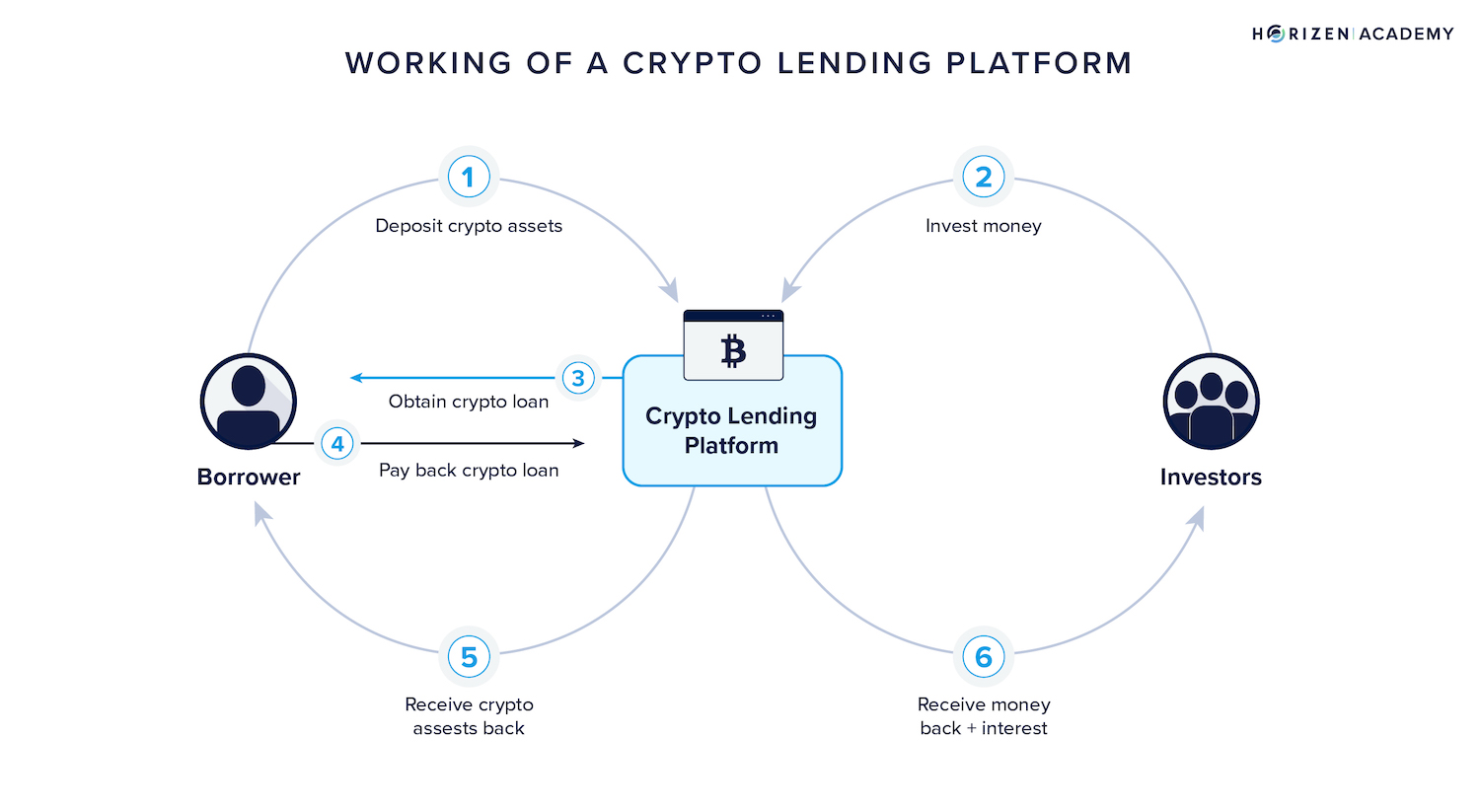

How crypto lending works today

At its core, crypto lending is a financial transaction where one party lends cryptocurrency to another in exchange for interest payments. This mechanism mirrors traditional banking but operates on blockchain infrastructure, allowing for faster settlement and 24/7 markets. The fundamental goal is simple: idle assets generate yield for lenders, while borrowers gain access to capital without selling their holdings.

The ecosystem splits into two distinct models: centralized custodial lending and decentralized non-custodial protocols. Understanding the difference is critical because the risk profile changes entirely depending on which model you use.

Centralized Custodial Lending

In the centralized model, you interact with a financial institution—often a major exchange or a regulated fintech company. You deposit your crypto into their platform, and they act as the intermediary, managing the loan issuance and repayment. This structure feels familiar if you have ever used a traditional bank or brokerage.

The primary advantage is ease of use. Customer support, password recovery, and streamlined interfaces make it accessible. However, you are trusting a third party with your assets. If the platform faces insolvency or regulatory action, your funds may be frozen or lost. This model relies heavily on the financial health and regulatory compliance of the institution.

Decentralized Non-Custodial Lending

Decentralized finance (DeFi) protocols remove the middleman. Instead of trusting a company, you interact directly with smart contracts on the blockchain. These self-executing code agreements manage the lending pool, ensuring that loans are overcollateralized and liquidated automatically if the value of the collateral drops too low.

In this model, you retain control of your keys until you lock them into the protocol. This eliminates counterparty risk related to corporate bankruptcy but introduces smart contract risk. If there is a bug in the code, funds can be exploited. The trade-off is clear: you gain autonomy and transparency, but you lose the safety net of a customer service team.

Both models serve different needs. Centralized platforms offer simplicity and fiat on-ramps, while decentralized protocols offer permissionless access and transparency. As you explore crypto lending, your choice between these two paths will define your risk exposure and potential returns.

Centralized vs decentralized lending models

Choosing between centralized finance (CeFi) and decentralized finance (DeFi) lending comes down to a fundamental trade-off: convenience versus control. CeFi platforms act as custodial intermediaries, similar to traditional banks, while DeFi protocols operate as non-custodial smart contracts on the blockchain. Understanding this structural difference is critical for managing risk in high-stakes financial decisions.

How CeFi Lending Works

Centralized exchanges like Binance or Coinbase hold your assets in their own wallets. When you lend, you are essentially depositing funds into their internal ledger. This model offers familiar user experiences, including customer support, fiat on-ramps, and often insured deposits. However, this convenience introduces counterparty risk. If the platform faces insolvency or regulatory action, your assets may be frozen or lost, as seen in the collapses of major lenders like Celsius and Voyager. Regulatory compliance is also a key feature; CeFi platforms typically require KYC/AML checks, ensuring that lending activities align with local financial laws.

How DeFi Lending Works

DeFi protocols like Aave or Compound remove the middleman entirely. You interact directly with smart contracts using your own non-custodial wallet. This means you retain full control over your private keys, eliminating counterparty risk from a central entity. Yields are often higher because they are driven by pure market supply and demand without corporate overhead. However, this comes with technical complexity and smart contract risk. Bugs or exploits in the code can lead to irreversible losses. Additionally, DeFi is largely permissionless, meaning it operates in a regulatory gray area in many jurisdictions, with no customer support to turn to if something goes wrong.

Key Trade-offs at a Glance

The table below summarizes the primary differences between these two models to help you decide which infrastructure aligns with your risk tolerance and technical comfort.

| Feature | CeFi (Centralized) | DeFi (Decentralized) |

|---|---|---|

| Custody | Platform holds keys | User holds keys |

| Yield Source | Platform lending fees | Market supply/demand |

| Regulation | KYC/AML required | Permissionless/Anon |

| Risk Type | Counterparty/Bankruptcy | Smart Contract Bugs |

| User Experience | Bank-like interface | Wallet interaction |

Security and Yield Considerations

When evaluating yield, remember that higher returns in DeFi often reflect higher risk. CeFi yields are generally lower but may include insurance mechanisms, though these are not always reliable. In DeFi, yields can fluctuate wildly based on liquidity pools. For live market data on the underlying assets, refer to the technical charts below to understand current volatility trends before committing capital.

Institutional infrastructure and regulation

The crypto lending market is no longer just a playground for retail speculators. Institutional players are moving in, bringing with them a demand for regulated entities, clear accounting standards, and robust legal frameworks. This shift is reshaping the landscape, turning what was once a Wild West frontier into a more structured, albeit complex, financial sector.

How institutions are entering the space

Traditional finance firms are approaching crypto lending through regulated entities rather than decentralized protocols alone. This involves partnering with licensed custodians and using compliant lending platforms that adhere to Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. The goal is to mitigate counterparty risk and ensure that assets are held in a manner that satisfies institutional auditors.

According to PwC’s accounting guides, a reporting entity may lend crypto assets to a counterparty in return for a fee, but this must be carefully structured to meet financial reporting standards. Institutions are prioritizing transparency and auditability, often requiring proof of reserves and regular third-party attestations. This approach contrasts sharply with the opaque nature of early DeFi lending pools, where smart contract risks were often the only safeguard.

The role of SEC guidance

Regulatory clarity, or the lack thereof, plays a pivotal role in institutional adoption. The SEC’s recent guidance and letters, such as the TDC response on crypto lending transactions, provide critical insights into how these activities might be classified under existing securities laws. While not a final rulebook, these documents signal the regulatory body’s intent to scrutinize lending platforms that offer yield on assets deemed securities.

For institutional investors, this means navigating a landscape where the definition of a "loan" can have significant legal and tax implications. They are increasingly seeking platforms that engage in proactive dialogue with regulators and offer clear legal opinions on their operational models. This caution is driving a bifurcation in the market: highly regulated, institutional-grade platforms on one side, and riskier, less compliant options on the other.

Market impact and data

The entry of institutional capital has introduced new liquidity dynamics and price sensitivities. While specific institutional volume data is often private, the broader market trends reflect increased stability in regulated environments. Investors can track the health of the broader crypto market, which influences institutional sentiment, through live data.

As institutions continue to integrate crypto lending into their portfolios, the pressure for standardized regulations will likely intensify. This could lead to a more mature market with clearer risk parameters, but it also means that the era of unregulated, high-yield lending may be coming to an end for those seeking institutional-grade security.

How Bitcoin and Ethereum Move Lending Markets

Lending rates do not exist in a vacuum; they are directly tethered to the technical health of the underlying collateral. When Bitcoin or Ethereum trends upward, lenders feel confident offering lower interest rates because the risk of liquidation is minimal. Conversely, technical breakdowns in these primary assets trigger immediate risk-off behavior, causing borrowing costs to spike as platforms tighten loan-to-value (LTV) ratios to protect their balance sheets.

Monitoring the price action of BTC and ETH is essentially monitoring the pulse of the entire crypto lending ecosystem. A sustained move above key resistance levels often signals liquidity injection, encouraging institutions to deploy capital into yield-generating lending protocols. However, a failure to hold support levels can lead to rapid deleveraging, where forced selling compresses spreads and reduces the availability of credit across the market.

The chart below illustrates the current technical structure of Bitcoin, which serves as the primary benchmark for institutional lending rates. Traders and lenders alike watch these moving averages and volume profiles to gauge whether the market is in a risk-on or risk-off phase.

Risk management for lenders and borrowers

Crypto lending offers liquidity without selling your assets, but it introduces risks that traditional banking largely eliminates. You are no longer protected by deposit insurance, and the infrastructure is still maturing. To participate safely, you must understand where the money goes and what happens when things break.

Smart contract vulnerability

When you lend on DeFi platforms, your funds are locked in code. If that code contains a bug or is exploited, the funds can be drained instantly. Unlike a bank, there is no customer service to reverse a transaction. Mitigation starts with due diligence: look for platforms that have undergone third-party security audits by reputable firms and have a history of responsible disclosure.

Liquidation risk

If you borrow against your crypto, the value of your collateral is constantly monitored. If the market drops and your collateral value falls below the required threshold, the protocol will automatically liquidate your assets to cover the loan. This can happen in minutes during high volatility. To manage this, maintain a healthy loan-to-value (LTV) ratio—ideally keeping it well below the liquidation threshold—and consider using stablecoins for borrowing to reduce volatility exposure.

Counterparty risk

In centralized crypto lending, you are trusting a company to hold your assets and pay you interest. If that company becomes insolvent, like Celsius or BlockFi did, you could lose everything. Always check the platform’s regulatory status and reserve proofs. For DeFi, while you avoid a single company’s failure, you still face protocol risk. Diversifying across multiple protocols can help spread this risk.

Market volatility

Cryptocurrencies are inherently volatile. A 20% drop in Bitcoin can trigger a cascade of liquidations across the market. This volatility affects both lenders (whose collateral value drops) and borrowers (whose loan costs may rise). Understanding the market cycles and having a clear exit strategy is essential for long-term participation.

Before depositing funds, verify that the smart contracts have been audited by established security firms. Look for audit reports on the platform’s website or through aggregators like Code4rena. Check if the platform has a bug bounty program, which indicates a proactive approach to security.

Set up alerts for your loan-to-value (LTV) ratios. If you are borrowing, keep your LTV conservative to avoid liquidation during market dips. Most platforms allow you to set custom alerts, so use them to stay ahead of sudden price movements.

Do not put all your assets into a single lending protocol. Spread your capital across multiple platforms and asset types. This reduces the impact if one platform experiences a technical failure or insolvency event.

For centralized platforms, check if they are registered with relevant financial authorities. Regulatory compliance often indicates a higher standard of operational transparency and capital reserves, though it does not eliminate risk entirely.

No comments yet. Be the first to share your thoughts!