The market has crossed $73 billion

Crypto-collateralized lending reached an all-time high of $73.6 billion at the end of Q3 2025, according to Galaxy Research. This milestone marks a decisive structural shift in how digital assets are leveraged, moving away from traditional, centralized venues toward onchain protocols.

The composition of this market has changed dramatically. Lending applications now account for more than 80% of the onchain market volume. This stands in stark contrast to Q4 2021, when lending made up just 53% of the market, with Crypto-Loan Products (CDPs) dominating the remaining share. The 16% CDP share seen in Q3 2025 reflects a maturation of the sector, where direct lending against collateral has become the primary vehicle for yield and liquidity.

This growth is not merely additive; it is redistributive. Capital that previously flowed into opaque, centralized finance (CeFi) platforms is increasingly settling on transparent, onchain ledgers. The efficiency of these protocols, combined with the demand for yield in a high-interest rate environment, has driven this migration. As the market expands, the distinction between CeFi and DeFi lending is becoming less about availability and more about the trade-offs between counterparty risk and capital efficiency.

DeFi infrastructure vs centralized platforms

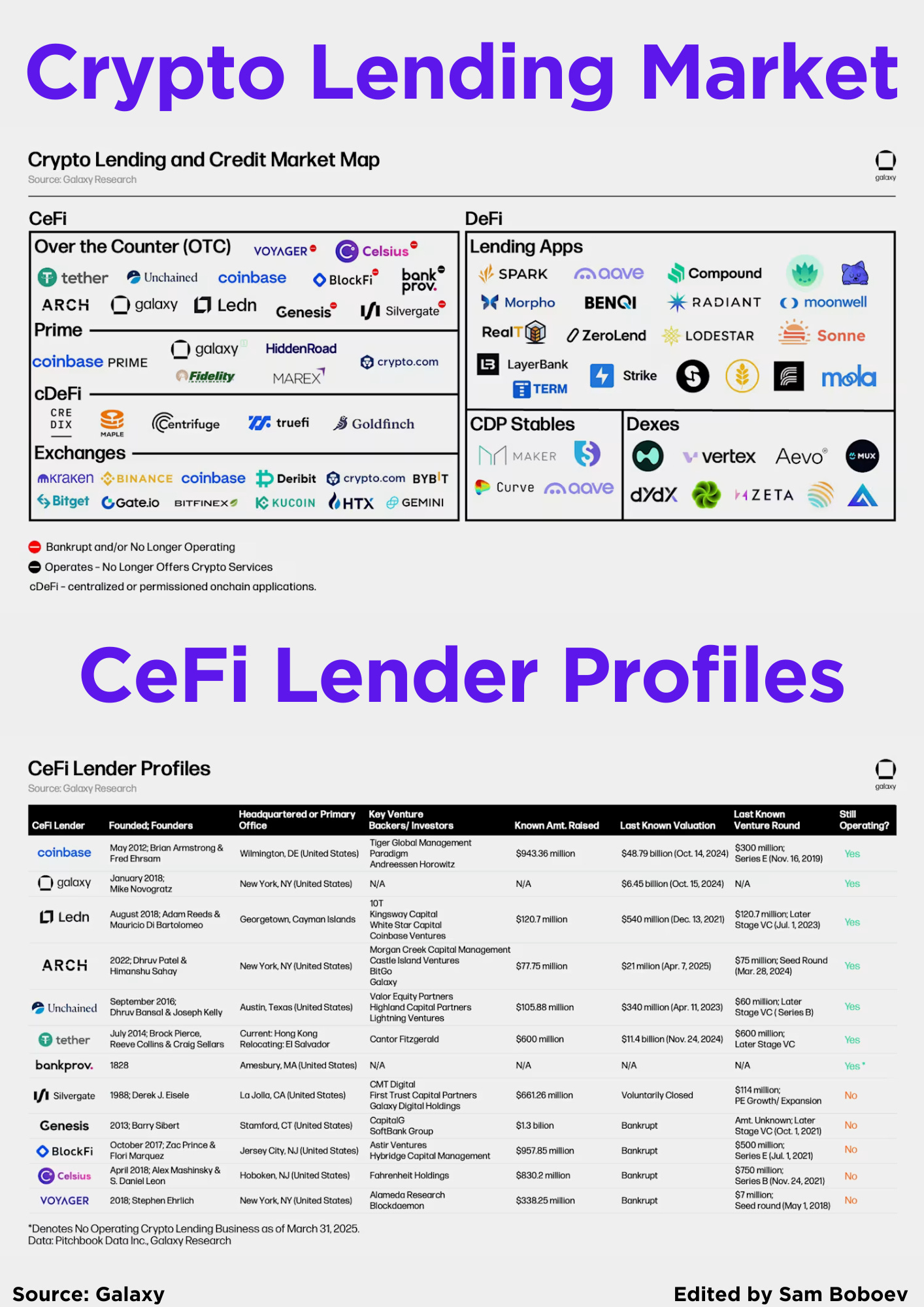

The crypto lending market operates on two distinct rails: decentralized protocols and centralized finance (CeFi) entities. Understanding the structural differences between these models is essential for evaluating risk and yield in 2026. DeFi platforms like Aave and Compound rely on smart contracts and on-chain transparency, while CeFi platforms like Coinbase Prime and Figure Technologies act as intermediaries, holding custody of assets and managing credit risk internally.

Custody and Control

In DeFi, custody is non-custodial. Users retain control of their private keys or interact directly with their wallets via flashbots or other MEV-protecting relays. This eliminates counterparty risk associated with a centralized entity going insolvent, but introduces smart contract risk. If a protocol has a vulnerability, funds can be drained. In CeFi, the platform holds custody of user assets. This offers a familiar user experience and often includes insurance funds or regulatory protections, but users must trust the platform’s solvency and operational integrity. The collapse of Celsius or BlockFi serves as a historical reminder of this centralized risk.

Transparency and Auditability

DeFi lending markets are fully on-chain. Every deposit, borrow, liquidation, and interest accrual is visible in the blockchain ledger. This real-time transparency allows for continuous risk assessment by the community. CeFi platforms, by contrast, operate as black boxes. While reputable providers like Coinbase Institutional publish market intelligence and maintain regulatory compliance, their internal balance sheets and exposure to specific borrowers are not publicly auditable in real-time. This opacity can hide correlated risks until a liquidity crunch occurs.

Yield Sources

Yield in DeFi is primarily generated by borrowing interest paid by traders and arbitrageurs, often amplified by protocol incentives (token emissions). This yield is volatile and closely tied to network activity. CeFi yields are typically derived from lending assets to institutional borrowers, hedge funds, or corporate clients (such as Figure’s digital asset lending platform). These yields are often more stable but may be capped by the platform’s business model and regulatory constraints.

The following table compares the core operational differences between these two lending rails.

| Feature | DeFi (Aave, Compound) | CeFi (Coinbase, Figure) |

|---|---|---|

| Custody | Non-custodial (user-controlled) | Custodial (platform-held) |

| Transparency | Fully on-chain, real-time | Partial, periodic reports |

| Counterparty Risk | Smart contract bugs/hacks | Platform insolvency/fraud |

| Yield Source | Borrower interest + incentives | Institutional lending spreads |

| Regulation | Minimal, code is law | Heavy, compliance-heavy |

Tracking Yields and Leverage Trends

Interest rates in crypto lending are not static; they act as a barometer for liquidity and sentiment. Unlike traditional finance, where central banks set a baseline rate, decentralized and centralized platforms adjust yields in real time based on supply and demand. When demand for borrowing surges, rates spike, rewarding lenders with higher returns. When liquidity dries up or borrowers step back, yields compress.

This dynamic is clearly visible in the shift from collateralized debt positions (CDPs) to direct lending applications. According to Galaxy Research, by the end of Q3 2025, lending applications accounted for more than 80% of the onchain market, a significant departure from the 53% share seen in Q4 2021. This structural shift means that current yield trends are driven more by active borrowing demand for trading and leverage than by long-term collateralization.

To understand the current landscape, it helps to look at the underlying asset prices and their correlation with lending activity. The value of collateral, primarily Bitcoin and Ethereum, directly influences the available liquidity pool. When these assets rally, lending volumes often increase as traders seek leverage, pushing rates up. Conversely, during bear markets, rates may fall as lenders compete for scarce borrowers or flee to stablecoin yields.

The following chart illustrates the price action of Ethereum, a primary collateral asset in DeFi lending markets. While it doesn't show lending rates directly, the volatility and trend of ETH often precede or coincide with shifts in DeFi lending liquidity and yield opportunities.

For a quick snapshot of the current market value, here is the live price of Ethereum:

How regulators classify crypto lending

The International Monetary Fund recently issued an issue note detailing how to record crypto lending in macroeconomic statistics. This guidance marks a shift from viewing these assets as speculative curiosities to treating them as formal financial instruments. By establishing a standard for how central banks should count crypto lending activity, the IMF is signaling that this sector is maturing into a recognized part of the global financial system.

The distinction matters because it changes how institutions measure risk and liquidity. When regulators can accurately track lending flows, they can better assess systemic exposure. This classification framework helps financial authorities distinguish between traditional fiat loans and crypto-based borrowing, allowing for more precise monetary policy adjustments. The move toward standardized reporting suggests that crypto lending is no longer an underground economy but a transparent, measurable asset class.

As official bodies integrate crypto lending into their statistical models, the market faces increased scrutiny but also greater legitimacy. This regulatory clarity encourages institutional participation, which can stabilize yields and reduce the volatility that has historically characterized the sector. The IMF’s approach provides a blueprint for other international organizations, potentially leading to a more unified global regulatory stance on digital asset lending.

Choosing a lending strategy for 2026

The global crypto lending platform market is projected to reach $25.06 billion by 2030, driven by an 18.5% annual growth rate as institutional and retail participants seek yield in a maturing asset class. Selecting the right lending path requires aligning your strategy with three variables: risk tolerance, capital size, and the specific nature of your yield target.

For large capital deployments seeking stability, centralized finance (CeFi) offers institutional-grade security and predictable returns. Platforms like Figure provide crypto-backed loans with same-day approval and flexible payment options, allowing borrowers to access liquidity without triggering taxable events. This approach suits investors who prioritize capital preservation and regulatory compliance over maximum yield. The trade-off is lower returns compared to decentralized alternatives, as CeFi platforms bundle insurance and operational costs into their pricing models.

Smaller portfolios or those prioritizing high yield may prefer decentralized finance (DeFi). DeFi lending protocols offer transparent, permissionless access to liquidity but require active management of smart contract risks and volatility. The absence of intermediaries allows for higher yields, but users must navigate impermanent loss, protocol exploits, and complex governance mechanisms. This path is best suited for technically proficient users who can monitor on-chain metrics and adjust positions dynamically.

A hybrid strategy often provides the optimal balance. Allocate the majority of capital to CeFi for steady, low-risk income, while using a smaller portion for DeFi experiments to capture higher yields. This diversification mitigates the impact of any single platform failure while maintaining exposure to the sector's growth. As the market evolves, staying informed about regulatory changes and protocol updates will be essential for long-term success.

| Feature | DeFi | CeFi |

|---|---|---|

| Risk Level | High | Medium |

| Yield Potential | High | Low to Medium |

| Accessibility | Permissionless | KYC Required |

| Management | Active | Passive |

The choice between DeFi and CeFi is not binary but a spectrum of risk and reward. By understanding the trade-offs and aligning them with your financial goals, you can construct a lending strategy that withstands market volatility while capturing the upside of the crypto economy.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!