How crypto lending works today

Crypto lending is a financial transaction where one party lends cryptocurrency to another in exchange for compensation. While the end goal mirrors traditional finance—borrowers get liquidity and lenders earn yield—the infrastructure supporting these transactions has split into two distinct models. Understanding the difference between centralized and decentralized lending is the first step in assessing risk.

Centralized lending (CeFi)

Centralized platforms operate similarly to traditional banks or brokerages. You deposit your assets into a platform-controlled wallet, and the institution manages the lending process. In this model, you are relying on counterparty trust. The platform acts as an intermediary, vetting borrowers, managing collateral, and handling repayments.

This structure offers convenience and often higher yields because the platform can aggregate capital and lend to institutional borrowers or engage in proprietary trading strategies. However, it introduces significant counterparty risk. If the platform mismanages funds or faces insolvency, your assets may be frozen or lost, as there is no on-chain guarantee of their safety. This dynamic was highlighted by major failures in the sector, where user funds were commingled and used without clear oversight.

Decentralized lending (DeFi)

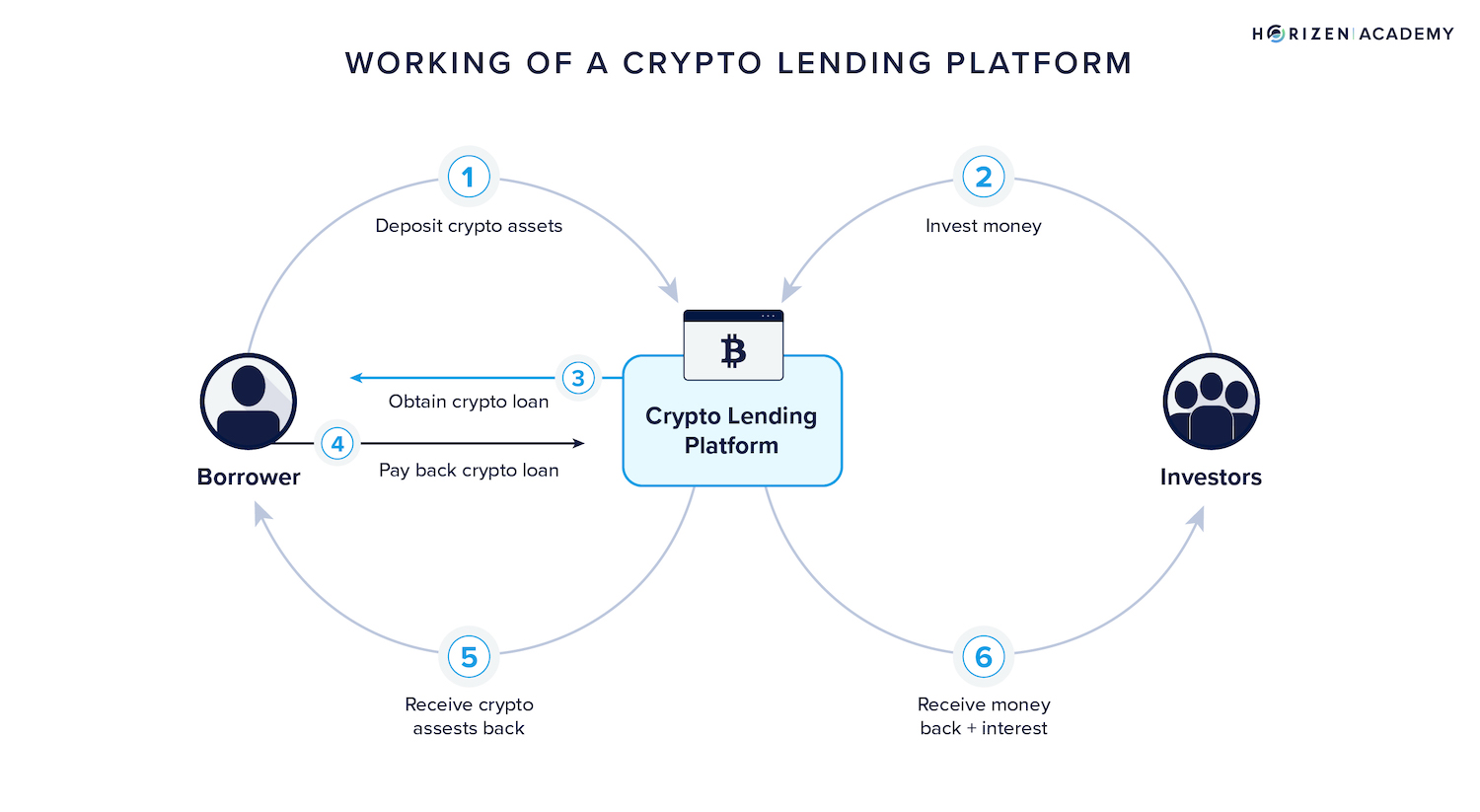

Decentralized lending removes the middleman by using self-executing smart contracts on a blockchain. Instead of depositing funds into a company’s custody, you interact directly with a protocol. Borrowers must typically provide overcollateralization—depositing more value in crypto assets than they wish to borrow. This collateral is locked in the smart contract.

If the value of the collateral drops below a certain threshold, the contract automatically liquidates the assets to repay the lender. This mechanism significantly reduces the risk of default compared to unsecured loans. However, it introduces smart contract risk. Bugs, exploits, or coding errors in the protocol can lead to the loss of funds, and the complexity of DeFi interfaces can be a barrier for non-technical users.

The baseline for risk assessment

Regardless of the model, crypto lending is not risk-free. In CeFi, your primary risk is the solvency and transparency of the lending entity. In DeFi, your risks include smart contract vulnerabilities, oracle failures (where price feeds are manipulated), and the volatility of the underlying collateral.

Lenders should view yields not just as income, but as compensation for these specific risks. Before committing capital, it is essential to audit the platform’s track record, understand who holds custody of the assets, and verify the technical security of any smart contracts involved.

Track market rates and liquidity

Crypto lending rates are not static; they fluctuate with market volatility and platform demand. Understanding these movements is essential for assessing both potential yield and liquidation risk. When Bitcoin or Ethereum prices drop, the value of your collateral shrinks, potentially triggering forced liquidations if you do not maintain adequate buffers.

To monitor these conditions, you can use live market widgets. The following chart shows recent BTC price action, which directly influences lending health. A sharp decline often correlates with tighter lending terms or higher interest rates as platforms try to attract more liquidity.

For a broader view of asset performance, you can also track live prices for major collateral assets. This helps you gauge the current market sentiment and adjust your lending strategies accordingly.

Real-world asset yields and DeFi infrastructure

The crypto lending landscape is shifting from pure speculation toward tokenized real-world assets (RWA). This transition bridges traditional finance (TradFi) and decentralized finance (DeFi), offering yields backed by tangible value rather than volatile token premiums. However, this bridge introduces complex infrastructure risks that differ significantly from native crypto lending.

To understand the shift, we must compare the underlying mechanics of RWA lending against traditional crypto-backed loans. The table below highlights the structural differences in yield sources, risk profiles, and regulatory exposure.

| Feature | RWA Lending | Traditional Crypto Lending |

|---|---|---|

| Yield Source | Real-world cash flows (e.g., treasury bills, corporate debt) | Borrower demand for leverage and market volatility premiums |

| Collateral Type | Tokenized real-world assets (RWAs) or stablecoins backed by RWAs | Native crypto assets (e.g., BTC, ETH, SOL) |

| Primary Risk | Credit risk of the underlying issuer and legal enforceability | Smart contract risk and rapid collateral liquidation |

| Regulatory Exposure | High (subject to securities and banking regulations) | Moderate to Low (often treated as property or commodity) |

| Liquidity | Lower; depends on secondary markets for tokenized assets | High; instant on-chain trading and liquidation |

The core infrastructure risk in RWA lending lies in the legal bridge. When a token represents a treasury bill or a corporate loan, the smart contract must have a legal claim on the underlying asset. If the legal entity holding the real-world asset defaults, or if the tokenization structure is legally ambiguous, the on-chain collateral may be worthless. This is a credit risk, not just a market risk.

In contrast, traditional crypto lending relies on over-collateralization and automated liquidations. If Bitcoin drops, the protocol sells the collateral to cover the loan. There is no legal counterparty risk, only smart contract risk. As the IMF notes in their guidance on macroeconomic statistics, the recording of these transactions depends heavily on whether the crypto asset acts as a liability or a pure store of value. RWA lending blurs this line, creating hybrid instruments that require rigorous legal due diligence.

Investors must look beyond the yield percentage. A 5% yield from a tokenized treasury bill carries legal and counterparty risks that a 0% yield from a pure crypto loan does not. The infrastructure is not just code; it is law.

Key risks in crypto lending

Crypto lending isn’t just about chasing higher yields; it’s about understanding where the money actually goes and what happens when things break. Unlike traditional banking, where your deposits are often insured by government agencies, crypto lending platforms operate in a wilder frontier. The risks here are structural, technical, and regulatory. Ignoring them is a fast track to losing your principal.

Smart contract vulnerabilities

At the heart of most crypto lending protocols is code. When you deposit assets, you’re interacting with smart contracts—self-executing programs that manage the lending and borrowing logic. If there’s a bug or a vulnerability in that code, hackers can exploit it. We’ve seen billions drained from lending protocols due to simple coding errors or complex flash loan attacks. Once the code is deployed, it’s often immutable. There’s no customer service line to call to reverse a transaction. You are relying entirely on the security audit and the integrity of the developers. A single oversight can wipe out the liquidity pool overnight.

Counterparty insolvency

Even if the code is perfect, the entity behind the platform might not be. Centralized lending platforms act as intermediaries, holding your assets in their custody. If they lend out those assets to risky borrowers or engage in speculative trading with your funds, they can become insolvent. The collapse of Celsius, Voyager, and Three Arrows Capital showed us that even large, well-known platforms can vanish when their risk management fails. In these cases, you are an unsecured creditor. The likelihood of recovering your full deposit is often slim, and the process can take years, if it happens at all. Always check who is holding your assets and what their balance sheet looks like.

Regulatory shifts

The regulatory landscape for crypto is still being written, and it’s changing rapidly. Governments are increasingly scrutinizing lending platforms, especially those that offer yield-like returns without clear regulatory oversight. A sudden regulatory crackdown can lead to platform shutdowns, frozen withdrawals, or forced compliance measures that disrupt the entire ecosystem. For example, if a platform is deemed an unregistered securities exchange, it may be forced to shut down in certain jurisdictions. This uncertainty adds a layer of risk that doesn’t exist in traditional finance. Staying informed about regulatory developments in your region is not just good practice; it’s essential for protecting your capital.

Steps to start crypto lending safely

Launching a crypto lending position requires more than just finding the highest yield. It demands a rigorous workflow that prioritizes security and due diligence over speed. Treat your capital like a business asset, not a lottery ticket.

Before depositing funds, check if the protocol has undergone third-party security audits from reputable firms. Look for active insurance coverage or a transparent bug bounty program. This is your first line of defense against smart contract vulnerabilities.

Understand the Loan-to-Value (LTV) ratio and liquidation thresholds. If the market drops, how much room do you have before your position is liquidated? Avoid platforms with thin liquidity or unstable collateral types that could suffer from sudden depegging events.

Enable multi-factor authentication (MFA) using an authenticator app, not SMS. Use a hardware wallet for any significant deposits. Never share seed phrases or private keys. Your security hygiene is just as important as the protocol's code.

Don’t put all your capital into a single lending protocol. Spread your exposure across multiple reputable platforms to mitigate the risk of a single point of failure. This diversification protects you if one platform experiences technical issues or insolvency.

Common questions about crypto lending

Crypto lending sits at the intersection of high yield and structural risk. Understanding the mechanics of profitability, entry barriers, and tax treatment is essential before deploying capital.

Is lending crypto profitable?

Yes, but yields fluctuate with market demand. Lenders earn interest from borrowers and can cross-sell custody services. Because crypto collateral can be liquidated in real-time, platforms can manage risk more aggressively than traditional banks, often passing those savings to lenders. However, platform insolvency remains a counterparty risk that pure yield calculations often ignore.

How do I start crypto lending?

Start by selecting a reputable lending platform that aligns with your risk tolerance. Once chosen, deposit your cryptocurrencies into the platform’s designated wallet. You then set your lending terms, such as the interest rate and loan duration. Always verify the platform’s security audits and insurance coverage before transferring significant assets.

What is the 30-day rule in crypto?

The "30-day rule" typically refers to the wash sale rule, which currently applies to spot Bitcoin ETFs rather than direct crypto assets. If you sell a spot Bitcoin ETF at a loss and buy it back within 30 days, the IRS may disallow that loss for tax purposes. Direct crypto-to-crypto trades generally do not trigger wash sale rules yet, but regulations are evolving.

No comments yet. Be the first to share your thoughts!