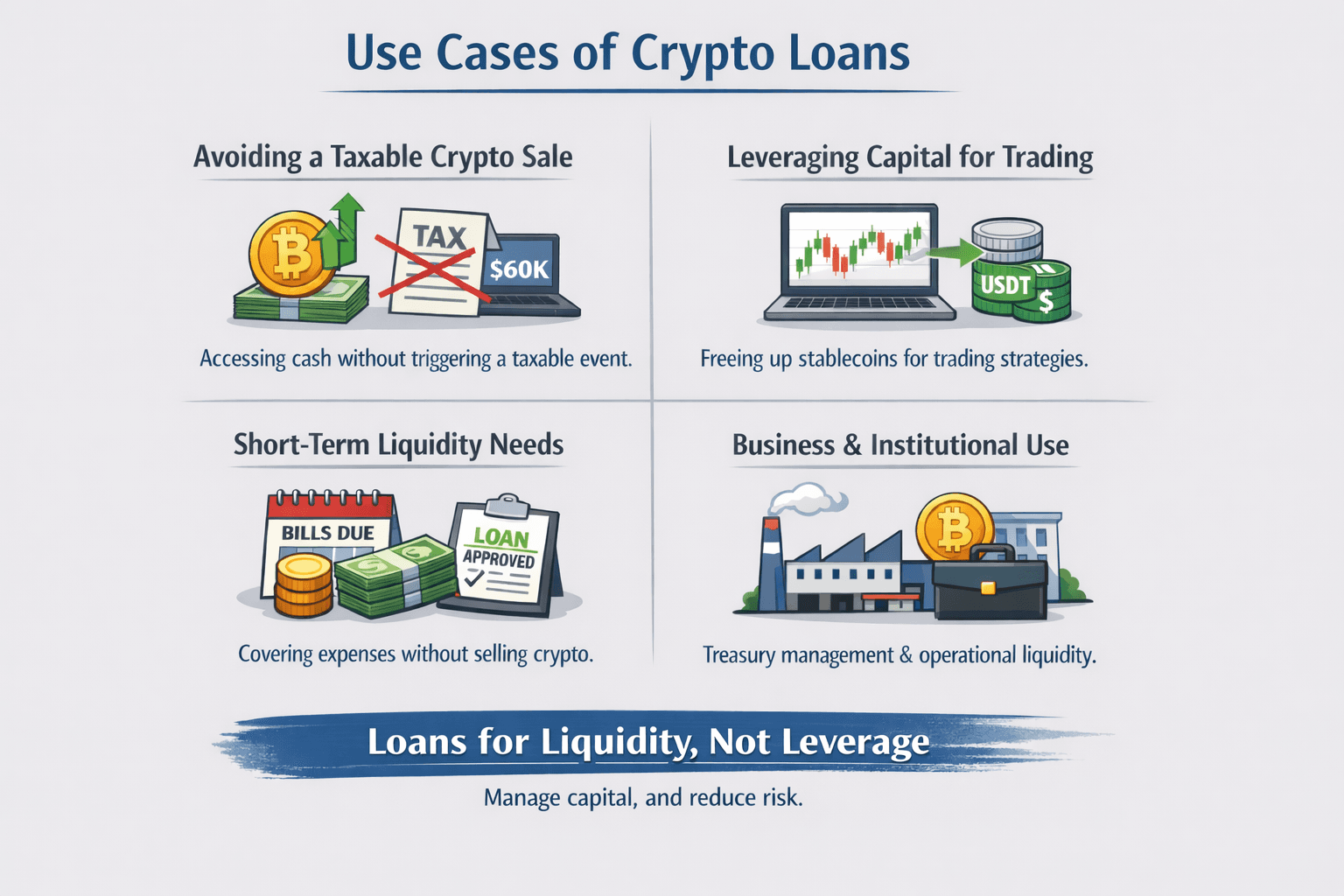

Defining the crypto lending strategy

A crypto lending strategy involves lending cryptocurrency to earn interest, functioning as a digital alternative to traditional bank loans. Instead of relying on centralized institutions, this process is governed by smart contracts or regulated platforms, allowing lenders to yield on idle assets while borrowers access liquidity without selling holdings.

There are two primary models for executing this strategy: decentralized finance (DeFi) and centralized finance (CeFi). In CeFi, you lend assets to a platform that acts as an intermediary, similar to a bank. In DeFi, you lend directly to a liquidity pool via a smart contract, removing the middleman but introducing technical risks. Understanding the distinction between these two models is the first step in building a secure lending framework.

While potential returns can be attractive, they come with significant risks. Lending rates for cryptocurrencies typically range from 3% to 8%, while stablecoins may offer between 10% and 18%. However, high returns often correlate with higher exposure to market volatility and platform insolvency. A sharp drop in the value of collateral can trigger margin calls, forcing borrowers to add funds or risk liquidation. Therefore, a robust strategy must prioritize risk management over yield chasing.

The chart above illustrates the volatility inherent in crypto assets. When using volatile assets like Bitcoin as collateral, price swings can quickly erode your loan-to-value ratio. This volatility is the primary driver of risk in crypto lending, making it essential to choose your collateral and counterparty carefully before committing capital.

CeFi vs DeFi lending infrastructure

Choosing a crypto lending strategy requires deciding where your assets will live. The two primary models—Centralized Finance (CeFi) and Decentralized Finance (DeFi)—offer distinct trade-offs between convenience and control. Understanding these infrastructure differences is critical because the risks are fundamentally different: one exposes you to corporate failure, the other to code failure.

CeFi platforms operate like traditional banks. You deposit crypto into an account managed by a company, which then lends those funds to institutional borrowers or uses them for proprietary trading. The interface is familiar; you log in with an email and password, and the platform handles the complex matching of borrowers and lenders. This ease of use is the primary draw. However, this convenience comes with significant counterparty risk. As seen in the collapses of major lenders like Celsius and Voyager, if the central entity mismanages funds or faces a liquidity crisis, your assets can vanish overnight. You are trusting a single point of failure to safeguard your collateral.

DeFi lending flips this model by removing the middleman entirely. Instead of a company, you interact with smart contracts on a blockchain. These self-executing programs hold your collateral and automatically release loans based on predefined rules. The primary advantage is transparency and non-custodial control. You retain ownership of your keys, and the logic of the lending protocol is visible on-chain for anyone to audit. There is no CEO to sue and no customer support team to call if the code fails.

The trade-off for this autonomy is complexity. DeFi requires a deeper understanding of blockchain mechanics, gas fees, and smart contract risks. If a protocol contains a bug or is exploited by an attacker, the loss is often irreversible. Additionally, DeFi lending typically requires over-collateralization; you must lock up more value in crypto assets than you borrow, usually at a ratio of 110% or higher, to protect lenders against volatility [src-serp-1].

To help visualize these structural differences, here is a side-by-side comparison of the two models:

| Feature | CeFi (Centralized) | DeFi (Decentralized) |

|---|---|---|

| Custody | Platform holds your keys | You hold your keys (non-custodial) |

| Transparency | Audited financial reports (opaque) | Real-time on-chain ledger (transparent) |

| Risk Type | Counterparty/Bankruptcy risk | Smart contract/Hack risk |

| User Experience | Simple, email/password login | Complex, wallet connection required |

| Collateral | Often uncollateralized (credit-based) | Always over-collateralized (crypto-for-crypto) |

| Privacy | KYC/Identity verification required | Pseudonymous, no ID required |

The choice between CeFi and DeFi ultimately depends on your risk tolerance and technical comfort. CeFi offers a streamlined experience for those willing to accept institutional risk, while DeFi provides sovereignty for those comfortable managing their own security. For many crypto lending strategies, the decision isn't binary; some investors diversify across both to balance convenience with security.

Where Yield Comes From and What Can Go Wrong

Crypto lending isn't a single product; it's a collection of different risk profiles. To build a sound crypto lending strategy, you need to understand that yield sources fall into two distinct buckets: stablecoins and volatile assets. The return you earn is directly tied to the risk you take on.

Stablecoin Yields: The 10–18% Range

Stablecoins like USDC or USDT typically offer the highest yields, often ranging from 10% to 18%. This premium exists because these assets are used heavily for leverage and short-term liquidity in the DeFi ecosystem. Borrowers are willing to pay higher rates to access capital without selling their underlying positions.

However, higher yield doesn't mean safer. These platforms often lend to riskier counterparties or use complex strategies to generate returns. If the underlying borrowers default or the protocol's strategy fails, your stablecoin principal is at risk. You are effectively trading credit risk for yield.

Volatile Asset Yields: The 3–8% Range

Lending volatile assets like Bitcoin or Ethereum generally yields between 3% and 8%. While these numbers look lower, they come with different dynamics. The primary risk here is price volatility. If the value of your collateral drops significantly, you may face a margin call.

In a crypto-backed loan, if the collateral value falls below a certain threshold, the protocol may liquidate your assets to cover the loan. This means you could lose your Bitcoin even if you intended to hold it long-term. The yield is compensation for this liquidation risk and the platform's insolvency risk.

Platform Insolvency and Counterparty Risk

Beyond asset-specific risks, every lending platform carries the risk of insolvency. Unlike traditional banks, most DeFi lending protocols are not insured. If a platform is hacked, exploited, or runs out of liquidity, your funds may be gone. Always check the protocol's audit history and total value locked (TVL) as indicators of stability.

When evaluating a crypto lending strategy, look beyond the Annual Percentage Yield (APY). Consider the platform's track record, the transparency of its reserves, and the specific mechanics of how your assets are being lent out. Higher yields often mask higher risks that can erase your gains in a single market downturn.

Selecting platforms and collateral

Choosing a crypto lending strategy requires more than comparing interest rates. You need to evaluate the collateral requirements, loan-to-value (LTV) ratios, and the regulatory standing of the platform. A platform offering high yields often masks significant counterparty risk or restrictive collateral terms.

Start by analyzing the LTV ratio. This metric determines how much you can borrow against your crypto assets. A lower LTV ratio (e.g., 50%) reduces the risk of liquidation if the asset price drops, while a higher LTV (e.g., 75-80%) offers more liquidity but increases exposure to margin calls. Stablecoins typically support higher LTVs due to lower volatility, whereas volatile assets like Bitcoin or Ethereum require stricter collateralization.

Regulatory compliance is equally critical. Platforms operating with proper licensing or registered entities provide a layer of legal recourse that anonymous DeFi protocols lack. While DeFi offers censorship resistance and often better rates, it shifts the entire risk burden to the user. If you prioritize capital preservation, stick to regulated custodians. If you seek maximum yield, understand that you are trading regulatory protection for potential returns.

Current market conditions for stablecoins, which often form the basis of these loans, fluctuate rapidly. Monitoring live rates helps you time your entry and understand the opportunity cost of locking up assets.

When selecting a platform, consider whether you need the anonymity of DeFi or the stability of a regulated lender. The "best" platform depends on your risk tolerance and whether you value regulatory oversight over yield potential.

Executing your lending workflow

Turning a crypto lending strategy into live capital requires discipline. Unlike traditional banking, DeFi infrastructure moves fast, and smart contract risks are real. Follow this checklist to deploy funds safely and avoid common pitfalls.

Before depositing, audit the protocol’s code. Look for recent third-party security audits from reputable firms like OpenZeppelin or CertiK. Check the total value locked (TVL) and user count to gauge community trust. Avoid unverified contracts, even if the yield looks attractive.

Understand the loan-to-value (LTV) ratio. Most platforms require over-collateralization, meaning you must deposit more crypto than you borrow. For example, a 70% LTV means you borrow $70 for every $100 deposited. Higher volatility assets often require higher collateral ratios to prevent liquidation.

Set price alerts for your collateral assets. If the market drops, your position may be liquidated, meaning you lose your collateral. Maintain a buffer below the liquidation price to avoid margin calls. Consider using stablecoins as collateral if you want to minimize volatility risk, though yields may be lower.

Do not put all your capital into one protocol. Spread your lending across multiple DeFi platforms to mitigate counterparty risk. If one protocol suffers a hack or exploit, your other positions remain safe. This diversification is a core principle of any robust crypto lending strategy.

Common questions on crypto lending

Crypto lending strategy involves balancing yield against the specific risks of decentralized and centralized infrastructure. Below are direct answers to frequent questions about profitability, risk, and platform selection.

When evaluating a crypto lending strategy, prioritize platforms with transparent reserve audits and strong security histories. The difference between a 5% yield and a 15% yield often reflects the level of counterparty risk you are assuming.

No comments yet. Be the first to share your thoughts!