Why crypto lending feels restrictive right now

The crypto lending landscape has shifted from a Wild West of high yields to a regulated, risk-aware market. Lenders are no longer chasing double-digit APYs on uncollateralized loans; instead, they are focusing on secured lending backed by real-world assets (RWA) and AI-driven risk models. This shift means borrowing costs have become more transparent but also more rigid. Platforms now demand stricter collateralization ratios and real-time monitoring of asset volatility.

For borrowers, this means the "easy money" era is over. You can still borrow against your crypto holdings, but you must provide significantly more collateral than before. For example, borrowing against Bitcoin might require a 150% loan-to-value (LTV) ratio, meaning you lock up $150 of BTC to borrow $100. This reduces leverage but protects lenders from sudden market crashes.

Lenders, meanwhile, are using AI to assess counterparty risk more accurately. Traditional credit scores don't apply in crypto, so platforms analyze on-chain behavior, transaction history, and even social reputation scores. This allows for more nuanced lending decisions but also means that new or low-activity wallets may face higher interest rates or rejection.

The result is a market that is safer but less accessible. If you're looking to leverage your crypto assets, you'll need to navigate these stricter requirements carefully. Understanding the underlying mechanics of collateralization and risk assessment is now more important than ever.

Crypto lending choices that change the plan

Crypto lending offers immediate liquidity without triggering taxable events from selling your assets. However, the mechanism introduces specific risks that differ significantly from traditional finance. You are trading counterparty risk and market volatility for access to capital. Understanding these tradeoffs is essential before locking up your digital assets.

Liquidity and Loan-to-Value Ratios

The Loan-to-Value (LTV) ratio determines how much you can borrow against your collateral. Conservative LTVs (50-60%) reduce the risk of liquidation but limit your access to funds. Aggressive LTVs (70-80+) maximize liquidity but leave little room for price drops. If the collateral price falls below the maintenance threshold, you face instant liquidation, losing your assets to cover the loan. This is the primary mechanical risk in crypto lending.

Interest Rates and Borrowing Costs

Lending rates fluctuate based on supply and demand dynamics within the protocol or platform. Fixed-rate loans offer predictability but often come with higher initial costs or stricter terms. Variable rates can be lower initially but may spike during periods of high market demand for stablecoins. Additionally, some platforms charge origination fees or require the borrower to hold platform-specific tokens, adding hidden layers of cost to the effective annual percentage rate (APR).

Counterparty and Platform Risk

The safety of your collateral depends entirely on the entity holding it. Centralized exchanges may commingle user funds, exposing you to insolvency risks similar to the FTX collapse. Decentralized protocols offer transparency but carry smart contract risk; bugs or exploits can lead to total loss. Always verify if the platform is fully collateralized and whether they have undergone recent security audits. Insurance funds may offer partial protection, but they are not a guarantee against total protocol failure.

Regulatory and Jurisdictional Exposure

Crypto lending is heavily scrutinized by regulators globally. Some jurisdictions have banned or restricted lending services, potentially freezing your access to funds if your account is flagged. Platform compliance measures may require identity verification (KYC) that compromises your privacy. Regulatory changes can alter the tax treatment of lending rewards or loan interest, impacting your net returns unexpectedly.

How to evaluate crypto lending platforms

Choosing a platform is the most critical decision in crypto lending. The infrastructure has shifted from simple CeFi wrappers to complex RWA integrations and AI-driven risk models. A platform’s stability depends less on its marketing and more on its custody solutions, collateral liquidation logic, and compliance posture. Use this framework to assess risk before depositing assets.

Start by checking where your assets are held. Legitimate platforms segregate user funds from operational capital. Look for proofs of reserves or third-party audit reports. If the platform commingles funds or lacks transparency, the risk of insolvency increases significantly. Avoid platforms that promise guaranteed returns without clear custody mechanisms.

Modern lending often involves Real World Assets (RWA) as collateral or yield sources. Evaluate how the platform values these assets. Does it use real-time oracle data or stale pricing? AI-driven risk analysis should adjust loan-to-value (LTV) ratios dynamically based on market volatility. Platforms that rely on static LTVs during high volatility are prone to under-collateralized loans and bad debt.

Liquidation is the safety valve of crypto lending. Understand the liquidation threshold and the grace period. A robust platform uses automated, transparent liquidation bots that act quickly to protect lenders. If the liquidation process is manual or opaque, you risk significant losses during market crashes. Ensure the platform has a history of smooth liquidations during past market downturns.

Compliance reduces the risk of sudden platform shutdowns. Check if the platform is registered in a jurisdiction with clear crypto regulations. Look for KYC/AML procedures, which, while inconvenient, signal a commitment to regulatory standards. Platforms operating in regulatory gray areas may face legal challenges that could freeze your assets. Prioritize platforms with clear legal entities and compliance teams.

Yield in crypto lending comes from interest, trading fees, or RWA returns. Ensure the yield is sustainable and not a subsidy to attract users. High yields often indicate high risk or unsustainable business models. Compare the platform’s fees against industry standards. Hidden fees can erode returns significantly over time. Choose platforms with transparent, competitive fee structures.

Spotting the traps in crypto lending

Crypto lending promises passive income, but the infrastructure behind it often hides significant risks. As real-world asset (RWA) infrastructure and AI-driven risk analysis become standard, distinguishing between robust platforms and misleading claims is critical. Many projects overstate their AI capabilities or underreport their exposure to volatile collateral.

Overstated AI risk models

Some platforms market "AI-driven" underwriting without disclosing the data sources or logic. True AI models require transparent, high-quality data feeds, not just a buzzword. If a platform cannot explain how its algorithm assesses borrower creditworthiness or collateral health, treat it as a black box. This opacity often masks poor risk management practices that only reveal themselves during market stress.

Hidden RWA liquidity gaps

Real-world assets are touted for stability, but they suffer from illiquidity. If a lending pool is heavily backed by illiquid RWAs, borrowers may face delays in accessing funds or platforms may struggle to liquidate collateral during a crash. Check the asset composition. A healthy platform balances crypto collateral with RWAs that have clear, secondary markets.

Misleading yield claims

High yields often signal high risk, not superior technology. Platforms promising returns significantly above market averages may be using depositor funds to pay existing investors (a Ponzi-like structure) or taking excessive leverage. Compare the offered rate against risk-free rates and peer platforms. If the spread is unreasonably wide, the risk of loss is likely higher than the potential gain.

Weak collateralization ratios

Some platforms offer low loan-to-value (LTV) ratios to attract borrowers, but this can be a trap. Low LTVs might seem safe, but if the platform lacks robust liquidation mechanisms, a sudden price drop can leave the lender with worthless collateral. Ensure the platform has automated, frequent liquidation triggers and sufficient insurance funds to cover shortfalls.

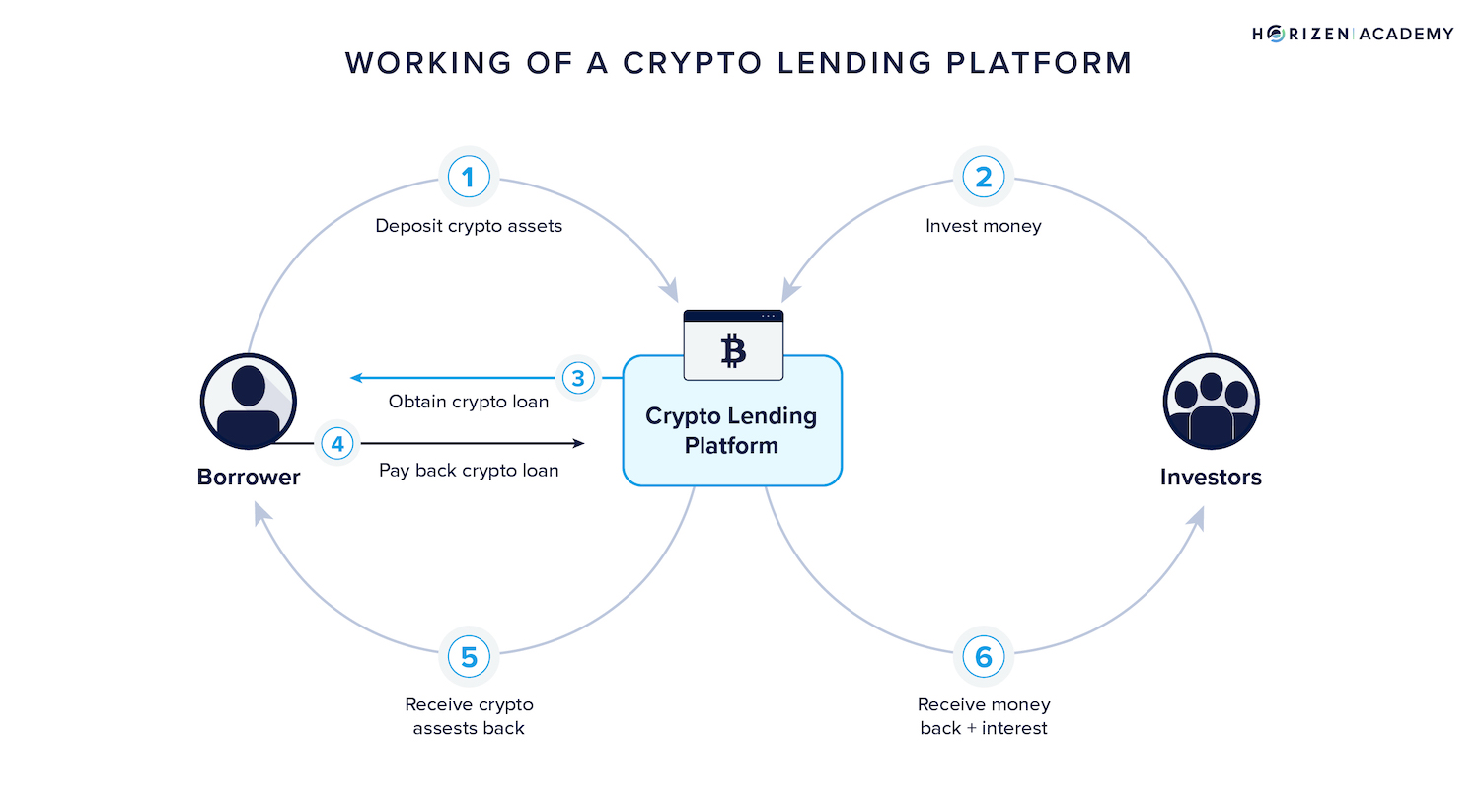

Crypto lending: what to check next

Crypto lending connects borrowers with lenders through digital platforms, offering yields that often outperform traditional savings accounts. However, the mechanics differ significantly from bank deposits, requiring a clear understanding of how value flows between parties.

No comments yet. Be the first to share your thoughts!