The current state of crypto lending

Crypto lending has evolved from a niche experiment into a foundational pillar of digital asset finance. At its core, it remains a straightforward financial transaction: one party lends cryptocurrency to another in exchange for interest compensation [1]. However, the infrastructure supporting these transactions has shifted dramatically, creating two distinct paths for participants in 2026.

The traditional model, often referred to as CeFi, relies on centralized intermediaries. These platforms act as banks, pooling user deposits and lending them out to institutional borrowers. While this model offers familiar user experiences, it concentrates risk. If the intermediary faces insolvency or regulatory crackdowns, user funds are often frozen or lost, as seen in previous market cycles.

In contrast, Decentralized Finance (DeFi) lending operates on smart contracts without central custodians. Here, borrowers must provide collateral in the form of other tokens, typically worth more than the loan value [2]. This over-collateralization is the primary safeguard against volatility. If the collateral's value drops significantly, the protocol automatically liquidates the assets to protect lenders [3]. This mechanism removes counterparty risk but introduces smart contract and liquidation risks that require careful management.

Understanding this divide is essential for building a strategy. CeFi offers simplicity and potentially higher yields from institutional lending books, while DeFi offers transparency and control over your assets. Both carry high stakes, and the choice between them depends on your risk tolerance and technical comfort.

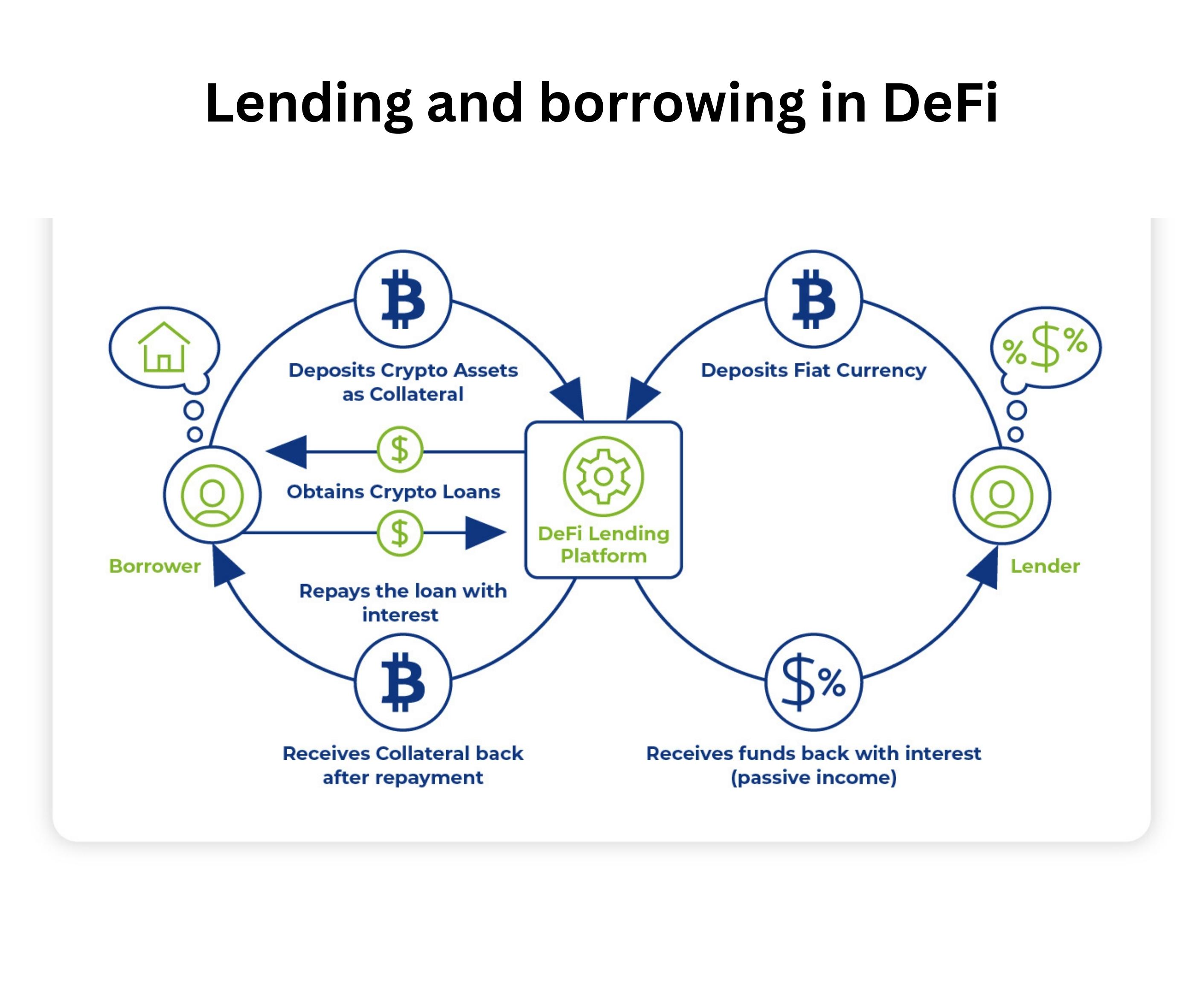

How DeFi Lending Mechanics Work

DeFi lending relies on over-collateralization to function without credit checks. To borrow, you must lock up cryptocurrency worth more than the loan itself, typically at a ratio of at least 150% [1]. This buffer protects lenders from the extreme volatility inherent in digital assets. If your collateral value drops, you face a margin call or liquidation.

Liquidation is the core risk mechanism. If the market price of your collateral falls below a set threshold, the protocol automatically sells your assets to repay the loan [2]. This process is swift and often results in significant losses for the borrower, who may lose their entire position. Understanding these mechanics is essential before deploying capital.

Beyond market mechanics, smart contract vulnerabilities pose a severe threat. DeFi protocols are open-source codebases that, if flawed, can be exploited by hackers. These bugs can lead to total loss of funds, as seen in past major breaches. Always audit the protocol's code or rely on established, battle-tested platforms to mitigate this infrastructure risk.

CeFi vs. DeFi lending models

Choosing between centralized finance (CeFi) and decentralized finance (DeFi) is a choice between convenience and control. CeFi platforms, such as centralized exchanges, act as intermediaries that hold your assets and manage the lending process. This mirrors traditional banking: you deposit funds, and the platform decides where they go. The trade-off is counterparty risk. If the exchange fails, you may lose access to your capital, as seen in past industry collapses.

DeFi protocols, by contrast, use smart contracts to automate lending. You retain custody of your assets in a non-custodial wallet until the moment you deposit them into the protocol. This removes the need to trust a company, but it introduces technical risks. Smart contract bugs or exploits can lead to total loss of funds. Additionally, DeFi requires a steeper learning curve to navigate wallets and gas fees safely.

The following table breaks down the core differences to help you weigh these risks against your needs.

| Feature | CeFi (Centralized) | DeFi (Decentralized) |

|---|---|---|

| Custody | Platform holds keys | User holds keys |

| Yield Source | Interbank/OTC lending | Protocol liquidity pools |

| Risk Profile | Counterparty/Insolvency | Smart contract/Code |

| Accessibility | Email/password login | Crypto wallet required |

| Privacy | KYC/Identity required | Pseudonymous/No KYC |

If you prioritize ease of use and customer support, CeFi may be the safer entry point, provided you monitor the platform’s solvency. If you understand technical risks and want full control, DeFi offers higher potential yields without a middleman. Always diversify across both to mitigate single-point failures.

Manage LTV and Choose Yield Wisely

Lending is a balancing act between borrowing power and risk exposure. The Loan-to-Value (LTV) ratio dictates how much you can borrow against your crypto collateral. A lower LTV, such as 50%, gives you breathing room against market volatility, while a higher LTV, like 75%, maximizes capital efficiency but leaves little margin for error. If the value of your collateral drops, you face a margin call or liquidation. Managing this ratio is the first line of defense in protecting your assets.

Yield sources vary significantly in risk. Stablecoins like USDC offer predictable, lower returns, making them suitable for conservative strategies. Volatile assets like Bitcoin or Ethereum can generate higher yields through lending or staking, but they introduce price risk on top of interest rate risk. Figure Markets notes that crypto-backed loans allow you to borrow traditional currency or stablecoins using digital assets as collateral, enabling you to access liquidity without selling your holdings [src-serp-2].

When selecting a yield source, consider the correlation between your collateral and the asset you are lending. Lending the same asset you hold as collateral can amplify risk if the market turns. Diversifying your yield generation across different asset classes or using a mix of stablecoins and volatile assets can help smooth out returns. Always monitor your LTV ratio closely, especially during periods of high market volatility, to avoid unexpected liquidations.

Assessing profitability and long-term viability

The headline yield on crypto lending often looks like free money, but the real test is what remains after the dust settles. In 2026, the gap between nominal interest and actual purchasing power is where most strategies fail. You aren’t just competing with traditional savings accounts; you are competing with inflation, impermanent loss, and the ever-present risk of platform insolvency.

Profitability isn’t a static number. It is a moving target driven by market cycles. During bull markets, borrowing demand spikes, pushing yields higher but also increasing the likelihood of liquidations. In bear markets, yields compress as liquidity dries up. To stay viable, your strategy must account for these swings rather than locking into fixed rates that ignore market reality.

The Real Cost of Risk

High yields are rarely free. They are compensation for taking on specific risks: smart contract bugs, regulatory crackdowns, or counterparty default. When evaluating a lending protocol, look beyond the Annual Percentage Yield (APY). Check the loan-to-value (LTV) ratios, the liquidity depth of the collateral, and the track record of the platform’s security audits.

Balancing Yield Against Inflation

A 10% APY sounds attractive until you realize that stablecoin de-pegging or inflation erodes that gain. The goal is positive real yield—earning more than the loss of purchasing power. This often means accepting lower nominal yields in exchange for higher stability, such as lending established stablecoins against blue-chip collateral like Bitcoin or Ethereum.

Long-Term Viability Checklist

- Platform Transparency: Does the protocol publish real-time proof of reserves? If not, the risk of hidden insolvency is too high.

- Collateral Diversity: Overexposure to a single asset class can wipe out your principal in a flash crash.

- Regulatory Alignment: Is the platform operating in a jurisdiction with clear crypto lending laws? Uncertainty here is a long-term threat.

Monitoring Your Position

Don’t set it and forget it. Regularly review your lending positions against market conditions. If the yield drops below inflation plus a risk premium, it may be time to reallocate. The most successful lenders are those who treat crypto lending as a dynamic portfolio component, not a passive income stream.

Frequently asked questions about crypto lending

Is crypto lending profitable?

Yes, but it comes with specific conditions. According to industry analysis, crypto-backed lending can open up additional revenue streams for lenders through loan interest and cross-selling services like custody [1]. Because cryptocurrencies can be liquidated in real-time, lenders can significantly reduce risk compared to traditional unsecured loans, making it a potentially profitable, albeit complex, strategy for 2026.

What are the risks of crypto lending?

The primary risk is volatility. If the value of the placed cryptocurrency drops significantly, borrowers may face margin calls, requiring them to provide more collateral or risk losing their assets [2]. Beyond market fluctuations, platform security and transparency are critical factors that can determine whether your capital remains safe or disappears entirely.

How do I choose a crypto loan platform?

When evaluating platforms, prioritize security, transparency, and actual usability over headline interest rates. A platform’s track record in handling audits, its regulatory compliance status, and the clarity of its smart contracts are far more important than short-term yield promotions. Always verify that the platform has a history of solvency and clear risk management protocols.

No comments yet. Be the first to share your thoughts!