Market infrastructure shifts

The 2026 crypto lending landscape bifurcates into two operational models: centralized finance (CeFi) and decentralized finance (DeFi). CeFi platforms offer custodial control and bank-like interfaces, while DeFi protocols provide permissionless access via smart contracts. This divergence dictates your risk profile and yield potential.

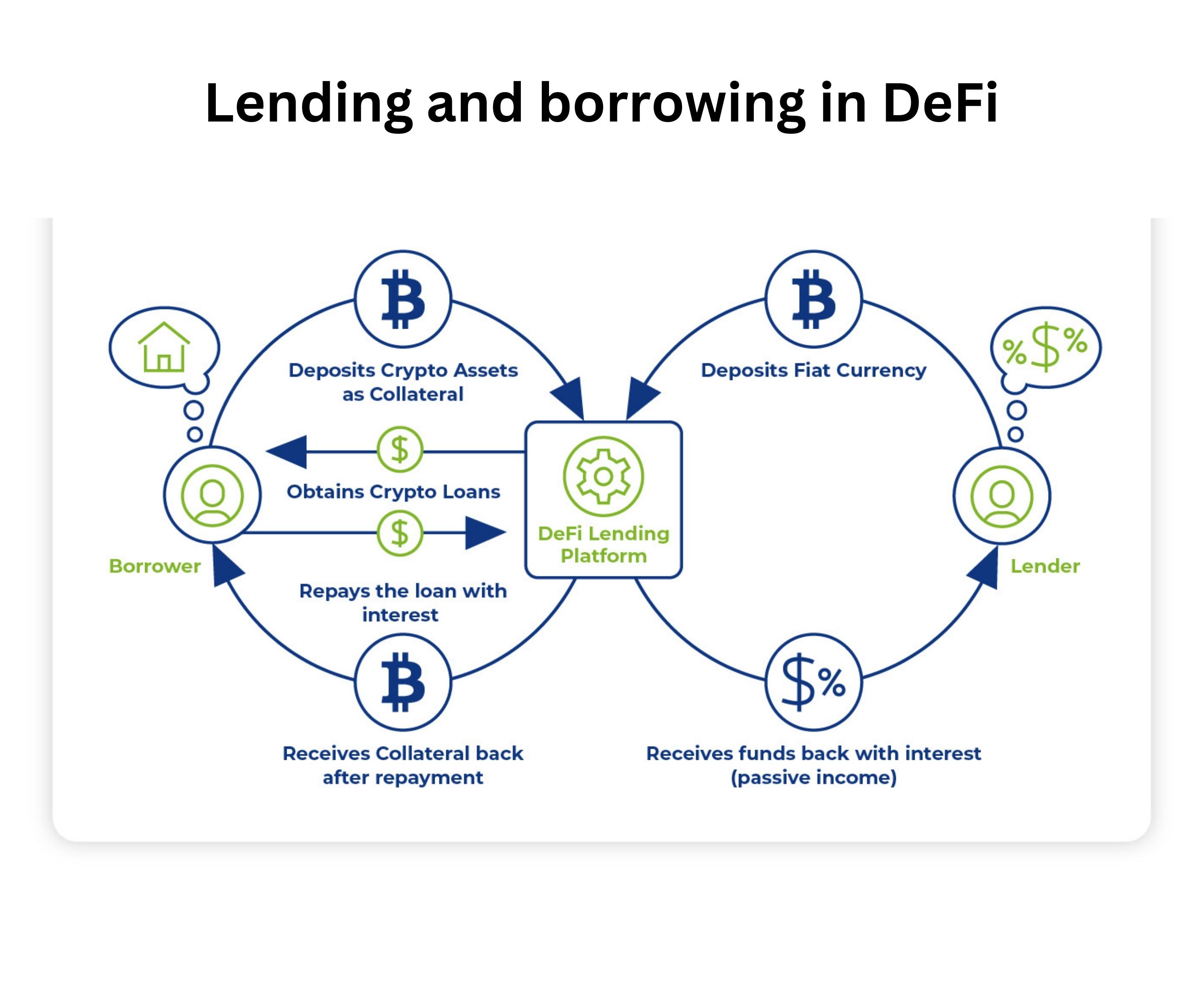

CeFi platforms like Coinbase or Binance act as custodians, pooling user funds to lend to institutional borrowers or for margin trading. This structure mirrors traditional banking, offering regulatory recourse and a single point of contact. However, it introduces counterparty risk; if the platform faces insolvency, user funds may be frozen. DeFi protocols like Aave or Compound automate lending through smart contracts. Borrowers must overcollateralize loans, typically depositing more value than they borrow, to mitigate default risk. This transparency allows real-time solvency audits but exposes users to smart contract vulnerabilities.

Centralized lending platforms

CeFi platforms serve as the bridge between digital assets and real-world liquidity, handling custody, compliance, and fiat off-ramps. They manage risk through proprietary algorithms or institutional lending desks, removing the need for users to manage gas fees or smart contracts.

Platforms like Nexo and SALT Lending streamline borrowing against crypto holdings. Nexo offers interest-paying accounts and instant loans, while SALT focuses on business capital using Bitcoin-backed loans. This infrastructure supports high-stakes decisions by providing predictable liquidity without forcing asset sales. However, CeFi is best suited for short-term liquidity needs. The lack of transparency in yield generation and concentration of risk necessitate diversification across multiple platforms. Always verify regulatory status and insurance coverage.

| Platform | APY Range | Collateral Types | Liquidity |

|---|---|---|---|

| Nexo | Up to 8% | BTC, ETH, USDT, etc. | Instant loans |

| SALT Lending | Variable | Bitcoin primarily | 1-2 business days |

| Celsius (Historical) | Up to 18.5% | BTC, ETH, stablecoins | Restricted (defunct) |

| BlockFi (Historical) | Up to 8.6% | BTC, ETH, stablecoins | Variable (defunct) |

Decentralized lending protocols

DeFi protocols operate as automated market makers for loans, relying on smart contracts rather than central intermediaries. Users deposit crypto into liquidity pools, and borrowers borrow directly from these pools. Interest rates are determined by supply and demand algorithms.

The core mechanic is over-collateralization. Without credit checks, borrowers must lock up more value than they wish to borrow. For example, depositing $150 of Ethereum to borrow $100 of a stablecoin creates a buffer against price drops. If the loan-to-value (LTV) ratio falls below a threshold, collateral is liquidated automatically.

Yield comes from borrower interest and protocol token incentives. Some platforms reward liquidity providers with governance tokens, boosting APY but adding volatility. Always audit contract history and check for reviews by reputable security firms.

Risk management and collateral

A robust crypto lending strategy treats collateral as a safety net, not a margin for error. Liquidations occur rapidly during market dips. If collateral value drops below the required threshold, the system sells it to cover the loan. Managing Loan-to-Value (LTV) ratios with a volatility buffer is essential.

1. Set conservative LTV targets

Avoid maxing out borrowing power. While platforms may allow 75% LTV, setting a personal limit of 50% to 60% provides a buffer against a 20% market correction. This prevents forced liquidation during sharp drops.

2. Choose stable, high-liquidity collateral

Pledge major cryptocurrencies like BTC or ETH with deep order books. Avoid niche altcoins, as their prices can gap down with little warning, leaving insufficient coverage. High-liquidity assets ensure fair market pricing during liquidations.

3. Monitor and rebalance regularly

LTV ratios change with every price tick. Set alerts for when your LTV approaches the danger zone. Add collateral or repay debt to restore safety. Regular monitoring prevents the "set it and forget it" mindset.

Read the platform’s liquidation policy before depositing. Understand the exact LTV threshold and associated fees. Some platforms offer grace periods; others act instantly.

Determine the maximum price drop your collateral can withstand. If your LTV is 50%, a 50% drop wipes out equity. Plan for a 30-40% drop without liquidation to define your risk tolerance.

Use platform tools or dashboards to track LTV in real-time. Set alerts at 70%, 80%, and 90% of your danger threshold to act proactively before forced liquidation.

| Feature | CeFi Lending | DeFi Lending |

|---|---|---|

| Liquidation Trigger | Platform-specific LTV threshold | Oracle-based price feed |

| Speed of Liquidation | Minutes to hours | Seconds (block-based) |

| Collateral Type | Major coins (BTC, ETH) | Broad (including stablecoins) |

| Risk of Insolvency | Counterparty risk | Smart contract risk |

CeFi liquidations take minutes to hours, offering a small window to add funds. DeFi executes liquidations in seconds via automated contracts. This speed makes DeFi more capital-efficient but dangerous if unmonitored. Keep LTV well below trigger points to avoid flash crash losses.

Yield Optimization Tactics

Maximizing returns requires moving beyond simple deposit yields. Understanding leverage and arbitrage mechanics allows for higher returns while managing volatility risks.

Stablecoin Arbitrage

This strategy exploits interest rate differences between CeFi and DeFi. CeFi platforms often offer lower stablecoin lending rates due to high demand for collateralized borrowing. DeFi protocols like Aave or Compound may offer higher variable rates during high borrowing demand. Arbitrageurs borrow stablecoins from low-yield CeFi sources and lend them into high-yield DeFi protocols. Success depends on monitoring rates in real-time and ensuring the spread exceeds transaction costs and slippage.

Leveraging Low-Interest Loans

Use low-interest crypto loans to acquire higher-yielding assets. Borrowing a stablecoin at 5% APR to deposit into a pool yielding 8-10% locks in a 3-5% spread. This leverages capital without risking principal holdings, provided collateral remains stable. Use blue-chip collateral like Bitcoin or Ethereum at conservative LTV ratios. Ensure the yield consistently outpaces the loan interest cost.

Risk Management in Yield Optimization

Leverage and arbitrage amplify gains and losses. A sudden collateral price drop can trigger liquidation. Smart contract risks in DeFi can lead to total loss. Maintain healthy collateral buffers and diversify yield sources across multiple protocols to mitigate single-point failures.

Is crypto lending a good investment?

Crypto lending offers a clear path to yield, often outpacing traditional savings accounts, but it demands active risk management. You are effectively acting as the bank, bearing the risk of platform insolvency and smart contract failure. Unlike bank deposits, there is no FDIC insurance. Capital is exposed to borrower defaults, platform hacks, and regulatory shifts. High returns are the premium for bearing this unsecured risk.

No comments yet. Be the first to share your thoughts!