Crypto lending limits to account for

Crypto lending requires a clear sequence: define the constraint, compare realistic options, test the tradeoff, and choose the path with the fewest hidden costs. This order keeps the advice usable.

Crypto lending choices that change the plan

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Choose the next step: Turn research into a practical decision framework

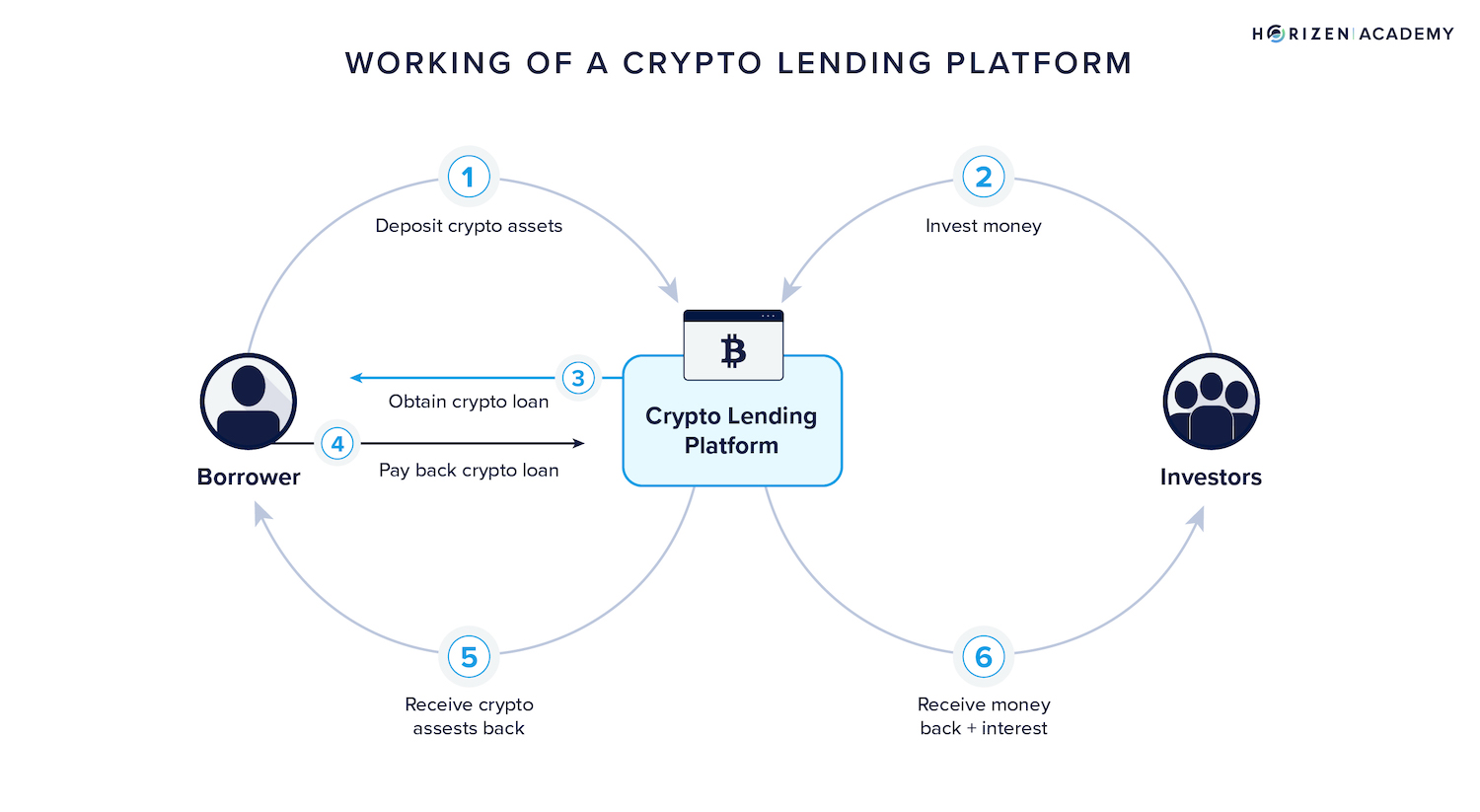

Navigating institutional crypto lending requires moving beyond headline yields to assess structural safety. You are not just borrowing against an asset; you are entering a secured loan agreement with specific accounting and risk implications. Use this framework to select the lending vehicle that matches your capital preservation goals.

Institutional platforms typically require over-collateralization to protect lenders during volatility. A 50% loan-to-value (LTV) ratio means you must pledge $2 in Bitcoin to borrow $1 in fiat. This buffer prevents immediate liquidation during minor market dips, but it also ties up more capital than traditional secured loans. Always calculate the liquidation threshold, not just the initial LTV, to understand your downside risk.

The safety of your collateral depends entirely on how the platform holds your assets. Institutional infrastructure requires clear proof of segregation, ensuring your crypto is not commingled with the platform’s operational funds or used for unsecured proprietary trading. Look for regulated custodians and regular attestation reports that confirm the platform holds sufficient reserves to back every dollar lent out.

Lending arrangements often trigger complex tax events and accounting classifications. As noted in PwC’s Viewpoint, lending may require the borrower to pay fees in crypto assets while returning the principal in kind, creating taxable income events at each payment interval. Consult a tax professional to understand how interest payments, collateral appreciation, and liquidation events impact your specific jurisdiction’s reporting requirements.

High yields often signal higher risk or unsustainable business models. Institutional lending yields are generally derived from institutional borrowing demand, not speculative DeFi incentives. Scrutinize whether the yield is backed by real economic activity, such as hedge fund leverage or corporate treasury management, rather than token emissions that dilute value over time.

| Feature | Centralized Lending | DeFi Lending |

|---|---|---|

| Custody | Platform-held, regulated | Self-custodied, smart contract |

| KYC/AML | Required | None/Permissionless |

| Yield Source | Institutional borrowing | Protocol fees/liquidity mining |

Watch Out for Weak Crypto Lending Options

Not every platform offering crypto-backed loans provides the same level of security or value. As institutional infrastructure matures, distinguishing between robust lending models and risky setups becomes critical for protecting your collateral.

Hidden Fees and Low Loan-to-Value Ratios

Some platforms advertise high yields but compensate with aggressive liquidation thresholds. A low loan-to-value (LTV) ratio means a small market dip triggers forced selling. Always calculate the liquidation price against your entry point before borrowing.

Opaque Custody and Unaudited Reserves

Avoid lenders that do not publish real-time proof of reserves. Without third-party audits or on-chain verification, you cannot confirm they hold your collateral securely. This lack of transparency is a major red flag in 2026’s market.

Regulatory Misalignment

Certain platforms operate in regulatory gray areas, exposing users to sudden service suspensions. Stick to institutions with clear compliance frameworks and established legal standings to ensure your assets remain accessible during market volatility.

Crypto lending: what to check next

Before committing capital or collateral, clarify how the loan structure impacts your tax liability and asset ownership. These practical answers address the most common objections readers face when navigating institutional crypto lending infrastructure.

No comments yet. Be the first to share your thoughts!