Crypto lending analysis limits to account for

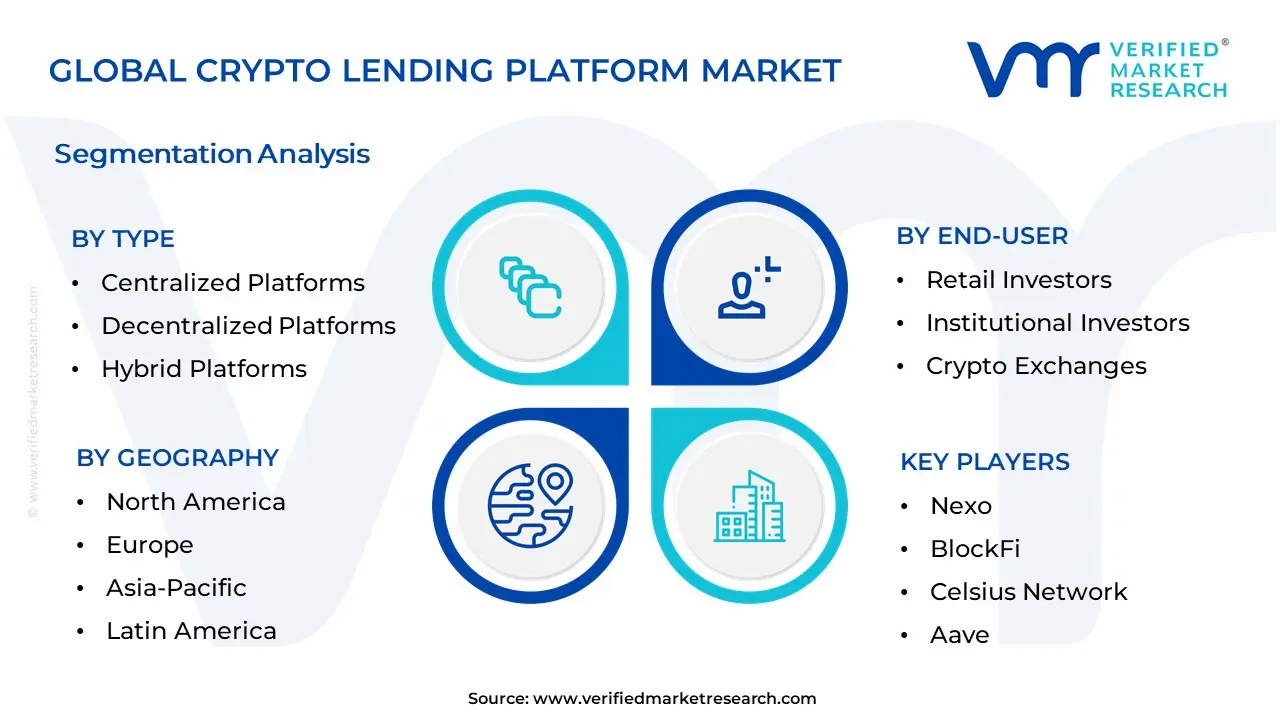

Evaluating crypto lending requires separating yield from survival. The market is not a monolith; it is a fragmented ecosystem where platform dominance and asset class dictate risk differently. To analyze this space effectively, you must look beyond the headline APY and examine the underlying mechanics of liquidity and collateral management.

CeFi concentration and counterparty risk

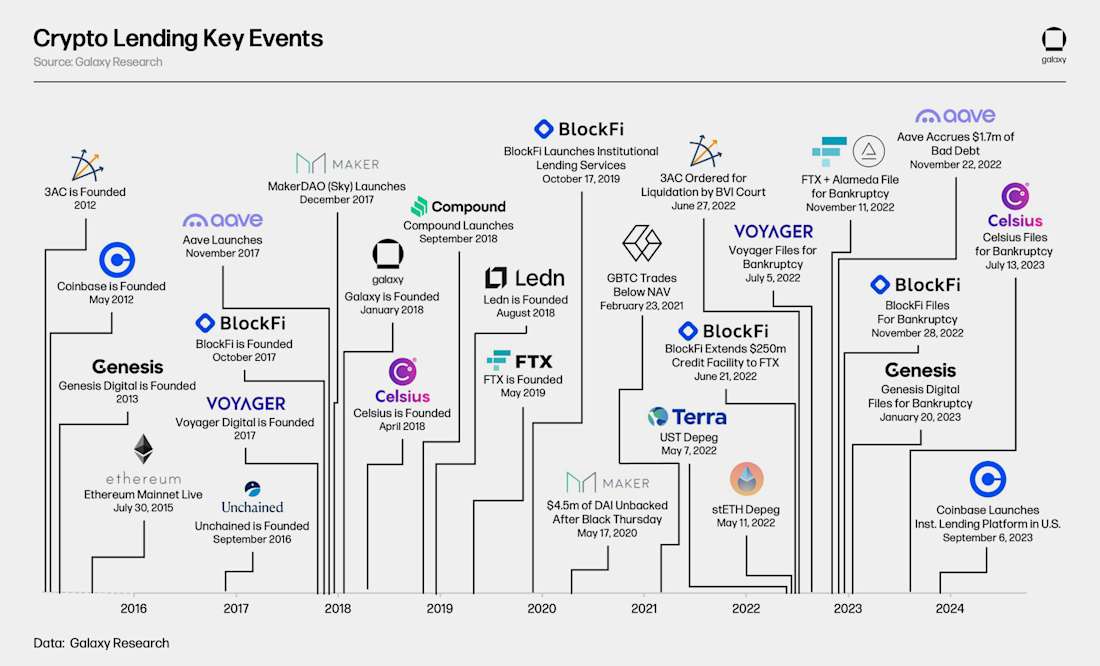

Centralized finance (CeFi) lending is dominated by a handful of entities, creating systemic concentration risks. Tether commands a 57% share of the CeFi lending market, followed by Nexo at 11% (Galaxy Research, Q2 2025). This concentration means that regulatory pressure or operational failure on one platform can ripple through the entire sector. When analyzing a CeFi lender, scrutinize their proof of reserves and audit history. The platform’s ability to honor withdrawals during market stress is more important than its marketing claims.

Stablecoin yield vs. volatility exposure

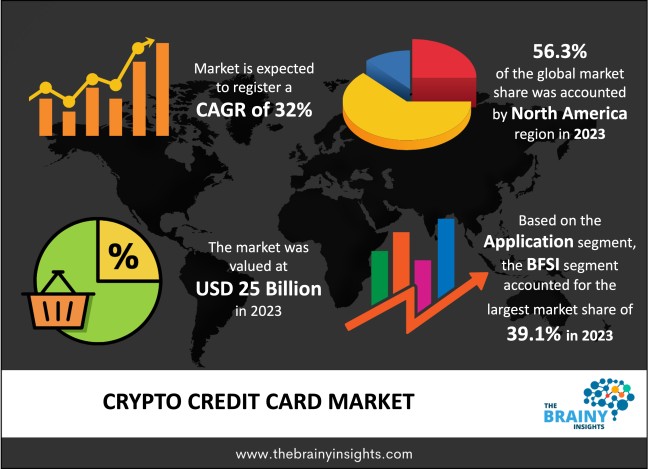

Yield structures vary drastically by asset type. While Bitcoin-backed loans typically offer rates between 3% and 8%, stablecoin lending often commands 10% to 18% (Emboker, 2026). This spread reflects the underlying risk: stablecoin yields are often backed by higher-risk DeFi strategies or corporate credit exposure. If you are analyzing stablecoin lending, assume the principal is at risk. The high yield is compensation for potential depegging events or smart contract failures, not a guarantee of income.

Liquidation mechanics and collateral volatility

The primary danger in crypto lending is liquidation. If the price of your collateral falls, the loan-to-value (LTV) ratio increases, triggering a margin call or forced sale (Better Markets). Unlike traditional finance, crypto markets can move 20% in hours. A robust lending analysis must stress-test collateral against historical drawdowns. If the platform’s liquidation threshold is tight, a minor market dip can wipe out your equity. Always calculate the "liquidation price" before locking assets, and factor in the platform’s liquidation penalty fees.

Regulatory clarity as a risk factor

Regulatory uncertainty remains the largest unknown. Platforms operating in gray jurisdictions face sudden shutdowns or asset freezes. Analyze where the entity is legally domiciled and whether it complies with local financial regulations. Jurisdictions with clear crypto frameworks (e.g., Switzerland, Singapore) offer slightly more protection than those with bans or ambiguous rules. Never lend more than you can afford to lose, regardless of the platform’s regulatory status.

Crypto lending analysis choices that change the plan

Use this section to make the Crypto Lending Analysis decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Build a decision framework for crypto lending

Crypto lending is not a passive savings account; it is an active risk management exercise. The market has shifted from the opaque, high-yield environments of 2021 to a more regulated, infrastructure-heavy landscape. To navigate this in 2026, you need a structured approach that prioritizes capital preservation over speculative yield.

The following steps outline a practical framework for evaluating lending opportunities, focusing on platform reliability, collateral safety, and regulatory compliance.

Start by verifying where your assets are held. Top-tier platforms now provide regular attestation reports from independent auditors, detailing their reserves and liabilities. Avoid platforms that do not publish these reports or rely solely on internal accounting. Look for "proof of reserves" that includes real-time on-chain verification, not just quarterly snapshots.

Regulatory clarity is the new baseline for safety. Prefer platforms registered with recognized financial authorities, such as the SEC or FCA, or those operating in jurisdictions with clear crypto-lending frameworks. Unregulated entities pose significant counterparty risk, as seen in the collapse of major lenders during the 2022 crisis. Check if the platform is subject to regular compliance audits.

Understand the loan-to-value (LTV) ratios and liquidation thresholds. Crypto-backed loans are sensitive to market volatility; a sharp price drop can trigger automatic liquidation. Choose platforms with conservative LTV limits (e.g., 50-60% for volatile assets like Bitcoin) and clear, automated liquidation processes. Avoid platforms that allow excessive leverage without adequate margin calls.

Never concentrate your lending capital on a single platform. Spread your exposure across multiple regulated lenders and decentralized finance (DeFi) protocols. This diversification mitigates the risk of a single point of failure, such as a platform hack or insolvency. Consider using a mix of centralized lending for ease of use and decentralized protocols for transparency.

High yields often signal high risk. In 2026, stablecoin lending rates typically range from 3% to 8%, while volatile assets may offer higher but riskier returns. Be skeptical of yields exceeding 15% unless backed by robust, transparent mechanisms. Compare rates across platforms to identify outliers and understand the underlying risk premium. Use tools like the Galaxy Crypto Lending Index to track market averages.

By following this framework, you can make informed decisions that balance potential returns with the inherent risks of crypto lending. Always prioritize platforms with strong regulatory compliance and transparent operational practices.

Spot the Weak Links in Crypto Lending

The crypto lending landscape is shifting fast, and not all platforms are built to handle the new regulatory reality. While some platforms promise high yields, they often mask significant structural risks that can wipe out principal. Understanding where the weak options fail is just as important as finding the strong ones.

The Liquidity Trap

Many platforms advertise impressive annual percentage yields (APY) but fail to disclose the liquidity constraints. If a platform cannot meet withdrawal requests during market stress, your "yield" becomes irrelevant. Galaxy Research notes that Tether dominates the CeFi lending market with a 57% share, highlighting how concentrated this sector really is. Relying on smaller, less transparent platforms exposes you to counterparty risk that isn't covered by insurance or reserves.

Volatility and Liquidation Risk

Crypto-backed loans are not risk-free just because you hold the collateral. Better Markets warns that wild price swings can quickly affect the value of your collateral, triggering liquidations. If the loan-to-value (LTV) ratio rises too fast, the platform may sell your assets at a loss. This is especially dangerous with volatile assets like Bitcoin or Ethereum, where a 10% drop in hours can trigger a cascade of forced sales.

Regulatory Blind Spots

With 2026 bringing stricter oversight, platforms operating in gray areas face sudden shutdown risks. Avoid platforms that do not clearly state their regulatory compliance status or jurisdiction. If a platform is not registered or licensed in a major financial hub, it may not be able to operate legally in your region next year. Always check for official regulatory filings before locking up your assets.

Crypto lending analysis: what to check next

Before committing capital to crypto lending platforms, it is essential to understand the mechanics of profitability and the specific risks involved. The landscape has shifted significantly with new regulatory scrutiny, making due diligence more critical than ever.

These questions highlight that while crypto lending offers liquidity and yield, it requires active monitoring of collateral ratios and platform health.

No comments yet. Be the first to share your thoughts!