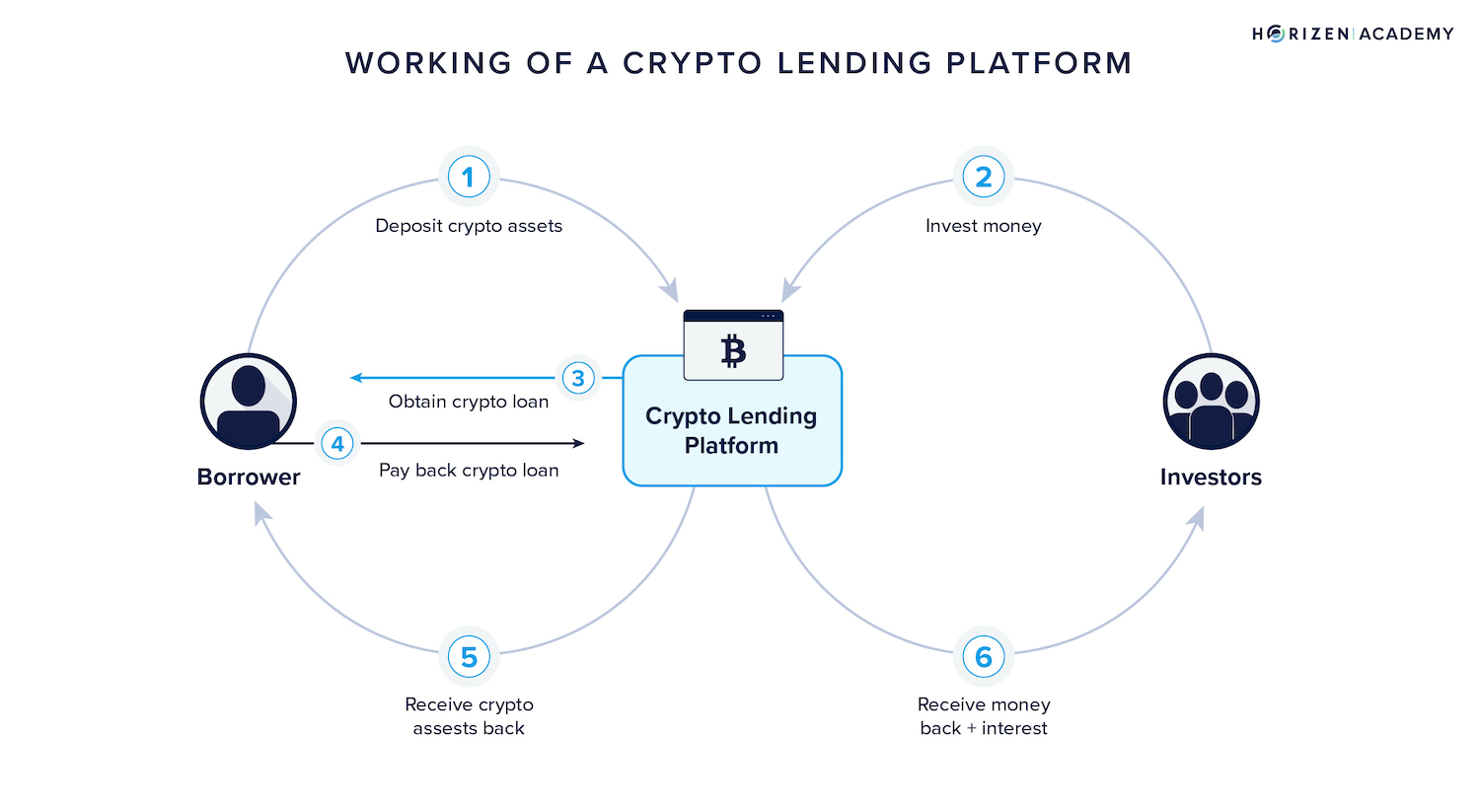

How crypto lending works today

Crypto lending has evolved from a niche DeFi experiment into a structured financial sector with two distinct operating models. Understanding the mechanical differences between these models is essential for evaluating risk and yield. The landscape is primarily divided into centralized, crypto-backed loans and decentralized, algorithmic lending protocols.

Centralized Crypto-Backed Loans

This model functions similarly to a traditional pawn shop or margin loan. You pledge digital assets—such as Bitcoin or Ethereum—as collateral to borrow fiat currency or stablecoins. The platform holds your assets in custody, and you receive a loan-to-value (LTV) ratio based on the collateral's market price. If the value of your collateral drops below a certain threshold, the platform may liquidate your assets to cover the loan.

The primary appeal here is simplicity and access to liquidity without selling your holdings. However, this convenience comes with counterparty risk. You are trusting a centralized entity to manage your assets securely and transparently. Regulatory scrutiny in this space is intensifying, as seen with recent enforcement actions against major exchanges for unregistered securities lending programs.

Decentralized Finance (DeFi) Lending

DeFi lending protocols operate without intermediaries. Instead of a company holding your funds, smart contracts on a blockchain manage the lending pool. Users deposit assets into these pools, and borrowers take out loans by over-collateralizing their positions. Interest rates are determined algorithmically based on supply and demand within the protocol.

This model offers greater transparency and control, as all transactions are recorded on-chain. However, it introduces smart contract risk—the possibility that a bug or exploit in the code could lead to loss of funds. Additionally, DeFi yields can be volatile, swinging dramatically based on market liquidity and borrowing demand. While often higher than traditional finance, these yields reflect the elevated technical and operational risks involved.

Real world asset yields explained

The crypto lending landscape is shifting from speculative, high-risk protocols toward tokenized real-world assets (RWA). This transition is driven by the structural difference between algorithmic stablecoin yields and tokenized treasury bills. Understanding this distinction is critical for evaluating risk-adjusted returns in the current market.

The Yield Gap: Stablecoins vs. Tokenized Treasuries

Historically, on-chain stablecoin yields were inflated by speculative demand and complex leverage loops. These returns were not backed by underlying economic activity but by the need to incentivize liquidity in volatile markets. In contrast, tokenized treasury bills offer a yield derived from actual U.S. government debt. This provides a transparent, lower-risk baseline that is directly correlated with traditional monetary policy rather than crypto-native speculation.

The spread between these two sources represents the primary risk premium in the current market. Tokenized treasuries typically track the risk-free rate, while on-chain stablecoin protocols must offer a significant premium to attract capital away from safer alternatives. This premium compensates lenders for smart contract risk, counterparty insolvency, and regulatory uncertainty.

Evaluating the Risk-Adjusted Return

When assessing RWA yields, focus on the source of the cash flow. Tokenized treasuries distribute interest payments directly from the U.S. Treasury, making the yield predictable and auditable. Stablecoin yields, however, often rely on fees from lending platforms or trading volumes, which can evaporate during market downturns.

A conservative approach prioritizes transparency and regulatory compliance. Look for protocols that provide proof of reserves and clear legal structures for the underlying assets. The goal is to capture yield without assuming the full risk of a depeg event or smart contract exploit.

Live Market Indicators

To contextualize these yields, monitor the performance of major stablecoins and treasury-backed tokens. The following widgets provide live market data for USDC and tokenized treasury products, reflecting current supply and demand dynamics.

DeFi infrastructure risks

Crypto Lending works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Choosing a lending platform

Picking the wrong platform is the fastest way to lose principal. You aren't just looking for the highest APY; you're looking for a vault that won't burst when the market turns. The best crypto lending platforms share three traits: they have been audited by reputable firms, they maintain healthy over-collateralization ratios, and they operate within clear regulatory frameworks.

Start by checking the audit history. Look for recent reports from firms like CertiK, OpenZeppelin, or Trail of Bits. An audit isn't a guarantee of safety, but it is proof that the code has been reviewed for vulnerabilities. Avoid platforms that rely on "internal security" without third-party verification.

Next, examine the over-collateralization ratio. In DeFi, you typically need to deposit more crypto than you borrow (e.g., 150%). This buffer protects lenders if the asset price drops. Centralized platforms may offer lower collateral requirements, but this increases their risk of insolvency during a crash. Higher collateral means lower yield, but it significantly reduces the risk of a liquidation cascade.

Finally, verify regulatory compliance. Platforms registered with financial authorities (like the FCA or SEC) are subject to stricter capital requirements and consumer protections. While DeFi offers anonymity, it offers no recourse if something goes wrong. For high-stakes capital, a regulated entity or a heavily audited, established DeFi protocol is safer than a new, anonymous project.

| Platform | Type | Audit Status | Min Collateral |

|---|---|---|---|

| Aave | DeFi | CertiK, OpenZeppelin | 125-150% |

| Compound | DeFi | OpenZeppelin, Trail of Bits | 125-150% |

| Nexo | CeFi | Internal + External | 20-50% |

| BlockFi (Historical) | CeFi | Limited | 50% |

Start lending safely checklist

Before deploying capital into RWA yields or DeFi protocols, treat your due diligence like a security audit. One missed variable can lead to total loss. Follow this ordered checklist to verify platform integrity and collateral health.

Check for recent third-party security audits (e.g., CertiK, OpenZeppelin) and any regulatory licenses. Avoid platforms with no public code verification or opaque legal structures. Coinbase outlines the basic mechanics, but you must dig deeper into the specific protocol's legal standing.

Ensure the platform maintains over-collateralization, typically above 150% for volatile assets. This buffer protects lenders if the underlying crypto price drops sharply. Check the liquidation thresholds to understand how quickly positions might be closed.

Review the platform's on-chain reserves. Can you withdraw your funds immediately, or are there lock-up periods? Transparent platforms publish real-time proof of reserves. Lack of liquidity visibility is a major red flag for solvency.

Be skeptical of yields that significantly outpace risk-free rates without a clear, explainable source. If the yield relies on complex, untested mechanisms, it may be unsustainable. Prioritize platforms with clear, documented revenue sources.

Never lend your entire capital to a single platform. Spread your exposure across multiple reputable protocols to mitigate the risk of a single point of failure. This is your primary defense against platform-specific insolvency.

No comments yet. Be the first to share your thoughts!