How crypto lending works now

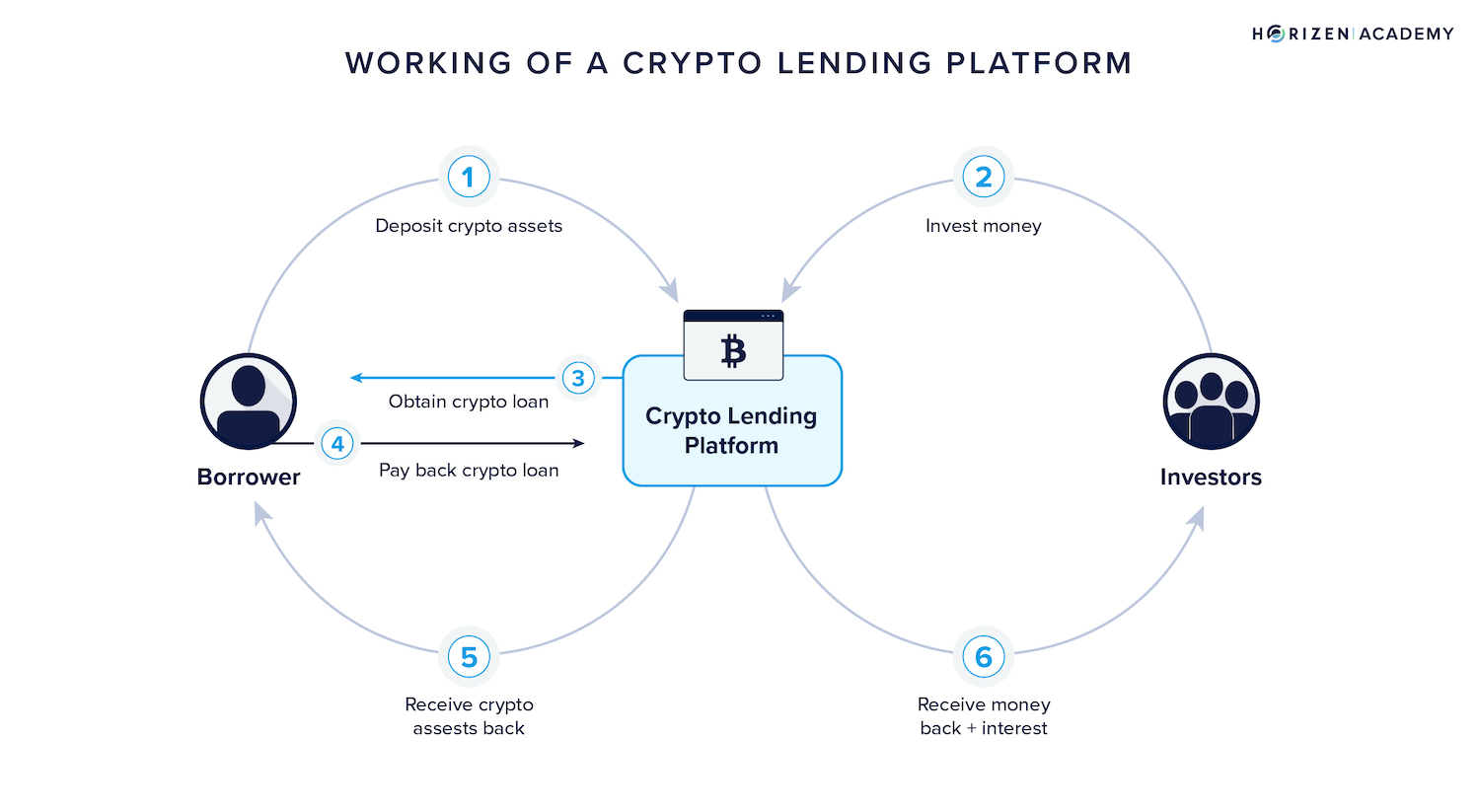

Crypto lending is a financial transaction where one party lends cryptocurrency to another in exchange for compensation, typically in the form of interest. This mechanism mirrors traditional banking but operates with distinct mechanics and risk profiles. As PwC notes in its accounting guides, a reporting entity may lend crypto assets to a counterparty in return for a fee, establishing the foundational structure of these agreements. However, unlike bank savings accounts, the returns here are directly tied to the volatility and demand of the underlying digital assets.

The ecosystem splits into two primary models: centralized finance (CeFi) and decentralized finance (DeFi). CeFi platforms act as intermediaries, holding your assets in custodial wallets and managing the lending process much like a traditional bank. You deposit crypto, and the platform lends it out to borrowers, paying you interest. DeFi, by contrast, uses smart contracts on public blockchains to automate lending and borrowing without a central authority. Borrowers often provide overcollateralized crypto assets to secure loans, while lenders supply liquidity to decentralized protocols.

At the core of both models is collateral. Because crypto prices fluctuate rapidly, lenders require borrowers to lock up assets worth more than the loan amount. If the value of the collateral drops below a certain threshold, lenders may require additional funds or trigger an automatic liquidation to protect their investment. This dynamic creates higher yields than traditional finance but introduces significant risk if market conditions shift sharply.

The volatility of the underlying assets directly impacts lending rates and platform stability. Understanding this relationship is essential for evaluating potential returns.

Real world asset yields explained

The crypto lending landscape is shifting from speculative yield to tangible value. Real World Assets (RWA) represent the tokenization of traditional financial instruments, bringing the stability of bonds and treasury bills on-chain. This shift matters because it decouples yield from the volatility of the crypto market itself.

Tokenized treasury bills offer a direct link to government debt. Instead of relying on complex lending protocols or unbacked interest rates, investors hold claims on actual U.S. Treasuries. This provides a predictable income stream derived from real economic activity rather than token emissions. For risk-adjusted returns, this is a fundamental upgrade in quality.

The appeal lies in the convergence of blockchain efficiency and traditional credit. You get the transparency of on-chain settlement with the underlying safety of sovereign debt. As the market matures, RWA is becoming the bedrock for sustainable yield strategies, offering a hedge against the erratic cycles that have defined crypto lending for years.

Platform risks and infrastructure

Crypto lending promises high yields, but the infrastructure behind those returns is fragile. Unlike a bank where your deposit is protected by insurance and regulated oversight, crypto lending lives on code and counterparty promises. In 2026, the gap between advertised APY and actual risk remains wide, especially when platforms operate without full transparency.

Smart contract vulnerabilities

Every crypto loan relies on smart contracts—self-executing code that locks collateral and manages repayment. These contracts are powerful but not infallible. Bugs, logic errors, or unforeseen exploits can drain funds instantly. Even audited contracts carry residual risk, as no audit can predict every possible attack vector or edge case in a rapidly evolving ecosystem.

Custodial risks in CeFi

Centralized lending platforms (CeFi) hold your assets in their own wallets. This creates a single point of failure. If the platform is hacked, mismanages funds, or faces insolvency, you may lose everything with no recourse. The collapse of major CeFi lenders in past cycles serves as a stark reminder: when you lend through a centralized entity, you are taking on their credit risk, not just market risk.

Non-custodial options reduce counterparty risk but increase user responsibility. You control your keys, but you also bear the burden of securing them and understanding the code you interact with.

Transparency and audits matter

Look for platforms that publish regular, third-party audits and maintain clear proof of reserves. Transparency isn’t just a buzzword—it’s your only shield against hidden insolvency or mismanagement. Platforms that operate in the open, with verifiable on-chain data and independent security reviews, offer a safer foundation for your lending strategy.

Market volatility amplifies infrastructure risk

Even well-audited contracts can’t protect against extreme market moves. A sharp drop in crypto prices can trigger liquidations, draining your collateral before you can react. This isn’t just a platform risk—it’s a market risk that interacts directly with the infrastructure. Always monitor your loan-to-value (LTV) ratios and set alerts to avoid sudden liquidations.

Choosing the right lending platform

Crypto Lending works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

No comments yet. Be the first to share your thoughts!