The scale of crypto lending

Crypto-collateralized lending reached an all-time high of $73.6 billion at the end of Q3 2025, according to Galaxy Research. This milestone marks a significant inflection point in the market, reflecting a structural shift from traditional centralized finance (CeFi) toward decentralized infrastructure. The volume underscores the growing institutional and retail appetite for onchain liquidity, even as the broader market faces regulatory uncertainty and volatility.

The composition of this lending market has also evolved. Lending applications now account for more than 80% of the onchain market, a stark contrast to the 53% dominance of crypto lending in Q4 2021. Meanwhile, collateralized debt positions (CDPs) have settled at 16%, indicating that users are increasingly favoring direct lending protocols over locked collateral models. This shift highlights a maturation in how participants seek leverage and yield, moving toward more flexible and transparent DeFi mechanisms.

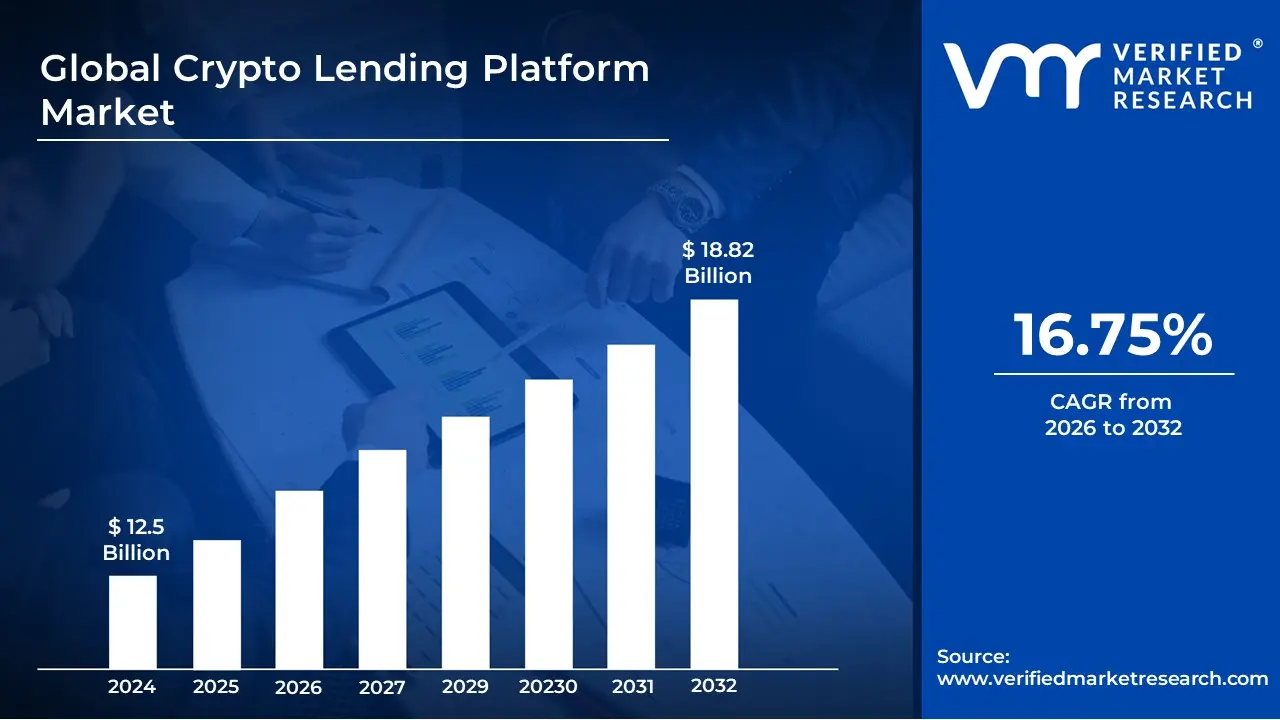

Looking ahead, the market is poised for continued expansion. The Crypto Lending Platform Market, valued at approximately $12.69 billion in 2026, is projected to reach $25.06 billion by 2030, growing at a compound annual growth rate (CAGR) of 18.5%. This trajectory suggests that crypto lending is no longer a niche activity but a core component of the digital asset ecosystem, driven by both technological innovation and increasing mainstream adoption.

Why Decentralized Lending Is Taking Share

The crypto lending market has shifted decisively toward decentralized finance (DeFi). According to Galaxy Research, lending applications now account for more than 80% of the onchain market as of Q3 2025, a stark contrast to the 53% share held by centralized finance (CeFi) models in late 2021. This migration isn't just about volume; it's about structural preference. Borrowers and lenders are moving away from opaque intermediaries toward protocols where code dictates terms.

Transparency is the primary driver. In DeFi, smart contracts execute loans automatically, meaning every transaction is visible on-chain. Users can see exactly how much collateral is locked, what the current liquidation thresholds are, and where their funds are being utilized. There is no black box. This open-book approach builds trust in an industry where counterparty risk has historically been a major pain point. When you lend through a decentralized protocol, you aren't trusting a bank's solvency report; you're trusting audited code and real-time data.

This shift has also unlocked superior yield opportunities. Because DeFi removes the overhead of traditional banking infrastructure, interest rates are often more competitive. Lenders can earn higher returns by providing liquidity to specific markets, while borrowers can access capital without credit checks, provided they have sufficient collateral. However, this comes with the responsibility of managing smart contract risk and understanding the mechanics of over-collateralization.

The move to DeFi lending reflects a broader trend in crypto: the demand for self-custody and verifiable financial systems. As the market matures, protocols that prioritize security and transparency are likely to capture even more market share from traditional centralized exchanges.

CeFi vs. DeFi lending structures

Crypto lending has split into two distinct camps: centralized finance (CeFi) and decentralized finance (DeFi). The choice between them comes down to how much trust you place in a company versus a codebase. CeFi platforms operate like traditional banks, while DeFi protocols function as automated market makers.

How CeFi lending works

Centralized lending platforms, such as Celsius or BlockFi (historically), act as intermediaries. You deposit crypto, and the platform lends it out to institutional borrowers, hedge funds, or market makers. In return, you earn interest. The platform manages the risk, custody, and regulatory compliance. This model offers a familiar user experience: you log in with an email and password, and the platform handles the rest. However, this convenience comes with counterparty risk. If the platform mismanages funds or faces insolvency, your assets may be frozen or lost, as seen in the 2022 collapses. Galaxy Research notes that while CeFi volume has contracted significantly since its 2021 peak, it still holds a substantial share of off-chain lending markets, particularly for institutional clients who require KYC/AML compliance [src-serp-1].

How DeFi lending works

DeFi lending protocols, like Aave or Compound, remove the middleman. Lenders deposit assets into smart contracts, which automatically match them with borrowers. There is no customer support team or central authority. Instead, the protocol uses overcollateralization and algorithmic interest rate models to manage risk. If a borrower’s collateral value drops, the smart contract automatically liquidates their position. This transparency allows anyone to audit the protocol’s solvency in real-time. According to Hedera, users can choose which money market to lend to, earning interest based on the market’s current supply and demand dynamics [src-serp-8]. The trade-off is complexity and smart contract risk; if the code has a bug, exploits can drain funds.

Side-by-side comparison

The table below highlights the structural differences that impact your risk and yield.

| Feature | CeFi Lending | DeFi Lending |

|---|---|---|

| Custody | Platform holds keys | User holds keys (self-custody) |

| Counterparty Risk | High (platform insolvency) | Low (smart contract code) |

| Yield Source | Institutional loans, trading | Borrower interest, fees |

| Regulatory Compliance | KYC/AML required | Permissionless, anonymous |

| Liquidity Access | Withdrawal limits possible | Instant (subject to pool depth) |

| Transparency | Opaque balance sheets | On-chain, auditable |

How DeFi Lending Generates Yield and Where the Risks Hide

Generating yield in decentralized finance (DeFi) is conceptually simple but mechanically complex. When you lend assets like Bitcoin or Ethereum through a protocol, you are essentially providing liquidity to borrowers. In return, the smart contract distributes interest payments, typically measured as an Annual Percentage Yield (APY). These rates often outpace traditional bank savings accounts, but that premium exists to compensate for the unique risks inherent in the ecosystem.

The interest rate models in protocols like Aave or Compound are dynamic. They adjust based on supply and demand. If too many people are borrowing a specific asset, the rate goes up to encourage more lenders to enter the market. Conversely, if lending supply exceeds demand, rates drop. This mechanism ensures that capital flows efficiently, but it also means your yield is never static. It fluctuates with market sentiment and borrowing volume.

However, this yield comes with significant exposure to two primary risks: liquidation and smart contract vulnerability. Understanding these is essential for protecting your capital in a high-stakes environment.

The Liquidation Risk

Liquidation is the most immediate threat to leveraged positions. If the value of the cryptocurrency you put up as collateral falls below a certain threshold, the protocol automatically sells your collateral to cover the loan. This process can happen rapidly during periods of high volatility.

Borrowers are not the only ones exposed. Lenders can also face indirect risks if the protocol’s liquidity dries up. In extreme cases, if a large number of borrowers are liquidated simultaneously, the protocol may struggle to sell assets at fair market value, potentially impacting the returns for lenders.

Smart Contract Vulnerabilities

Beyond market mechanics, there is the risk of code failure. DeFi protocols run on smart contracts—self-executing code on the blockchain. If there is a bug or a vulnerability in this code, hackers can exploit it to drain funds.

While audits help identify issues, they are not foolproof. New vulnerabilities are discovered regularly. This risk is particularly acute for newer or less audited protocols. Investors must assess the track record and security history of the platform before committing capital.

Regulatory Outlook and Macro Trends

The regulatory landscape for crypto lending is shifting from a gray area to a structured framework, driven largely by how major institutions record these activities. For market participants, this isn't just about compliance; it's about how crypto lending fits into the broader macroeconomic picture. The International Monetary Fund (IMF) has taken a significant step in this direction with its guidance on recording crypto lending in macroeconomic statistics.

The IMF’s Issue Note on "Recording of Crypto Lending-Borrowing in Macroeconomic Statistics" clarifies how to treat crypto assets that lack a corresponding liability designed as a general medium of exchange. This guidance helps central banks and statistical agencies integrate crypto lending data into traditional economic models, reducing ambiguity for lenders and borrowers alike. When regulators treat these assets with the same rigor as traditional financial instruments, it signals a maturation of the market.

This regulatory clarity impacts market dynamics by reducing systemic risk. As seen in the broader crypto market, volatility remains a factor, but institutional adoption is growing. The integration of crypto lending into official statistics allows for better risk assessment and policy-making, which can stabilize the sector over time.

To understand the current market context, it is useful to look at major asset performance. The following chart illustrates recent price movements for Bitcoin, which often serves as a benchmark for the broader crypto lending and DeFi ecosystem.

As regulations evolve, the distinction between traditional finance and DeFi will likely blur. Participants who stay informed about these macro trends will be better positioned to manage the risks and opportunities in the crypto lending market.

Frequently asked: what to check next

Can you make money with crypto lending?

Yes. When you lend Bitcoin or other cryptocurrencies, you earn interest in the form of an Annual Percentage Yield (APY). This mechanism mirrors traditional bank savings accounts, but the rates are typically much higher. The elevated yields compensate lenders for the significantly higher risk profile inherent in the crypto market, including volatility and smart contract vulnerabilities.

How risky is crypto lending?

Crypto lending carries substantial risk, primarily driven by price volatility. If the value of the collateralized cryptocurrency drops sharply, borrowers may face margin calls. This forces them to deposit more assets or risk having their positions liquidated. Additionally, lenders face the risk of platform insolvency or smart contract exploits, which can result in the total loss of deposited funds.

What is the difference between CeFi and DeFi lending?

CeFi lending involves depositing assets with a centralized company that manages custody and lends to institutional borrowers, offering a familiar user experience but higher counterparty risk. DeFi lending uses smart contracts for peer-to-peer lending, offering self-custody and transparency but requiring users to manage their own keys and understand smart contract risks.

No comments yet. Be the first to share your thoughts!