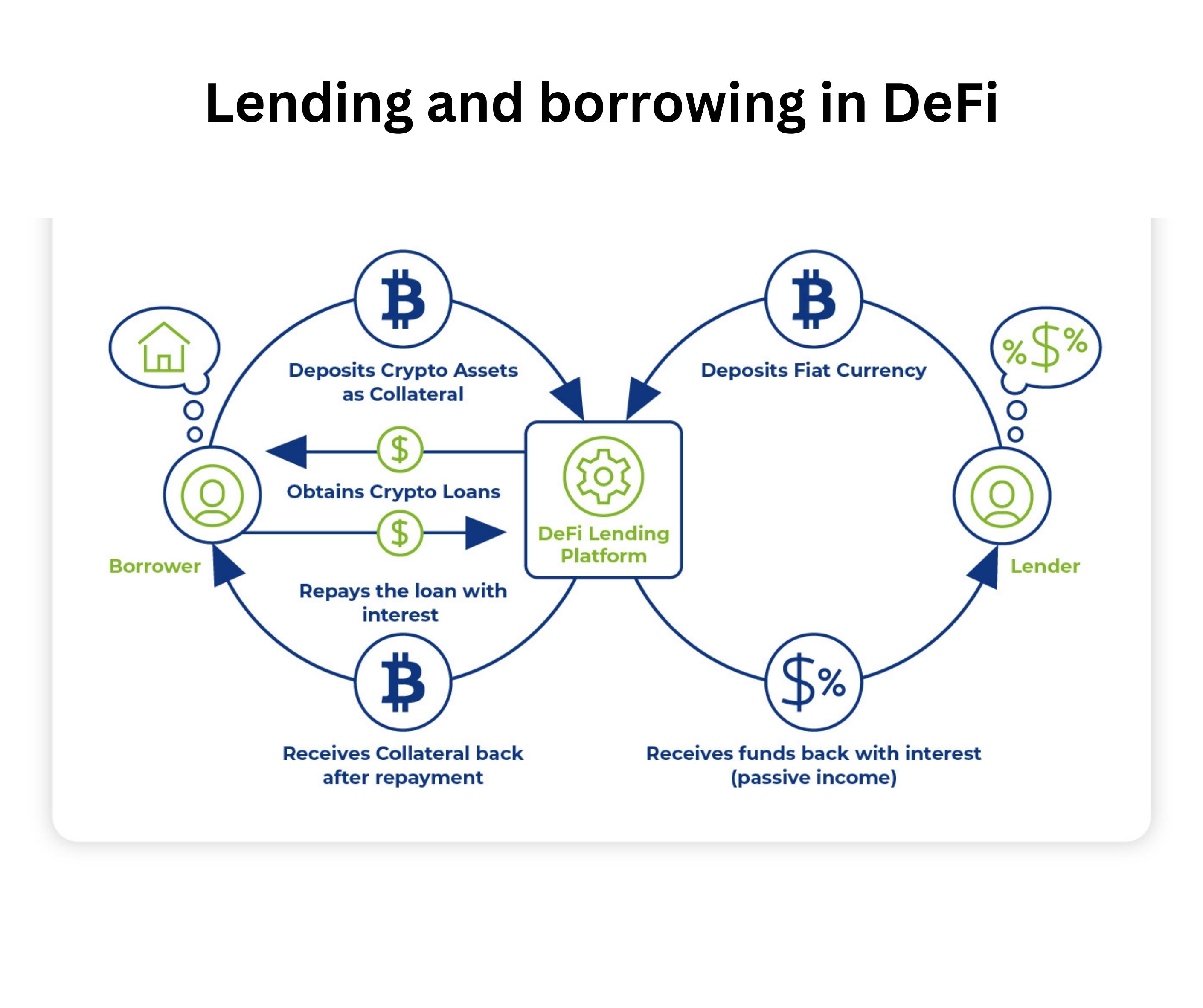

How crypto lending works

Crypto lending is a financial transaction where one party lends cryptocurrency to another party in exchange for compensation, typically in the form of interest or yield. At its core, it mirrors traditional finance but operates on blockchain infrastructure, allowing for faster settlement and often higher returns. However, the mechanisms that secure these loans differ significantly between centralized exchanges (CeFi) and decentralized finance (DeFi) protocols.

To understand the landscape, you need to distinguish between the two primary structures: collateralized and uncollateralized lending. Most crypto lending today is collateralized. This means the borrower must lock up assets worth more than the loan amount to secure the position. If the value of the collateral drops below a certain threshold, the protocol or exchange can liquidate the assets to cover the loss. This over-collateralization is the safety net that makes lending volatile digital assets possible without credit checks.

Uncollateralized lending is rarer and riskier. It relies on the borrower’s creditworthiness or smart contract reputation rather than locked assets. While this allows for borrowing without tying up capital, it introduces significant counterparty risk. If the borrower defaults, the lender has little recourse. This is why the majority of yield-generating opportunities you see today are built on collateralized models, where the asset itself acts as the guarantee.

The volatility of the underlying asset, like Bitcoin, directly influences lending rates. When markets are turbulent, lenders demand higher yields to compensate for the risk of liquidation, while borrowers may face stricter collateral requirements. Understanding this dynamic is essential before committing capital to any lending platform.

CeFi vs DeFi lending platforms

When you start looking for yield in crypto, you will quickly hit two distinct infrastructure models: centralized finance (CeFi) and decentralized finance (DeFi). Both let you lend your assets, but they handle custody, transparency, and risk in fundamentally different ways. Choosing between them is less about which is "better" and more about what kind of trade-off you are willing to accept.

CeFi platforms operate like traditional banks. You deposit your crypto into an account managed by a company, and they handle the lending process for you. The interface is familiar, customer support exists, and withdrawals are usually instant. However, this convenience comes with a significant caveat: you do not hold the keys. Your assets are pooled and lent out to institutional borrowers, hedge funds, or used for proprietary trading. If the platform mismanages those funds or faces insolvency, your access to your capital is at the mercy of their solvency and regulatory standing. This is the central bank risk of CeFi.

DeFi lending, by contrast, runs on smart contracts deployed on public blockchains like Ethereum or Solana. There is no company to call if something goes wrong. Instead, your funds are locked in code that automatically matches lenders with borrowers. You retain custody of your assets until they are deposited, and the terms of the loan are visible on-chain for anyone to audit. This transparency is powerful, but it introduces smart contract risk. If the code has a bug or is exploited by a hacker, there is no customer service team to reverse the transaction. You are responsible for your own security.

The following table breaks down the structural differences between these two models.

| Feature | CeFi (Centralized) | DeFi (Decentralized) |

|---|---|---|

| Custody | Platform holds private keys | User holds keys via wallet |

| Transparency | Audited reports (varying quality) | On-chain code (publicly verifiable) |

| Counterparty Risk | High (platform insolvency) | Medium (smart contract bugs) |

| Yield Source | Institutional loans, proprietary trading | Peer-to-peer borrower interest |

| Access Control | KYC/AML required | Permissionless (no ID needed) |

The choice often comes down to your comfort with technical complexity versus institutional trust. If you prioritize ease of use and are comfortable trusting a regulated entity with your assets, CeFi offers a smoother experience. If you prefer full control and want to verify the mechanics of your yield yourself, DeFi is the more transparent, albeit riskier, path.

Where the yield actually comes from

When you deposit crypto into a lending platform, you aren’t just parking your assets in a digital safe. You are actively participating in a market where capital is rented out to borrowers. Understanding the source of these returns is essential for a realistic Crypto Lending guide, as the yield you see is rarely free money—it is compensation for specific risks and services.

Trading Fees and Market Making

A significant portion of yield, particularly in decentralized finance (DeFi), comes from liquidity provision. When you supply assets to a lending pool or automated market maker, you are enabling traders to swap tokens instantly. In return, you collect a share of the trading fees generated by those swaps.

This mechanism ties your returns directly to market volatility. When trading volume spikes, fees—and thus yields—rise. However, this also exposes you to impermanent loss if the asset price moves significantly against your position. It is a high-activity income stream that requires active monitoring rather than passive holding.

Institutional Borrowing

In both centralized finance (CeFi) and institutional-grade DeFi protocols, a major driver of yield is institutional borrowing. Hedge funds, market makers, and other large entities often need to borrow crypto to execute strategies like short selling or arbitrage. They post collateral and pay interest to access that liquidity.

These borrowers typically seek large, stable lines of credit. Because they are professional entities, the interest rates they pay are often more stable and predictable than retail-driven yields. This segment provides a steady baseline return for lenders, assuming the borrower remains solvent and the collateral is sufficient.

Staking Rewards

For proof-of-stake cryptocurrencies like Ethereum, yield also stems from network staking. When you lend staked assets, the platform often passes on the block rewards and transaction tips earned by validators. This is essentially a dividend for securing the network.

However, staking rewards are not guaranteed. They depend on network activity, validator performance, and potential slashing penalties if the underlying protocol misbehaves. When evaluating a Crypto Lending guide option, always check if the stated yield includes staking rewards or if it is purely from interest, as the risk profiles differ significantly.

Current Market Rates

Yield rates are not static; they fluctuate based on supply and demand dynamics. During bull markets, when traders are eager to leverage up, borrowing demand spikes, pushing lending rates higher. In bear markets, rates often compress as demand for borrowed assets dries up.

To get an accurate picture of current conditions, you should look at live data rather than historical averages. The widget below shows the current price of USDC, a common base asset for lending pairs, helping you gauge the stability of your principal.

Key risks in crypto lending

Crypto lending promises high returns, but those yields come with specific, often severe, risks that differ depending on whether you use a centralized exchange (CeFi) or a decentralized protocol (DeFi). Understanding these mechanics is essential before you deposit your assets.

Smart Contract Exploits

In DeFi lending, your funds are locked in smart contracts—automated code on the blockchain. If there is a bug or vulnerability in that code, hackers can exploit it, draining the protocol’s liquidity. Unlike traditional banks, there is no customer support to reverse a transaction once the exploit occurs. Even audited contracts can fail due to unforeseen logic errors or oracle manipulation, where fake price data triggers false liquidations.

Platform Insolvency (CeFi)

Centralized lending platforms act like traditional banks, pooling your assets to lend out at higher rates. The risk here is counterparty risk: if the platform lends too aggressively or invests poorly, it can become insolvent. The collapse of major CeFi lenders in recent years demonstrated how quickly user funds can become inaccessible. Without deposit insurance like FDIC coverage in the US, your crypto is often unsecured debt owed by the company.

Liquidation Cascades

DeFi loans are over-collateralized, meaning you must deposit more value than you borrow. If the value of your collateral drops sharply, the protocol automatically sells it to repay the loan. In volatile markets, this can trigger a cascade: one liquidation lowers the price, triggering more liquidations, causing a "death spiral." This mechanism protects lenders but can leave borrowers with zero collateral and significant debt.

Choosing a lending strategy

Selecting the right crypto lending strategy requires aligning your platform choice with your risk tolerance and liquidity needs. Whether you prioritize the higher yields of decentralized finance (DeFi) or the regulatory clarity of centralized finance (CeFi), the decision hinges on how much control you are willing to surrender for returns.

Centralized platforms often offer insurance funds or regulatory compliance, providing a safety net for conservative investors. However, this comes with counterparty risk—if the platform fails, your assets may be inaccessible. DeFi protocols remove the middleman but expose you to smart contract vulnerabilities and market volatility without a safety net.

If you need immediate access to your funds, CeFi loans or stablecoin lending pools on major DEXs like Aave offer predictable exit options. DeFi strategies like locked staking or longer-term lending agreements often lock your capital for fixed periods, meaning you cannot withdraw without penalty or waiting out the term. Match the asset’s lock-up period to your cash flow requirements.

High yields in DeFi often come with impermanent loss or complex yield farming mechanics. CeFi rates are typically lower but more transparent. Use a

Always calculate the net yield after accounting for trading fees, gas costs, and potential slippage. A 10% APY in DeFi might net 6% after gas and impermanent loss, while a 5% CeFi rate might be all you pay.

Before depositing, check if the protocol has undergone third-party security audits. For CeFi, review their proof-of-reserves documentation. For DeFi, look for established track records and bug bounty programs. Never invest more than you can afford to lose in untested or unaudited protocols.

A

No comments yet. Be the first to share your thoughts!