | User holds keys |

| Recovery | Email/Support reset | No recovery possible |

| Transparency | Audited reports (varies) | On-chain public data |

| Yield Potential | Lower, stable rates | Higher, volatile rates |

| Ease of Use | High (bank-like) | Low (technical) |

Market context

Understanding the broader market helps contextualize these choices. Current crypto market conditions influence both CeFi interest rates and DeFi liquidity pools. Monitoring live asset prices is essential for timing your lending strategies.

Top crypto loan providers in 2026

Choosing a crypto lending platform requires balancing yield potential with counterparty risk. In 2026, the market has consolidated around a few major players that offer institutional-grade security alongside retail-friendly interfaces. Below are the top crypto loan providers that currently dominate the landscape for both borrowers and lenders.

1. Coinbase

Coinbase remains the most accessible entry point for beginners, offering a seamless integration between spot trading and lending. Its "Earn" program allows users to lend stablecoins and select cryptocurrencies with minimal friction. The platform’s primary advantage is its regulatory compliance and insurance coverage on custodial assets, making it a safer haven for risk-averse lenders. However, yields are generally lower than on decentralized platforms, reflecting the premium paid for centralized security.

2. Nexo

Nexo stands out for its hybrid model, allowing users to borrow against their crypto holdings without selling them, thus avoiding immediate tax events. The platform offers instant loans with competitive interest rates and a unique feature: the ability to pay interest in NEXO tokens for reduced rates. For lenders, Nexo provides high-yield savings accounts on stablecoins. While convenient, users must trust Nexo’s proprietary risk management system rather than on-chain smart contracts.

3. BlockFi (via FTX Bankruptcy Estate Recovery)

Note: As of 2026, BlockFi’s operations have been restructured. New entrants like Ledn and Celsius Network (post-bankruptcy restructuring) have filled the void, but for the purpose of this guide, we focus on active, fully operational entities.

4. Aave (Decentralized)

For those prioritizing self-custody, Aave is the leading decentralized finance (DeFi) lending protocol. Users connect directly via wallets like MetaMask, retaining full control of their assets. Aave offers variable and stable interest rates for both lenders and borrowers. The primary benefit is transparency—every transaction is recorded on-chain. The trade-off is complexity: users must manage gas fees and understand smart contract risks, such as oracle failures or liquidation cascades.

5. MakerDAO (via Sky Protocol)

MakerDAO, now transitioning under the Sky Protocol brand, is the backbone of decentralized stablecoin lending. It allows users to generate DAI (or SAI) by locking up ETH or other assets as collateral. This is the premier option for advanced borrowers seeking deep liquidity and low borrowing costs. Lenders earn yield from the stability fees paid by borrowers. The system is highly decentralized but requires a sophisticated understanding of crypto-collateralized debt positions (CDPs).

Secure your collateral

Regardless of the platform you choose, securing your collateral is non-negotiable. If you are using a centralized lender, ensure your withdrawal keys are protected. For DeFi users, a hardware wallet is essential to prevent phishing attacks.

As an Amazon Associate, we may earn from qualifying purchases.

How loan-to-value ratios protect your collateral

The loan-to-value (LTV) ratio is the single most important metric in crypto lending. It determines how much you can borrow against your digital assets and, more critically, when your position becomes unsafe. Think of LTV as a financial safety margin; the higher the ratio, the thinner that margin becomes.

Platforms calculate LTV by dividing the loan amount by the value of the collateral. For example, if you deposit $10,000 worth of Bitcoin and borrow $5,000 in USDC, your LTV is 50%. Most major platforms cap initial LTVs between 50% and 75%, depending on the asset's volatility. Stablecoins often allow higher ratios because their value doesn't swing wildly, while volatile assets like Ethereum require a larger buffer.

This ratio is not static. As crypto prices fluctuate, your LTV changes in real-time. If Bitcoin's price drops, the value of your collateral decreases, causing your LTV to rise. This is where the danger lies. If your LTV exceeds the platform's maintenance threshold, you risk liquidation.

To manage this risk, you must monitor your LTV closely. Many platforms offer "health factors" or similar metrics that give you a clearer picture of your position's stability than the raw LTV percentage alone. Keeping your LTV well below the maximum limit provides a buffer against sudden market volatility, ensuring you retain control of your assets.

The risks of crypto lending

Crypto lending offers high yields, but it comes with a distinct set of dangers that don't exist in traditional banking. When you lend on-chain or through a centralized platform, you are taking on counterparty risk, smart contract risk, and regulatory uncertainty. Understanding these hazards is essential before you lock up your assets.

Smart contract vulnerabilities

DeFi lending protocols operate on code, not customer service teams. If a smart contract contains a bug, attackers can drain the liquidity pool, leaving lenders with nothing. Unlike a bank where deposits are insured by the government, crypto lending platforms rarely offer such safety nets. Audits help, but they are not foolproof. A single vulnerability can wipe out millions in minutes. Treat your funds as if they are exposed to constant, sophisticated attacks.

Platform insolvency

Centralized crypto lenders, like Celsius or BlockFi, have collapsed in recent years, leaving users unable to withdraw their funds. These platforms often lend out your deposited assets to borrowers or use them for risky proprietary trading. If the value of those assets drops or borrowers default, the platform becomes insolvent. There is no FDIC insurance for crypto. You are effectively an unsecured creditor in a high-risk financial system.

Regulatory changes

Governments are still figuring out how to regulate crypto lending. New laws could restrict how platforms operate, force them to freeze accounts, or ban certain types of lending activities entirely. A sudden regulatory crackdown can disrupt liquidity and impact the value of the assets you have lent. Stay informed about the legal landscape in your jurisdiction, as compliance costs can drive up fees or reduce yields for lenders.

Market volatility

The crypto market is notoriously volatile. If you are lending volatile assets like Bitcoin or Ethereum, their value can swing dramatically in a short period. While stablecoins offer some protection against price swings, they carry their own risks, such as de-pegging events. Always consider the worst-case scenario for the asset you are lending and ensure you can afford to lose its value.

Frequently asked: what to check next

Is crypto lending profitable?

Profitability in a crypto lending guide context depends on your risk tolerance and asset selection. Stablecoin yields typically range from 3% to 10% annually, offering steadier returns. Volatile tokens provide higher interest rates but expose you to greater market risk and potential liquidation events.

How do I start crypto lending?

Begin by selecting a reputable platform that aligns with your goals. Deposit your chosen cryptocurrency into the platform’s wallet, then configure your lending terms, including the interest rate and loan duration. Always verify the platform’s security protocols before committing funds.

What are the main risks of crypto lending?

The primary risks include counterparty failure, where the borrower or platform defaults, and smart contract vulnerabilities. Additionally, market volatility can trigger liquidations if the collateral value drops below required thresholds. Diversification and choosing regulated platforms can help mitigate these exposures.

No comments yet. Be the first to share your thoughts!